{kind=link}

The knowledge offered on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation. See Lexington Legislation’s editorial disclosure for extra info.

You possibly can decrease your bank card rate of interest by following good credit score habits and having a stable historical past of on-time funds, researching how your present rate of interest stacks up in opposition to competing bank card corporations’ provides and calling your bank card issuers to barter a decrease rate of interest and clarify why you deserve it.

As an informed client and a accountable borrower, it’s possible you’ll be questioning how one can decrease your hefty bank card rates of interest. In any case, a number of years have in all probability handed because you first utilized, and maybe your credit score has improved since then. Fortunately, it’s very attainable to attain a diminished fee by following these steps:

- Work to enhance your possibilities of getting permitted by following good credit score habits and guaranteeing you’ve a stable historical past of on-time funds.

- Analysis your present rate of interest and the way it stacks as much as what competing bank card corporations are providing.

- Name your bank card issuers to barter a decrease rate of interest, explaining why you deserve it.

- When you’re rejected, strive once more and ask to talk to a unique individual, or think about different choices.

Desk of contents:

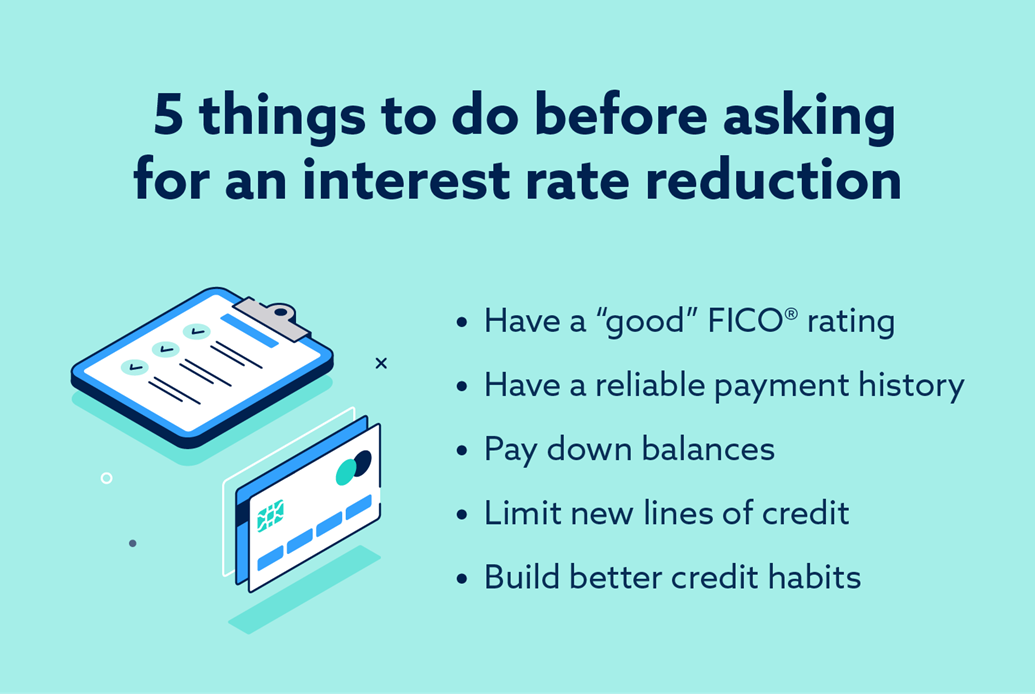

1. Enhance your probabilities of getting permitted

Since curiosity expenses are an enormous moneymaker for bank card issuers, a diminished fee is an enormous ask. Bank card corporations will seemingly solely be keen to bend for his or her finest clients, so that you’ll first need to do the whole lot you possibly can to set your self up for fulfillment.

This implies guaranteeing your credit score is in tip-top form—particularly, a “good” FICO ranking or higher. Purpose for a FICO® rating of not less than 670 earlier than you ask for an rate of interest discount, though it’s possible you’ll need to goal for 740 to bump your self as much as the “superb” bracket.

You’ll additionally need to guarantee you’ve a dependable historical past of on-time funds. When you’ve had a shaky historical past of missed or late funds, it’s possible you’ll need to deal with making on-time funds for a 12 months earlier than you ask for a diminished rate of interest.

One other indication of a stable bank card buyer is somebody who’s keen to pay down their balances and scale back their debt even earlier than asking for a fee discount. Decrease debt ranges could point out higher monetary standing, which may enhance an individual’s negotiating energy.

When you’re planning to ask for a discount in your rate of interest, it’s smart to attempt to keep away from making use of for brand spanking new traces of credit score. As it’s possible you’ll already know, credit score inquiries can negatively influence your credit score. Opening new bank cards or making use of for extra loans could negatively have an effect on your negotiating energy and talent to qualify for a fee discount.

Bettering your credit score standing, particularly when you’ve beforehand struggled with destructive gadgets, is a course of that takes time. Slightly than in search of a quick-fix resolution, deal with constructing good credit score habits resembling the next:

- Setting cost reminders so that you keep in mind to pay bank card payments on time.

- Keep away from opening pointless credit score accounts.

- Keep away from closing outdated accounts until you’re certain it gained’t have an effect on your credit score historical past.

- Usually overview bank card statements and dispute unauthorized expenses.

- Use your bank card rewards properly (think about using money again to pay your invoice).

- Observe and shield your private info to keep away from fraud.

- Test your credit score report and file a dispute for any inaccuracies.

2. Do the analysis

Now that you just’ve labored to enhance your credit score standing, you’ll need to perform a little research earlier than calling your bank card issuer. First, verify what your present rate of interest is. Yow will discover this in your month-to-month bank card assertion. How does your fee evaluate to what’s thought-about “good”? How does it stack as much as charges that opponents are providing?

Decide a great bank card rate of interest

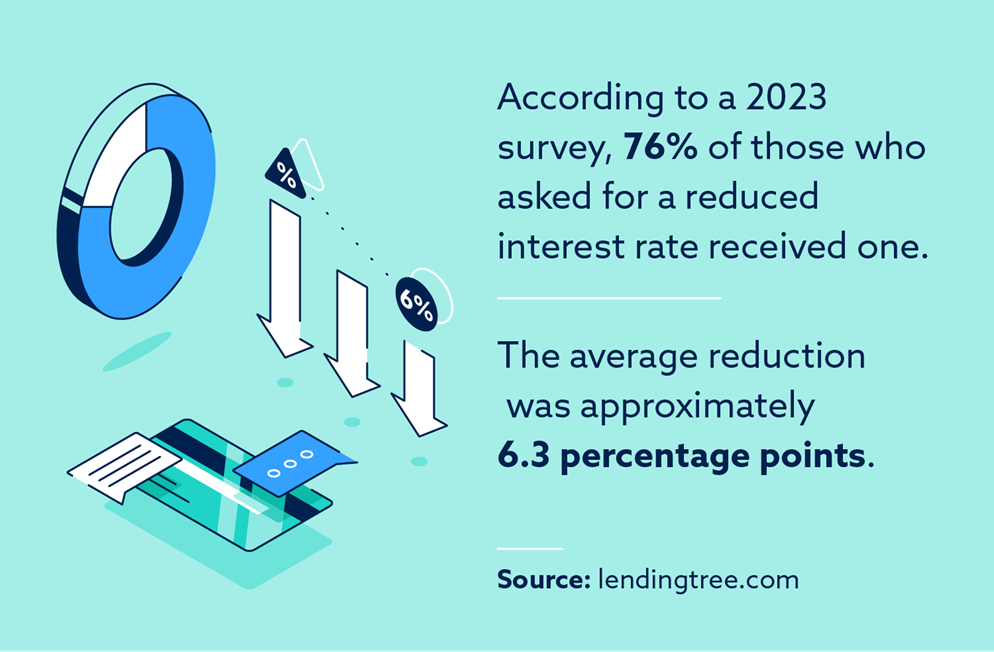

As of August 2023, the common bank card APR charged is 20.93 p.c. In case your rate of interest is even a number of proportion factors beneath this quantity, you’re seemingly working with a great rate of interest, and negotiations to go any decrease could also be unsuccessful.

On the flip facet, in case your rate of interest is considerably larger than common, you could have extra wiggle room to barter—particularly when you’ve improved your monetary standing and credit score because you first utilized.

Search for what opponents are providing

Bank card corporations should provide aggressive rates of interest to remain in enterprise. They comprehend it’s a aggressive business and that shedding clients is pricey. If yow will discover comparable playing cards with decrease rates of interest, you should utilize this as ammunition to barter a decrease fee.

Have a look at different accessible playing cards and their phrases and rates of interest. Pay attention to the cardboard title, bank card firm and rate of interest. Hold this helpful for when it’s time to name your bank card issuer. The extra particular you may be, the higher.

3. Ask your bank card issuers

When you’ve researched the competitors and labored to enhance your probabilities of getting permitted for a decrease rate of interest, it’s time to start calling your bank card issuers.

If in case you have a number of bank cards, name every one of many issuers and think about beginning with the cardboard you’ve had the longest. You’ll seemingly have probably the most success with the corporate you’ve the longest and finest monitor report with.

Alternatively, you would begin with the cardboard that carries the very best rate of interest. A discount right here may enable you save more cash, however needless to say it’s possible you’ll not have the ability to leverage your lengthy historical past as a dependable buyer.

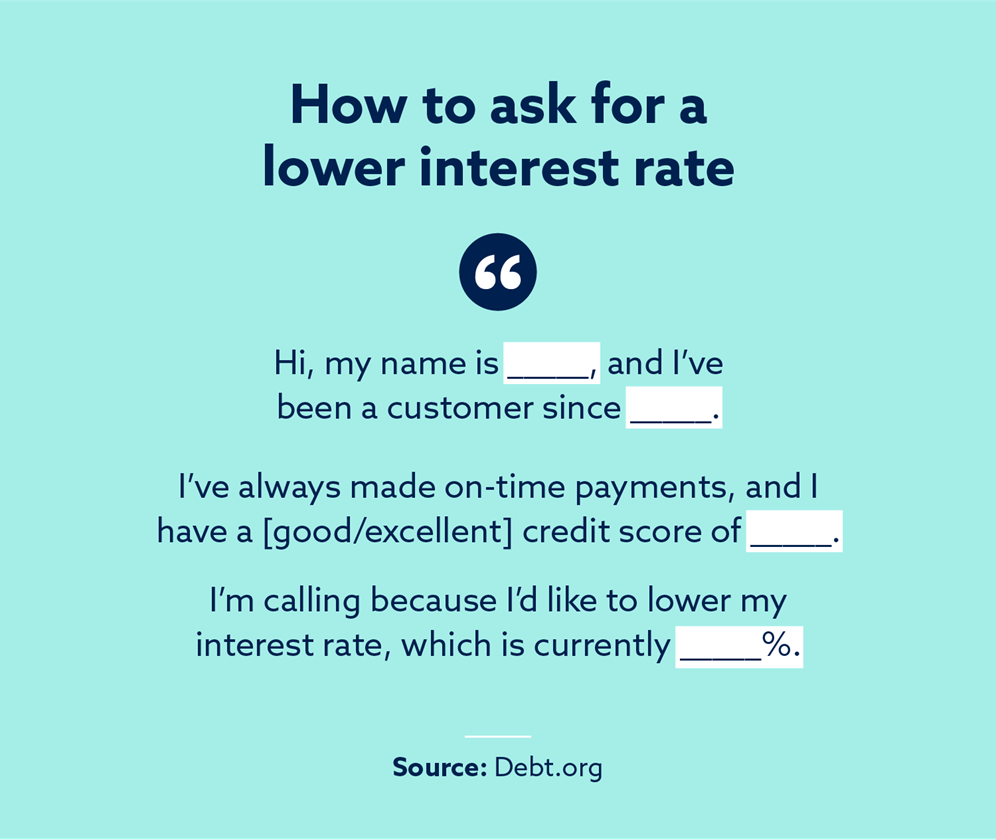

Begin by explaining who you’re and why you deserve consideration for an rate of interest discount. Be sure to say your credit score and what number of years you’ve been a buyer. Take into account the next script:

“Hello, my title is ____, and I’ve been a buyer since ____. I’ve at all times made on-time funds, and I’ve a [good/excellent] credit score rating of ____. I’m calling as a result of I’d prefer to decrease my rate of interest, which is presently ___ p.c.”

Do: Analysis beforehand, have particular numbers and know your price as a buyer.

Don’t: Go right into a name unprepared or with out understanding precisely what you’re asking for.

Then, clarify the explanation you need an rate of interest discount. Perhaps you’ve lately confronted furlough or wage cuts or it’s essential repay costly medical payments. Or possibly you’re simply attempting to enhance your credit score and wish to pay down your debt.

Do: Be factual and clarify your scenario.

Don’t: Be impolite, demanding or entitled.

That is additionally a good time to carry up opponents. When you put together for the decision, you can be conscious of opponents and what they’re providing. Be particular—point out different bank card corporations and their APR provides, and counsel that when you aren’t in a position to attain an settlement, you’ll think about taking your enterprise elsewhere for extra aggressive charges.

Do: Be particular about what different opponents are providing and see if they may match charges.

Don’t: Cancel your card when you don’t get a diminished fee, as this may increasingly damage your credit score rating.

When you rating a decrease fee—congratulations! Now transfer on to the following bank card issuer. When you obtain a “no,” or a compromised fee that’s nonetheless larger than you’d like, think about attempting once more at one other time or while you’ve additional improved your credit score.

Do: Be diligent about following up or talking to a supervisor if issues aren’t going properly.

Don’t: Hand over after the primary strive. Ask for the reasoning behind a “no” so you possibly can change your scenario to get the speed you need.

FAQ: Does asking for a decrease rate of interest have an effect on credit score rating?

The one means asking for a decrease rate of interest may damage your credit score rating is that if it requires the creditor to drag a tough inquiry. Bank card corporations could do that to take a look at your credit score report to see when you qualify for a decrease rate of interest.

A onerous inquiry could trigger your credit score to take a small hit—nevertheless, it could possibly solely have an effect on your credit score rating for as much as 12 months. That mentioned, when you efficiently rating a decrease rate of interest, it might not directly assist enhance your credit score since paying off your debt will likely be more cost effective.

Keep in mind that bank card rates of interest aren’t reported to credit score bureaus since they don’t immediately have an effect on your credit score, so a tough inquiry is the one state of affairs that may quickly damage your rating.

FAQ: Can I ask once more if I get rejected the primary time?

Sure. When you didn’t obtain the discount you’d like otherwise you have been merely advised “no,” you possibly can strive once more in a number of weeks, particularly when you can come up with another person the second time. Until the creditor has to drag a tough inquiry every time you ask for a fee discount, you possibly can ask a number of instances.

When you plan to name again once more, think about doing additional analysis beforehand and providing a purpose why it’s possible you’ll want a diminished rate of interest.

You might select to regulate your script to one thing just like the next:

“Hello, my title is _____, and I’ve been a buyer for _____ years. I’ve been steadily paying my bank card invoice and paying down balances since turning into your buyer, and I’ve a great/glorious credit score rating of ____.

Just lately, I’ve run into some monetary difficulties [briefly explain difficulties]. And seeing as I’ve been a loyal buyer with a superb monitor report, I’m calling to see when you would scale back my bank card rate of interest.

My present fee is ____ p.c, however I see that ____ bank card firm provides their ____ bank card, which is similar to mine, at a ____ p.c rate of interest. Would you be keen to match this fee or provide a decrease rate of interest, resembling ___ p.c?”

Bear in mind to be persistent, affected person and respectful, as completely different representatives and supervisors could provide various outcomes.

4. Take into account different choices

In case your bank card issuer gained’t budge in your rate of interest, it might be time to contemplate different methods to decrease your bank card rate of interest. Listed below are two non permanent options it’s possible you’ll think about whereas attempting to pay down your debt.

Attempt the stability switch methodology

When you’re sad along with your present rate of interest, a stability switch means that you can switch your present account stability to a unique card with a decrease rate of interest. You then make funds to your new account, saving cash in curiosity expenses.

Take into account that stability switch rates of interest, whereas low, are often non permanent. This implies your introductory fee will seemingly enhance after the promotional interval is over. Purpose to repay the vast majority of your debt earlier than this occurs to benefit from your stability switch.

Search out debt consolidation

With debt consolidation, you possibly can take a number of high-interest bank card balances and mix them right into a single mortgage with a doubtlessly decrease rate of interest. Simply preserve an eye fixed out for charges and penalties. Moreover, you’ll need to overview the mortgage phrases and restrictions to see if the compensation timeline is appropriate in your wants.

Lengthy-term advantages of a decrease rate of interest

It’s no secret {that a} decrease rate of interest is favorable and should give you some debt aid. It saves you cash while you’re paying off bank card debt. Nonetheless, for these with important bank card debt, a decrease rate of interest might also let you repay your debt sooner. This, in flip, saves you more cash in curiosity over time and means that you can see an enchancment in your credit score and monetary standing sooner.

Bear in mind to keep up good credit score administration even after you’ve scored a decrease rate of interest and paid down your debt. On-time funds, low credit score utilization and a protracted credit score historical past are all essential issues to remember.

Your first step to credit score restore

Regardless of good credit score administration, errors are surprisingly widespread in credit score experiences, which might trigger your credit score to dip for unfair causes. Study how Lexington Legislation Agency’s credit score restore companies may help you tackle these questionable destructive gadgets and get you on monitor for the credit score you deserve.

Notice: Articles have solely been reviewed by the indicated lawyer, not written by them. The knowledge offered on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation; as an alternative, it’s for basic informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or assets contained throughout the website don’t create an attorney-client or fiduciary relationship between the reader, consumer, or browser and web site proprietor, authors, reviewers, contributors, contributing corporations, or their respective brokers or employers.