{kind=link}

Powerful Love

This week’s CPI report served up powerful love for each bulls and hopeful doves. The rally that took us again above 4,000 on the S&P 500 was put to a painful finish on Tuesday, when the S&P fell 4.3% and the Nasdaq tumbled 5.2% on the heels of hotter-than-expected inflation. The issue is that it wasn’t simply hotter on one metric — it was hotter on the headline quantity, the core quantity, and when measured month-over-month and year-over-year.

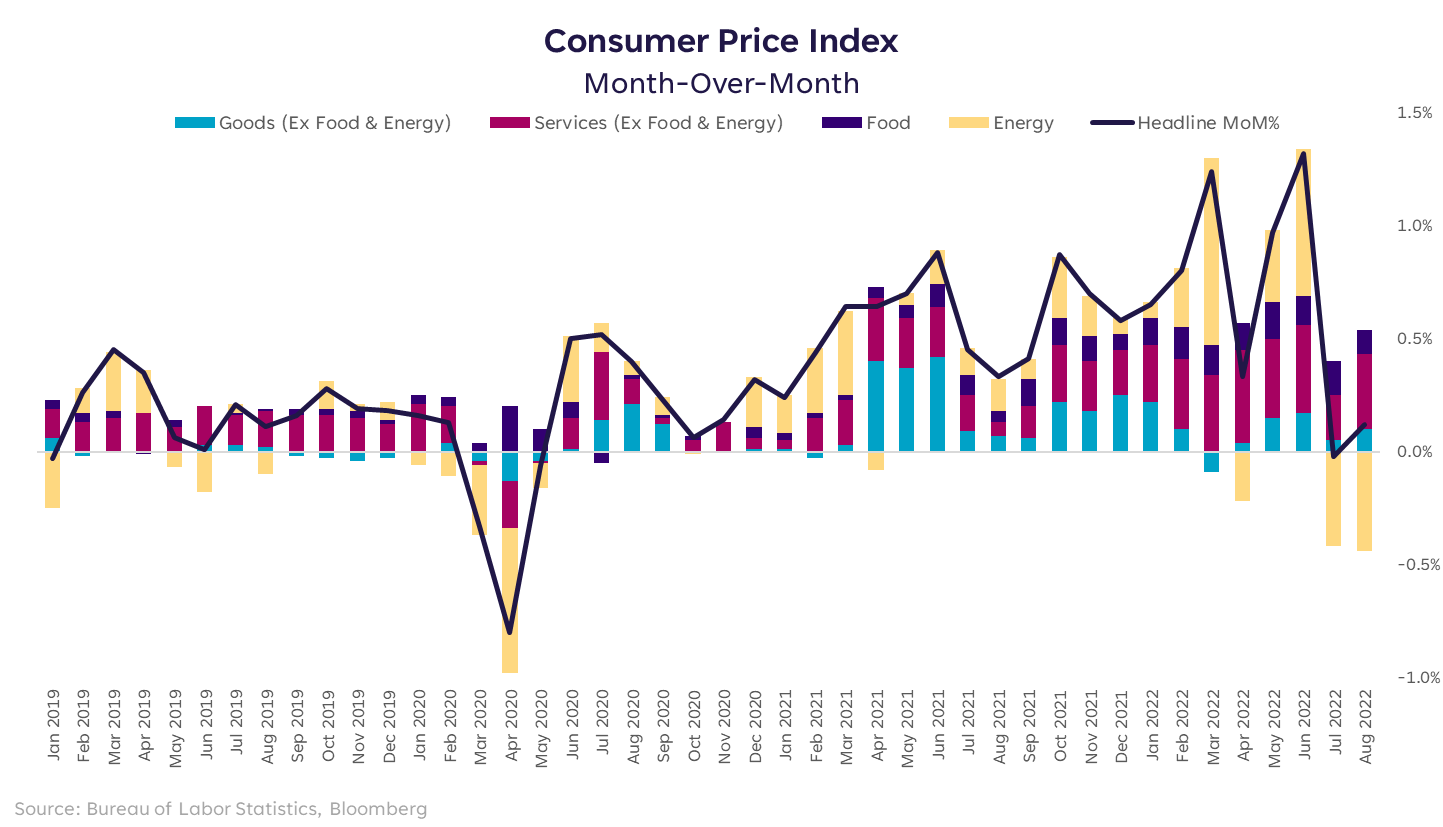

The actual star of the “powerful love” present was the month-over-month (m/m) change. Based on estimates, this month was anticipated to be the primary the place CPI would put up a adverse m/m studying since Might 2020. As an alternative, we acquired a constructive 0.1%.

It’s Not Me, It’s You

It’s not power, it’s providers. The optimism a couple of cooler inflation report was pushed by the truth that power and gasoline costs have fallen considerably within the final three months. WTI Crude Oil is down 28% over that interval and the common price of gasoline within the U.S. is down over 26%. The chart above depicts the power (yellow) element pulling the general studying down.

However a rise in providers inflation gained the combat this time. Specifically, the issue spot that’s lastly rising within the knowledge is housing, which falls below providers on this methodology. We’ve identified for a while that housing affordability is low and that residence costs and hire ranges have skyrocketed. We additionally know that they haven’t began to return down in a significant manner, and that it takes longer for housing market indicators to make their manner into these headline numbers. And right here we’re.

All people Hurts

For these of you who’re youthful than I’m, “All people Hurts” is a 90s tune by a band referred to as R.E.M., and it’s not quick on unhappy lyrics.

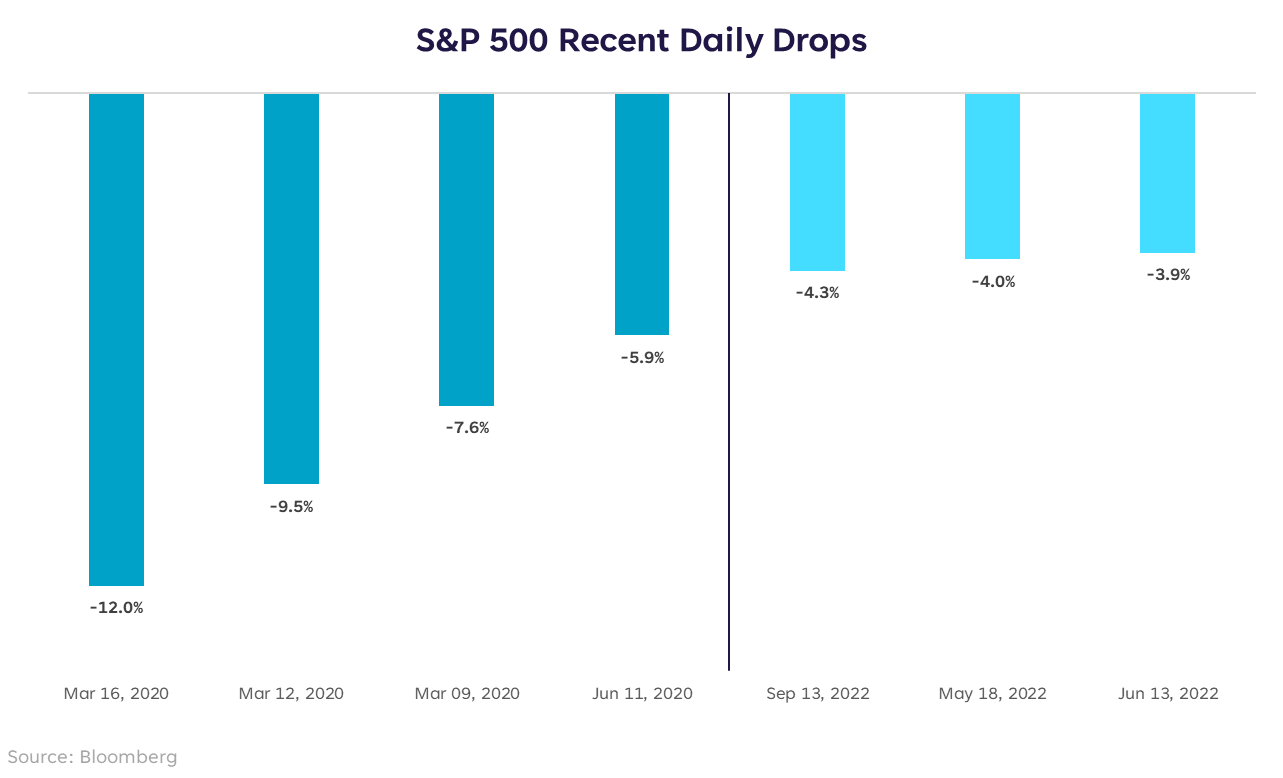

On Tuesday, we noticed the worst one-day drop within the S&P since June 2020. I can’t assist however assume it was a pivotal day, whether or not it was the belief that sticky inflation would require extra ache to repair, or just the start of one other valuation flush that might take us right down to prior lows. There’s additionally the likelihood it is going to seem like an overreaction in a pair months.

In any occasion, I believe we’ll speak about that day for some time, but it surely’s necessary to place it in perspective. A 4.3% every day drop was giant by any requirements, however nonetheless not almost as giant as what we noticed within the depths of Covid when uncertainty was at its peak and the market actually wasn’t functioning because it ought to.

I don’t need to reduce it although. September and October could be powerful months for markets and this yr appears like no exception. Provided that we now have a Fed assembly looming within the subsequent week, and will probably be one the place they publish a brand new dot plot and abstract of financial projections, there could possibly be extra one-day flushes to return. These pesky excessive inflation prints could possibly be foreshadowing a extra hawkish dot plot, and better projections for inflation, unemployment, and the Fed Funds Charge.

The persistently hawkish stance and messaging by the Fed leads me to consider that markets may even see a couple of extra every day stabs downward that proves to be a ultimate huge flush. This will sound odd, but when that occurs swiftly, which means inside the subsequent couple months, that truly turns into the bull case for my part. It could possibly be a fast and painful drop, leading to a renewed transfer increased later within the yr that’s extra sturdy, as inflation falls extra notably. After all, nobody is aware of precisely what is going to occur or when, however on days when everyone hurts, I are likely to consider that the top of ache comes nearer into view.

Please perceive that this info supplied is basic in nature and shouldn’t be construed as a advice or solicitation of any merchandise provided by SoFi’s associates and subsidiaries. As well as, this info is on no account meant to supply funding or monetary recommendation, neither is it supposed to function the premise for any funding determination or advice to purchase or promote any asset. Remember the fact that investing entails threat, and previous efficiency of an asset by no means ensures future outcomes or returns. It’s necessary for buyers to think about their particular monetary wants, targets, and threat profile earlier than investing determination.

The knowledge and evaluation supplied by means of hyperlinks to 3rd get together web sites, whereas believed to be correct, can’t be assured by SoFi. These hyperlinks are supplied for informational functions and shouldn’t be seen as an endorsement. No manufacturers or merchandise talked about are affiliated with SoFi, nor do they endorse or sponsor this content material.

Communication of SoFi Wealth LLC an SEC Registered Funding Adviser

SoFi isn’t recommending and isn’t affiliated with the manufacturers or corporations displayed. Manufacturers displayed neither endorse or sponsor this text. Third get together emblems and repair marks referenced are property of their respective house owners.

Communication of SoFi Wealth LLC an SEC Registered Funding Adviser. Details about SoFi Wealth’s advisory operations, providers, and charges is about forth in SoFi Wealth’s present Kind ADV Half 2 (Brochure), a duplicate of which is on the market upon request and at www.adviserinfo.sec.gov. Liz Younger is a Registered Consultant of SoFi Securities and Funding Advisor Consultant of SoFi Wealth. Her ADV 2B is on the market at www.sofi.com/authorized/adv.

SOSS22091504