{kind=link}

Nonetheless Between the Uprights

In celebration of the begin to the NFL’s common season this week, please humor my soccer analogies and shameless plug for the Inexperienced Bay Packers…#gopackgo (that was it, that’s the plug).

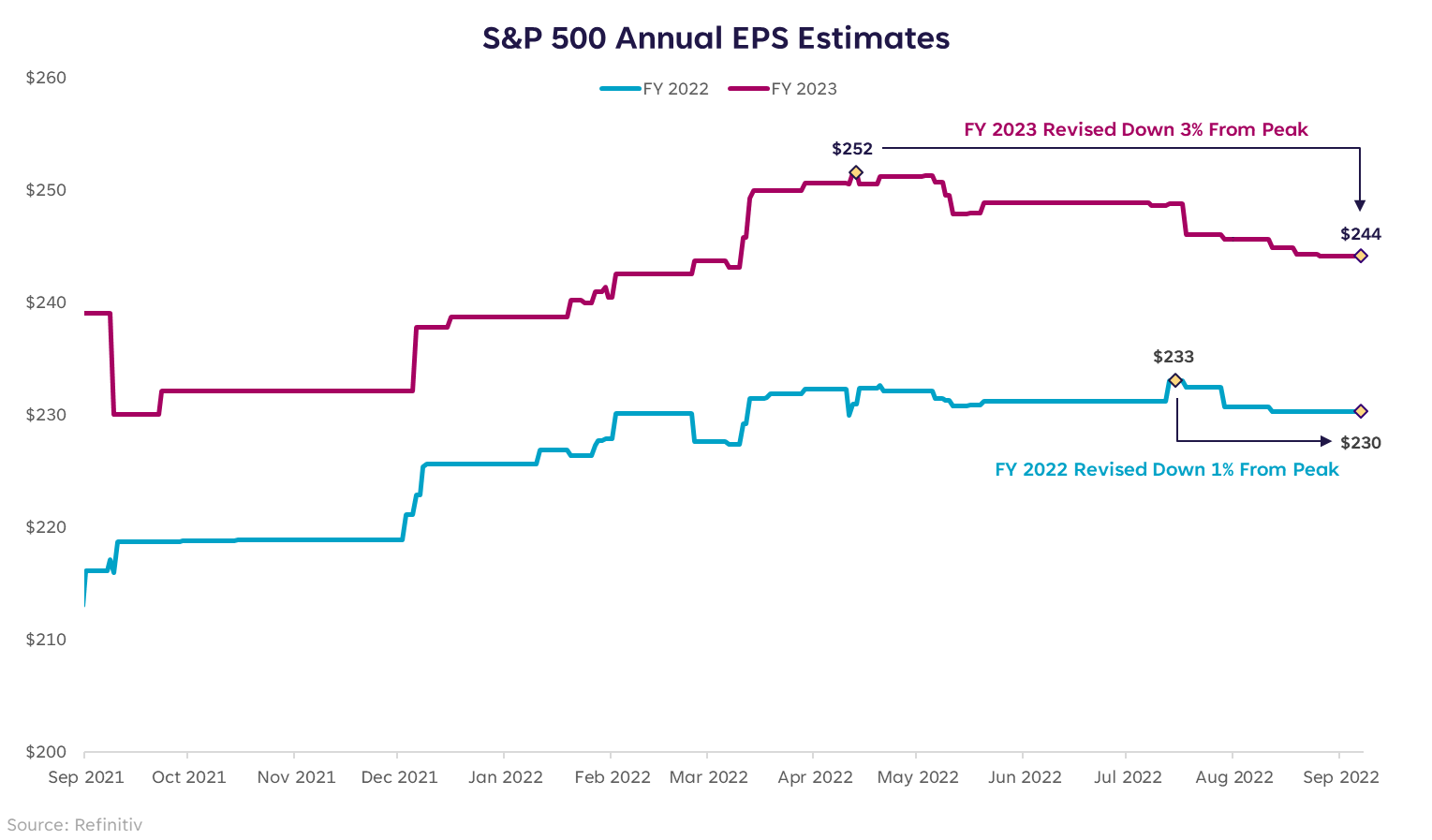

After many months of market pundits (self included) warning everybody about downward earnings revisions that have been looming giant, to this point not a lot has transpired. As of this writing, 2022 S&P 500 earnings per share (EPS) are anticipated to be $230, down just one% from their peak. Likewise, 2023 S&P EPS are anticipated to be $244, down solely 3% from their peak.

These revisions are a far cry from the punch within the intestine many feared. Some may argue {that a} 24% peak-to-trough decline within the S&P, like we noticed within the first half of this yr, foretells a punch within the intestine that simply hasn’t occurred but. And which may be true. However for now, the scoreboard nonetheless says the sport isn’t over.

Tied on the Half

Let’s say one staff is “no recession” and the opposite staff is “recession.” Every finish zone is labeled accordingly. I’d at the moment put us with a tie rating at halftime. The following critically necessary issue that may resolve the place the ball finally ends up is whether or not or not these unfavourable earnings revisions come to be.

However how unfavourable is unfavourable?

Some downward transfer in earnings will be absorbed by the truth that S&P corporations are working record-high revenue margins. It’s the bigger downward revisions that line-up with these seen in prior recession intervals that will sign recession within the close to future — particularly when coupled with a market that’s both approaching or already in bear market territory. (Notice: as of shut on Sept 7, the S&P is down 18% peak-to-trough — dangerously near the “bear” definition of -20% or extra).

Throughout recessions, the typical peak-to-trough decline in trailing 12-month earnings is roughly 30%. Not each recession sees that steep of a drop. Some are far more shallow (-4.6% in 1980) and a few are far more extreme (-91.9% from 2007-2009). There isn’t any magic degree that claims “that is recessionary,” however earnings would wish to return down markedly from right here with the intention to turn out to be a recession sign, for my part. Specifically, if 2023 EPS are revised down by 10-15% or extra, it could be troublesome for us to avert recession.

Pump Pretend?

As a lot as I need to be constructive, the present circumstances are such that being too constructive runs the chance of sounding like a pollyanna. September is traditionally a troublesome month for markets, we’ve solely seen one month of cooling in CPI, quantitative tightening accelerates this month, the S&P is once more approaching bear market territory, and the following Fed assembly is simply two weeks away.

Add these parts to the truth that inflation this excessive has by no means been “mounted” with out a recession and also you see why many are bearish. However as Stanford professor Scott Sagan as soon as stated, “Issues which have by no means occurred earlier than occur on a regular basis.” That quote is what begins chapter 12 of the e book The Psychology of Cash by Morgan Housel. It presents the concept that historical past is usually a poor information to the longer term as a result of occasions have modified, and the market buildings in place as we speak are totally different from the market buildings that have been in place 25-50 years in the past.

Was this latest rally only a pump faux? Maybe. If we’re headed to the “recession” finish zone, the market is more likely to see extra draw back and probably new lows. But when we’re headed for the “no recession” finish zone, the playbook appears to be like totally different, and far more constructive. Keep nimble, construct your bench, and take the sport one play at a time. And bear in mind, the worst staff from final yr will get first decide within the draft. Even within the worst of occasions, there’s a possibility to select up winners.

Please perceive that this info supplied is normal in nature and shouldn’t be construed as a suggestion or solicitation of any merchandise provided by SoFi’s associates and subsidiaries. As well as, this info is under no circumstances meant to supply funding or monetary recommendation, neither is it meant to function the premise for any funding determination or suggestion to purchase or promote any asset. Understand that investing entails threat, and previous efficiency of an asset by no means ensures future outcomes or returns. It’s necessary for buyers to think about their particular monetary wants, objectives, and threat profile earlier than investing determination.

The data and evaluation supplied by means of hyperlinks to 3rd celebration web sites, whereas believed to be correct, can’t be assured by SoFi. These hyperlinks are supplied for informational functions and shouldn’t be considered as an endorsement. No manufacturers or merchandise talked about are affiliated with SoFi, nor do they endorse or sponsor this content material.

Communication of SoFi Wealth LLC an SEC Registered Funding Adviser

SoFi isn’t recommending and isn’t affiliated with the manufacturers or corporations displayed. Manufacturers displayed neither endorse or sponsor this text. Third celebration logos and repair marks referenced are property of their respective house owners.

Communication of SoFi Wealth LLC an SEC Registered Funding Adviser. Details about SoFi Wealth’s advisory operations, providers, and charges is ready forth in SoFi Wealth’s present Type ADV Half 2 (Brochure), a replica of which is accessible upon request and at www.adviserinfo.sec.gov. Liz Younger is a Registered Consultant of SoFi Securities and Funding Advisor Consultant of SoFi Wealth. Her ADV 2B is accessible at www.sofi.com/authorized/adv.

SOSS22090801