{kind=link}

So I’ve had this write-up concept on my desktop computer considering that November 2024. It was a vacant Word file merely labelled “LLPA-free re-finance.”

It was something I was considering for a very long time because usually a price and term re-finance won’t pencil (make good sense economically) unless there’s a specific rates of interest discount rate.

As an example, if you can just decrease your existing home mortgage price by say 0.25% or 0.50%, there’s a good possibility it won’t make good sense.

Among the concerns with traditional finance (Fannie/Freddie) re-finances is they’re subject to loan-level cost modifications (LLPA), which can lead to a price a lot greater than the par price.

Because Of This, what might have been an excellent finance that reduces an existing property owner’s month-to-month repayment is never ever sought. Quickly that might transform…

LLPA-Free Refinance Can Alleviate Home Mortgage Repayments and Reduced Default Danger

Go into the LLPA-free re-finance, which I’ve contemplated considering that the price situation held and home mortgage prices virtually tripled.

Once they started to alleviate, there was an excellent possibility for current home customers to decrease their prices and obtain some repayment alleviation.

Doing so would certainly likewise lead to reduced default threats as a reduced repayment normally suggests the finance is much more inexpensive and likelier to execute.

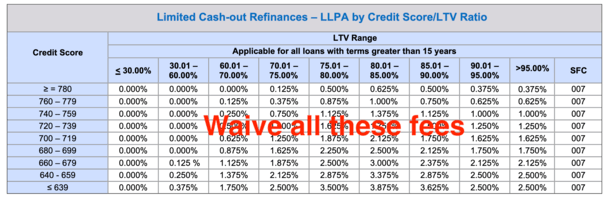

In spite of that, price and term refinances undergo great deals of prices hits, the most significant being for credit rating.

Notably, these LLPAs put on finances backed by Fannie Mae and Freddie Mac, yet out federal government home loans such as FHA finances, VA finances, and USDA finances.

Since these charges exist, a current home purchaser could not have the ability to benefit from the reduced prices available without going through expensive modifications.

Completion outcome could be handing down the re-finance possibility since it simply doesn’t make good sense economically.

Just How Much Could Debtors Conserve Without LLPAs on a Price and Term Refinance?

Allow’s take into consideration an instance. A current home purchaser with a 690 FICO rating would certainly undergo a 2.25% prices pinch hit credit rating at 80% loan-to-value proportion (LTV).

While it can differ, 1% in charge could relate to something like 0.25% to 0.375% in price.

Simply put, if their price with the charge was 6.375%, possibly maybe 6% without the charge.

And bear in mind, all a price and term re-finance does (disallowing an item adjustment) is reduced the month-to-month repayment.

So such a customer would certainly be kipping down a riskier finance for a lower-risk finance using a reduced month-to-month repayment.

That need to be interesting Fannie Mae and Freddie Mac and capitalists as well, that might presume the finance will certainly be held much longer and not pre paid swiftly.

Rather, since the LLPAs do use, the debtor could be informed the very best they can obtain is 6.375%.

If their existing price is 6.875% or 7%, they might identify that it’s simply ineffective to re-finance.

LLPAs Forgoed on Home Acquisition Funding Yet Out the Refi

Making issues worse is some home customers obtain their LLPAs totally forgoed for a home acquisition finance, yet they aren’t forgoed for a succeeding re-finance.

Because Of This, it’s much more tough to obtain the re-finance to pencil and make good sense for the debtor.

They’re primarily incentivized on the home acquisition, yet after that sort of embeded the finance, also if home mortgage prices boost.

There are likewise those with reduced FICO ratings that undergo huge LLPAs, in spite of just wishing to decrease their repayment and obtain some alleviation.

As an example, a customer with a 650 FICO at 80% LTV would certainly be struck with a 2.875% charge.

If we convert that charge right into price, it could relate to 0.75% or even more. So rather than 6%, they could be informed 6.75% is the very best they can obtain.

Once More, if their existing rates of interest is 7%, possibilities are they won’t seek the 6.75% price.

Yet if they might prevent that large prices hit and obtain the 6% price, suddenly we’re speaking some healthy and balanced financial savings.

On a $500,000 finance quantity, a price of 6% would certainly be $2,997.75 each month vs. a regular monthly repayment of $3,326.51 for a price of 7%.

That’s approximately $330 in financial savings each month if the debtor can obtain the LLPA-free re-finance.

And once more, that’s a much safer finance for all included since the property owner is paying $330 much less each month.

It’s a Good Sense Concept That Can Lower Home Mortgage Fees Without Treatment

It feels like a quite good sense concept to make the real estate market more secure and secure it from home mortgage misbehaviors and ultimate repossession.

The bright side is America’s Cooperative credit union, the Independent Area Bankers of America, and the Home Mortgage Bankers Organization have all presented such a concept today.

In a letter to Kevin Hassett, the supervisor of the National Economic Council of the USA, they appealed for this adjustment.

The one caution is you’d require an existing GSE-loan (backed by Fannie Mae or Freddie Mac) and a “solid repayment background,” which they specified as no late repayments in the previous 12 or 18 months.

In the very same letter, they asked for “decently decreasing LLPAs across-the-grid for acquisition finances” too.

This might make home purchasing less expensive as well and obtain home mortgage prices reduced without the requirement for megabytes acquiring or reduced bond returns or even more QE and Fed treatment.

It in fact makes a great deal of feeling to me so with any luck it’s something they’ll take into consideration.

It’d absolutely cause a rise in re-finance applications and great deals of financial savings for American property owners.

Continue Reading: Exactly how does home mortgage refinancing job?

Prior to developing this website, I functioned as an account exec for a wholesale home mortgage loan provider in Los Angeles. My hands-on experience in the very early 2000s influenced me to start discussing home loans 19 years ago to aid possible (and existing) home customers much better browse the home mortgage procedure. Follow me on X for warm takes.