{kind=link}

When you’re fascinated by shopping for a house, or refinancing an present house mortgage, mortgage charges are doubtless prime of thoughts.

As you could or could not know, mortgage charges can change day by day primarily based on market circumstances, much like the inventory market.

This implies they are often increased in the future and decrease the following. Or they could do subsequent to nothing in any respect from daily, and even week to week.

However having an concept of which path they’re going may be useful, particularly if you happen to’re actively buying your charge.

Let’s focus on a easy technique to monitor mortgage charges utilizing available financial knowledge.

You Can Observe Mortgage Charges Utilizing the 10-Yr Bond Yield

- Merely lookup the 10-year bond yield in your favourite finance web site

- Examine the path it’s going (such as you would a inventory ticker)

- If it’s up then mortgage charges will doubtless be increased than yesterday

- If it’s down then mortgage charges will doubtless be decrease than yesterday

Fingers down, the only technique to monitor mortgage charges is the 10-year treasury bond yield.

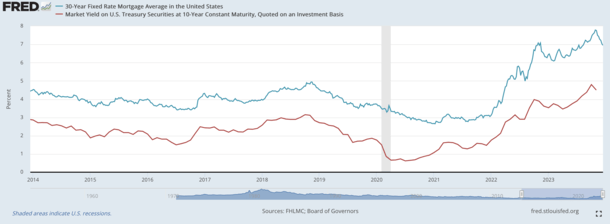

Over time, mortgage charges and the 10-year yield have moved in close to lockstep, as seen within the graph above from FRED.

In different phrases, when 10-year yields fall, so do mortgage charges. And when yields rise, mortgage charges climb increased.

As for why, many 30-year fastened mortgages are paid off in a couple of decade. This implies the length is much like a 10-year bond.

However as a result of mortgages have prepayment danger, there’s a “unfold,” or premium that’s paid to buyers of related mortgage-backed securities (MBS), that are additionally bonds.

This unfold is the distinction between the going 30-year fastened mortgage charge and the 10-year yield.

For a very long time, it hovered round 170 foundation factors. This meant if a 10-year bond was yielding 3.00%, a 30-year fastened mortgage could be priced round 4.70%. Or maybe 4.75%.

So in an effort to monitor mortgage charges, you merely needed to lookup the 10-year yield and add this unfold. You then’d have a ballpark value for mortgage charges.

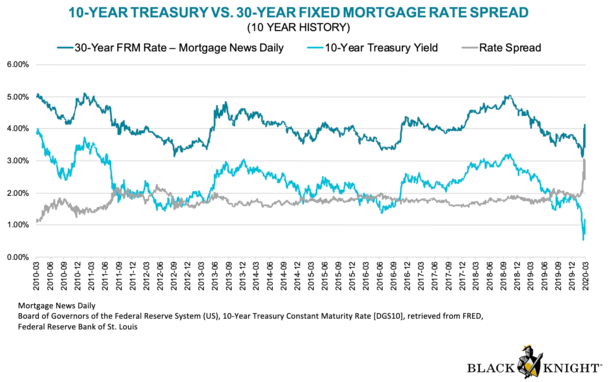

Mortgage Charge Spreads Have Widened, However the 10-Yr Bond Yield Is Nonetheless Related for Monitoring the Course of Charges

Not too long ago, mortgage charge spreads widened significantly as a consequence of financial uncertainty, heightened prepayment danger, out-of-control inflation, and different elements.

At one level, the unfold was greater than 300 foundation factors, or roughly double the norm, as seen within the chart above. This made monitoring a bit tougher, however the path of yields and charges was nonetheless related.

So although the spreads have been wider, if the 10-year yield went up on a given day, mortgage charges doubtless elevated as properly. Or vice versa.

This implies you’ll be able to nonetheless lookup the 10-year bond yield and decide which method mortgage charges will go that day.

If yields are up, mortgage charges will doubtless be up too. If yields are down, there’s a superb likelihood mortgage charges shall be down additionally.

The identical goes for magnitude of change. If yields plummet, mortgage charges also needs to enhance rather a lot. But when yields surge increased, be careful for a lot increased charges.

Now again to these extensive spreads. Over the previous 18 months or so, the Fed has been battling inflation with 11 charge hikes by way of their very own federal funds charge.

However now that the Fed has indicated that their subsequent transfer may very well be a charge lower, and that inflation could have peaked, there’s much more calm within the markets.

As such, spreads have come again all the way down to round 270 foundation factors. Whereas nonetheless ~100 bps increased than regular, it’s moderating.

And once more, we are able to nonetheless guess path whatever the unfold being wider than ordinary.

MBS Costs Are Even Extra Correct Than 10-Yr Bond Yields When Monitoring Mortgage Charges

A mortgage charge purist will inform you that the 10-year bond is a superb benchmark to trace mortgage charges. However that taking a look at precise MBS costs is healthier.

That is true as a result of MBS costs straight impression mortgage charge motion. So if MBS costs fall on a given day, mortgage charges will rise.

Bear in mind, when the value of a mortgage bond falls, as a consequence of much less demand, its yield, aka rate of interest, will increase.

As such, if you need mortgage charges to go down, you’ll be rooting for MBS costs to extend. They usually’ll improve if demand is powerful, thereby pushing yields down.

Now the query is how do you go about monitoring MBS costs?

Whilst you can monitor the 10-year bond yield on Yahoo Finance (as seen above), Google Finance, Marketwatch, CNBC, you identify it, MBS value knowledge isn’t as available.

Nevertheless, Mortgage Information Every day does a superb job of posting day by day MBS costs on its web site.

They record each UMBS for Fannie Mae and Freddie Mac (conforming mortgages) and Ginnie Mae (GNMA) MBS for FHA loans and VA loans.

When you’re curious if mortgage charges are up or down on a given day, head over there and have a look at MBS costs.

Bear in mind, if MBS costs are down, mortgage charges shall be increased. And if MBS costs are up, mortgage charges shall be decrease.

To sum issues up, monitoring mortgage charges isn’t too troublesome. Merely lookup the 10-year yield every morning and likewise take a look at MBS costs.

From there you’ll have a reasonably good concept of whether or not they’re going to be increased or decrease than the day gone by.

Now relating to predicting them, that’s one other story altogether…

Learn extra: 2024 Mortgage Charge Predictions

(Picture: fdecomite)