{kind=link}

A have a look at mortgage charge historical past

There’s no query that mortgage charges have risen in 2022. Thirty-year charges tipped above 5% in April for the primary time in a decade. And between June 9 and June 16 alone, they rose by 55 foundation factors (0.55%) — the biggest one-week improve since 1987.

If there’s a silver lining, it’s that mortgage charges are nonetheless comparatively low from a historic standpoint. Traditionally, 30-year mounted charges have averaged slightly below 8 %. So although at present’s charges are hovering above 5%, they’re nonetheless a superb deal comparatively.

Discover your lowest mortgage charge. Begin right here (Jul seventeenth, 2022)

On this article (Skip to…)

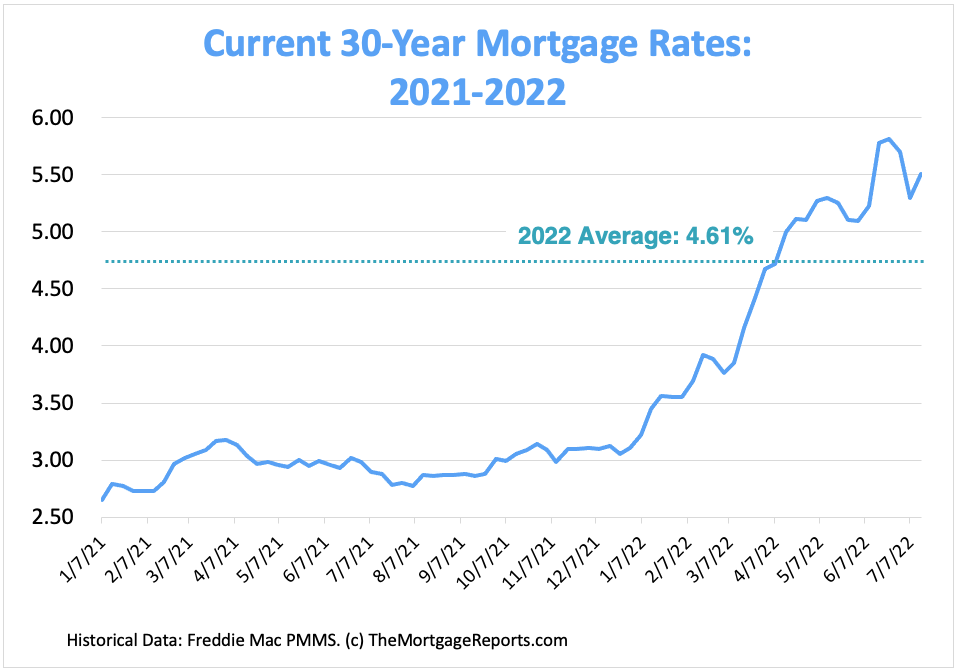

30-year mortgage charges chart: The place are charges now?

Mortgage rates of interest fell to file lows in 2020 and 2021 through the Covid pandemic.

Emergency actions by the Federal Reserve helped to push mortgage charges beneath 3% and maintain them there.

However with inflation surging to 41-year highs, mortgage rates of interest have risen in 2022. And coverage tightening by the Fed is prone to push them increased nonetheless.

Those that are able to lock an rate of interest sooner quite than later could also be sensible to take action.

Present mortgage rates of interest chart

Chart represents weekly averages for a 30-year fixed-rate mortgage. Supply: Freddie Mac

Discover your lowest mortgage charge. Begin right here (Jul seventeenth, 2022)

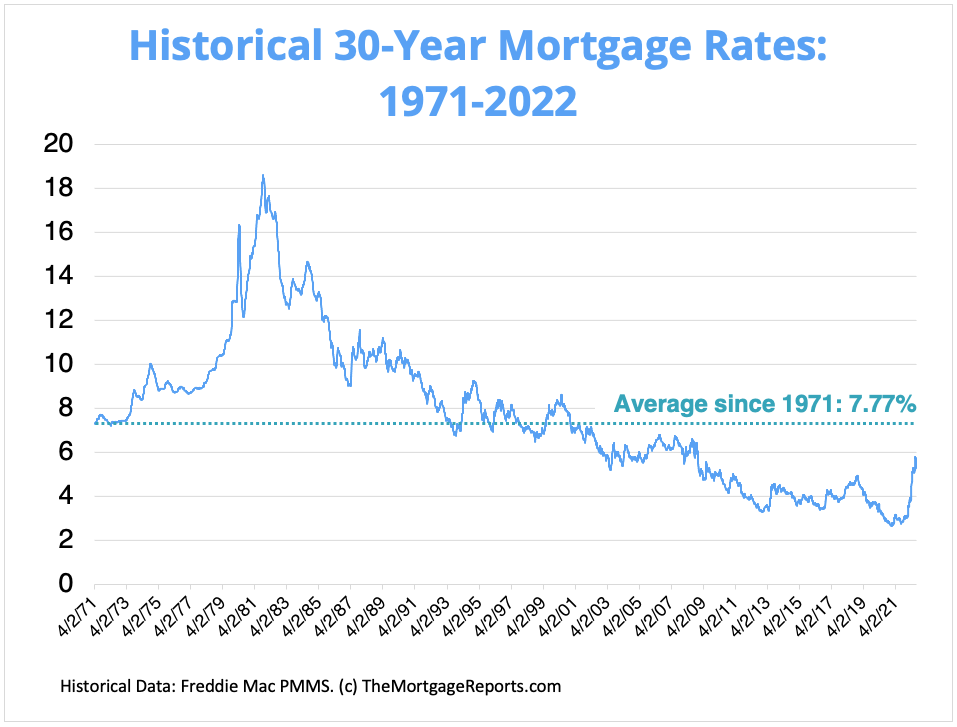

Historic mortgage charges chart

Regardless of current rises, at present’s 30-year mortgage charges are nonetheless beneath common from a historic perspective.

Freddie Mac — the primary business supply for mortgage charges — has been maintaining data since 1971.

Between April 1971 and June 2022, 30-year mortgage charges averaged 7.77 %. So even with the 30-year FRM above 5%, charges are nonetheless comparatively inexpensive in comparison with historic mortgage charges.

Historic 30-year mortgage charges chart

Chart represents weekly averages for a 30-year fixed-rate mortgage. Supply: Freddie Mac

Mortgage charge tendencies over time

For some perspective on at present’s mortgage rates of interest, right here’s how common 30-year charges have modified from 12 months to 12 months over the previous 5 a long time.

| Yr | Common 30-Yr Price | Yr | Common 30-Yr Price | Yr | Common 30-Yr Price |

| 1974 | 9.19% | 1990 | 10.13% | 2006 | 6.41% |

| 1975 | 9.05% | 1991 | 9.25% | 2007 | 6.34% |

| 1976 | 8.87% | 1992 | 8.39% | 2008 | 6.03% |

| 1977 | 8.85% | 1993 | 7.31% | 2009 | 5.04% |

| 1978 | 9.64% | 1994 | 8.38% | 2010 | 4.69% |

| 1979 | 11.20% | 1995 | 7.93% | 2011 | 4.45% |

| 1980 | 13.74% | 1996 | 7.81% | 2012 | 3.66% |

| 1981 | 16.63% | 1997 | 7.60% | 2013 | 3.98% |

| 1982 | 16.04% | 1998 | 6.94% | 2014 | 4.17% |

| 1983 | 13.24% | 1999 | 7.44% | 2015 | 3.85% |

| 1984 | 13.88% | 2000 | 8.05% | 2016 | 3.65% |

| 1985 | 12.43% | 2001 | 6.97% | 2017 | 3.99% |

| 1986 | 10.19% | 2002 | 6.54% | 2018 | 4.54% |

| 1987 | 10.21% | 2003 | 5.83% | 2019 | 3.94% |

| 1988 | 10.34% | 2004 | 5.84% | 2020 | 3.10% |

| 1989 | 10.32% | 2005 | 5.87% | 2021 | 2.96% |

Supply: Freddie Mac

Can 30-year mortgage charges go decrease?

The quick reply is that mortgage charges may all the time go decrease. However you shouldn’t anticipate them to.

With inflation at 40-year highs and the Federal Reserve making aggressive charge hikes to fight it, mortgage charges appear prone to rise within the close to future. Keep in mind that the Fed doesn’t set mortgage charges, however these charges usually comply with the identical basic development as the general market.

That mentioned, charges have been extra unstable currently as a result of recession fears and we’ve seen some drops in current weeks.

As all the time, charges transfer unpredictably and it’s robust to time the market — particularly with so many unknowns about the place the financial system is at present headed. Residence patrons are usually higher off shopping for after they’re financially prepared whatever the charge market.

Keep in mind that you’re not caught with a mortgage charge endlessly. If charges drop considerably, householders can all the time refinance in a while to chop prices.

Mortgage charge predictions for 2022

On the time of this writing (July 2022), inflation within the U.S. was at a four-decade excessive. And the Federal Reserve was enacting aggressive charge hikes to attempt to tame it. These and different crimson flags had many patrons frightened about the opportunity of a recession and what it will imply for the housing market.

Whereas the Fed’s actions are at present nudging mortgage charges increased, the other is also true. If the Federal Reserve manages to get inflation underneath management, mortgage charge progress might finally cool off as nicely.

However there are lots of unknowns. And even when charges do cool off, debtors shouldn’t anticipate them to drop again into the file low, 2-3% territory seen over the previous two years. These historic mortgage charges have been as a result of distinctive circumstances — specifically, the coronavirus pandemic — and solely a large, sudden financial downturn may deliver charges again to such lows.

Historic mortgage charges: Essential years for charges

The lengthy–time period common for mortgage charges is slightly below 8 %. That’s based on Freddie Mac data going again to 1971.

However mortgage charges can transfer quite a bit from 12 months to 12 months — even from day after day. And a few years have seen a lot larger strikes than others.

Let’s have a look at a couple of examples to point out how charges usually buck standard knowledge and transfer in sudden methods.

1981: The all-time excessive for mortgage charges

1981 was the worst 12 months for mortgage rates of interest on file.

How unhealthy is unhealthy? The typical mortgage charge in 1981 was 16.63%.

- At 16.63% a $200,000 mortgage has a month-to-month value for principal and curiosity of $2,800

- In contrast with the long-time common that’s an additional month-to-month value of $1,300 or $15,900 per 12 months

And that’s simply the typical — some individuals paid extra.

For the week of Oct. 9, 1981, mortgage charges averaged 18.63%, the best weekly charge on file, and virtually 5 occasions the 2019 annual charge.

2008: The mortgage droop

2008 was the ultimate gasp of the mortgage meltdown.

Actual property financing was accessible in 2008 for six.03% based on Freddie Mac.

- The month-to-month value for a $200,000 mortgage was about $1,200 per 30 days, not together with taxes and insurance coverage

Put up 2008, charges declined steadily.

2016: An all-time low for charges

Till not too long ago, 2016 held the bottom annual mortgage charge on file going again to 1971. Freddie Mac says the standard 2016 mortgage was priced at simply 3.65%.

- A $200,000 mortgage at 3.65% has a month-to-month value for principal and curiosity of $915

- That’s $553 a month lower than the long-term common

Mortgage charges had dropped decrease in 2012, when one week in November averaged 3.31%. However a few of 2012 was increased, and the complete 12 months averaged out at 3.66% for a 30-year mortgage.

2019: The shock mortgage charge drop-off

In 2018, many economists predicted that 2019 mortgage charges would high 5.5%. That turned out to be fallacious.

In truth, charges dropped in 2019. The typical mortgage charge went from 4.54% in 2018 to three.94% in 2019.

- At 3.94% the month-to-month value for a $200,000 dwelling mortgage was $948

- That’s a financial savings of $520 a month — or $6,240 a 12 months — in comparison with the 8% lengthy–time period common

In 2019, it was thought mortgage charges couldn’t go a lot decrease. However 2020 and 2021 proved that considering fallacious once more.

2021: The bottom 30-year mortgage charges ever

Charges plummeted in 2020 and 2021 in response to the Coronavirus pandemic.

By July 2020, the 30-year mounted charge fell beneath 3% for the primary time. And it saved falling to a brand new file low of simply 2.65% in January 2021.

- At 2.65% the month-to-month value for a $200,000 dwelling mortgage is $806 a month not counting taxes and insurance coverage

- You’d save $662 a month, or $7,900 a 12 months, in comparison with the 8% long-term common

Nevertheless, record-low charges have been largely depending on accommodating, Covid-era insurance policies from the Federal Reserve. These measures have been by no means meant to final. And the extra U.S. and world economies recuperate from their Covid droop, the upper rates of interest are prone to go.

2022: Mortgage charges spike

Due to sharp inflation progress, increased benchmark charges, and a downside on mortgage stimulus by the Fed, mortgage charges spiked within the first six months of 2022.

Based on Freddie Mac’s data, the typical 30-year charge jumped from 3.76% to five.78% between March 3 and June 16 — a rise of over 200 foundation factors (2.00%) in simply three months.

Charges may proceed to extend all year long. The place they’ll plateau, it’s inconceivable to say.

Components that have an effect on your mortgage rate of interest

For the typical homebuyer, monitoring mortgage charges helps reveal tendencies. However not each borrower will profit equally from at present’s low mortgage charges.

Residence loans are personalised to the borrower. Your credit score rating, down fee, mortgage sort, mortgage time period, and mortgage quantity will have an effect on your mortgage or refinance charge.

It’s additionally attainable to negotiate mortgage charges. Low cost factors can present a decrease rate of interest in alternate for paying money upfront.

Let’s have a look at a few of these components individually:

Credit score rating

A credit score rating above 720 will open extra doorways for low-interest-rate loans, although some mortgage packages comparable to USDA, FHA, and VA loans might be accessible to sub-600 debtors.

If attainable, give your self a couple of months or perhaps a 12 months to enhance your credit score rating earlier than borrowing. You might save 1000’s of {dollars} via the lifetime of the mortgage.

Down fee

Larger down funds can shave your borrowing charge.

Most mortgages, together with FHA loans, require a minimum of 3% or 3.5% down. And VA loans and USDA loans can be found with 0% down fee.

However for those who can put 10%, 15%, and even 20% down, you would possibly qualify for a standard mortgage with low or no non-public mortgage insurance coverage and severely scale back your housing prices.

Mortgage sort

The kind of mortgage mortgage you utilize will have an effect on your rate of interest. Nevertheless, your mortgage sort hinges in your credit score rating. So these two components are very intertwined.

For instance, with a credit score rating of 580 chances are you’ll qualify just for a government-backed mortgage comparable to an FHA mortgage. FHA loans have low rates of interest, however include mortgage insurance coverage irrespective of how a lot cash you set down.

A credit score rating of 620 or increased would possibly qualify you for a standard mortgage, and — relying in your down fee and different components — doubtlessly a decrease charge.

Adjustable-rate mortgages historically supply decrease introductory rates of interest in comparison with a 30-year fixed-rate mortgage. Nevertheless, these charges are topic to vary after the preliminary fixed-rate interval.

So an initially decrease ARM charge may rise considerably after 5, 7, or 10 years.

Mortgage time period

On this publish we’ve tracked charges for 30-year fixed-rate mortgages, however 15-year fixed-rate mortgages are likely to have even decrease borrowing charges.

With a 15-year mortgage, you’d have a better month-to-month fee due to the shorter mortgage time period. However all through the lifetime of the mortgage you’d save quite a bit in curiosity costs.

At a 3% rate of interest for a $200,000 dwelling mortgage, you’d pay $103,000 in curiosity costs with a 30-year mortgage paid off on schedule. A 15-year fixed-rate mortgage would value solely about $49,000 in curiosity.

Mortgage quantity

Charges on unusually small mortgages — a $50,000 dwelling mortgage, for instance — are usually increased than common charges as a result of these loans are much less worthwhile to the lender.

Charges on a jumbo mortgage mortgage are usually increased, too, as a result of lenders have a better threat of loss. Jumbo loans assist consumers purchase high-value actual property.

Low cost factors

A low cost level can decrease rates of interest by about 0.25% in alternate for upfront money. A reduction level prices 1% of the house mortgage quantity.

For a $200,000 mortgage, a reduction level would value $2,000 upfront. Nevertheless, the borrower would recoup the upfront value over time because of the financial savings earned by a decrease rate of interest.

Since curiosity funds play out over time, a purchaser who plans to promote the house or refinance inside a few years ought to most likely skip the low cost factors and pay a better rate of interest for some time.

Some charge quotes assume the house purchaser will purchase low cost factors, so make sure to verify earlier than closing on the mortgage.

Different mortgage prices to bear in mind

Keep in mind that your mortgage charge will not be the one quantity that impacts your mortgage fee.

While you’re estimating your property shopping for finances, you additionally have to account for:

- Down fee

- Closing prices

- Low cost factors (non-obligatory)

- Personal mortgage insurance coverage (PMI) or FHA mortgage insurance coverage premiums

- Householders insurance coverage

- Property taxes

- HOA dues (if shopping for in a householders affiliation)

Fortunately, whenever you get pre-approved, you’ll obtain a doc referred to as a Mortgage Estimate that lists all these numbers clearly for comparability.

Use your Mortgage Estimates to seek out one of the best total deal in your mortgage — not simply one of the best rate of interest.

You can even use a mortgage calculator with taxes, insurance coverage, and HOA dues included to estimate your complete mortgage fee and residential shopping for finances.

When to lock your mortgage charge

Keep watch over day by day charge adjustments. However for those who get a superb mortgage charge quote at present, don’t hesitate to lock it in.

Keep in mind, for those who can safe a 30-year mortgage charge at or beneath 6%, you’re paying lower than most American homebuyers all through historical past. That’s not a nasty deal.