The advantages of blockchain know-how are but to be realized in banking. Whereas some giant banks have business initiatives nothing has actually taken off but. A lot of that is because of regulatory uncertainty however many banks are actively participating and studying whereas we’re on this one thing of a holding interval.

Our subsequent visitor on the Fintech One-on-One podcast is Robert Morgan, the CEO of the USDF Consortium, a gaggle of banks making a blockchain-based system for tokenized deposits that may make banking safer, cheaper and extra dependable for shoppers (see their deck right here). Rob was once the top of innovation on the American Bankers Affiliation (we had him on the present again in 2017) and so he has a deep understanding of banking and know-how.

On this podcast you’ll study:

- Why Rob determined to make the leap from the ABA to the USDF Consortium.

- How he describes what USDF is strictly.

- How banks will use USDF and an outline of the funds move.

- The first advantages of USDF and the preferred use instances.

- How the programmability of USDF might be leveraged.

- Why USDF will probably be complementary to Fedwire and FedNow (when it launches).

- How the USDF Consortium, the Provenance Blockchain and Determine are associated.

- How they’re working with the Federal regulatory companies at the moment.

- Particulars of their response to Treasury’s RFC on digital belongings.

- How they view CBDCs and the way it might be complementary to what they’re constructing.

- The forms of banks which might be members of the consortium.

- The place they’re at in relation to USDF going dwell.

- The objections of banks who are usually not prepared to hitch the consortium.

- What Rob thinks the following transfer from regulators will probably be in relation to digital belongings.

- What the banking system may appear like in ten years time.

You possibly can subscribe to the Fintech One-on-One Podcast through Apple Podcasts or Spotify. To hearken to this podcast episode, there’s an audio participant immediately above or you’ll be able to obtain the MP3 file right here.

Obtain a PDF of the Transcription or Learn it Below

FINTECH ONE-ON-ONE PODCAST 385-ROBERT MORGAN

Welcome to the Fintech One-on-One podcast, Episode No. 385. That is your host, Peter Renton, Chairman and Co-Founding father of Fintech Nexus.

(music)

Earlier than we get began, I wish to let you know a few new occasion we’re internet hosting in London on October seventeenth and 18th referred to as Merge, it’s targeted on the intersection of conventional finance and Web3. Whatever the value of crypto tokens, the know-how being developed by Web3 startups has the potential to utterly remodel the monetary system. Our occasion will probably be bringing collectively leaders from Web3, fintech and conventional finance to debate how this transformation will happen. Discover out extra and register at fintechnexus.com.

Peter Renton: As we speak on the present, I’m delighted to welcome again Robert Morgan, he’s the CEO of the USDF Consortium. Final time on the present, a number of years in the past, when he was on the American Bankers Affiliation – he was head of innovation there – and so he’s actually obtained deep experience within the banking area, coping with Washington throughout innovation in banking, So now, he’s moved to USDF, which is the USDF Consortium, a membership group of banks so that they’re actually all about bringing banks the flexibility to mint tokenized deposits.

Now, we’ll clarify what which means: it’s all blockchain-based, we go into the know-how in some depth, we speak in regards to the totally different use instances, how the fee flows work, the way it’s going work with the Fed system, Fedwire and ACH. We speak about, you already know, the programmability of USDF and the thrilling items that may carry. We additionally speak about, you already know, the place the regulators stand, the place they stand with regulators, what these conversations are like with lawmakers as effectively, we speak about CBDCs and way more. It was an interesting episode, hope you benefit from the present.

Peter: Welcome again to the podcast, Rob!

Robert Morgan: Nice to be again, good to see you.

Peter: Sure, certainly. So, final time we had you on, a number of years again now, you had been with the American Bankers Affiliation, Head of Innovation there. So inform me, you clearly had a attention-grabbing job, you stayed there for fairly some time, however what was the driving pressure in shifting from the ABA to the USDF Consortium?

Rob: So, spent 11 years on the ABA and might’t say sufficient nice issues about that. The crew in ABA, the work that they do, actually loved and pleased with every thing we constructed there and over the time I used to be at ABA we noticed quite a lot of totally different tendencies, quite a lot of waves of disruption come by the business and in that point we noticed banking modernize an amazing quantity. However what I feel in the end has probably not panned out are the warnings of banks being disrupted and disintermediated and in lots of ways in which’s as a result of quite a lot of the fintech innovation that we’ve seen, it’s round how do you work together with what on the finish of the day is a reasonably conventional financial institution deposit and its new type components, new methods to have interaction. What we’re beginning to see now I feel is one thing that actually does increase that query of what is going to banks play in our economic system and I feel it’s actually essential to be sure that banks have the flexibility to proceed enjoying the essential function they do. So, what’s totally different at the moment and one of many explanation why the chance with USDF is so nice is we’re asking elementary questions on what does it imply to digitize cash and as we each know, the greenback actually is already digital at the moment, however what we’re speaking about is how can we tokenize cash, how can we leverage blockchain as the way in which to ship monetary providers.

The truth is that as we consider cash at the moment, we frequently consider money and as we take into consideration digital greenback conversations we take into consideration how are we transacting money, however the actuality is at the moment, 73% of cash is financial institution cash. It’s the legal responsibility of a personal establishment like a financial institution or a credit score union that’s mature, so 73% of that cash exists at the moment and in a type the place it will possibly assist energy lending that drives the economic system.

And so, as we glance ahead, at the moment we see a lot of choices that may put off that, whether or not it’s non-bank Stablecoins and even within the conversations round ought to the Federal Reserve problem a CBDC and one of many issues that USDF is doing is attempting to make sure is that as we take a look at the way forward for cash on blockchain, banks can play the identical function in that market that they do in each different and act in that very same intermediating function in being able to create credit score. So, I feel that’s a extremely essential query not only for the banking business, however for the economic system as we go ahead and I feel that is one of the simplest ways to assist affect that.

Peter: Proper, proper, that sounds truthful sufficient. I wish to dig into the CBDC factor in only a minute, however earlier than we do this I wish to simply get your description of what USDF is. Significantly, I imply, you had been in conventional banking for a very long time, I think about that you just’ve had quite a lot of questions on your transfer right here. How do you describe USDF say to somebody who actually doesn’t understand it very effectively that’s in conventional banking.

Rob: It’s a humorous query as a result of I feel there’s a lot buzz about crypto on the whole and there are such a lot of banks attempting to grasp what their technique is on crypto, what their technique is on blockchain and the place all the items match collectively. In some ways, now we have little or no to do with crypto itself and are extra targeted on blockchain so, you already know, on the finish of the day, we imagine blockchain generally is a extra environment friendly ledger for conventional monetary providers transactions. And so, once we speak to banks about what this implies for his or her enterprise, we are sometimes speaking about what ledger are you utilizing and the way can we make it extra environment friendly.

So, there was an period the place banking was carried out on paper ledgers that we moved to on-premise servers, now we’ve since moved to cloud-based servers. We expect blockchain generally is a extra environment friendly ledger as we glance in direction of the way forward for monetary providers and USDF is a crucial piece in making that attainable. USDF is a tokenized deposit so not a Stablecoin however a illustration of an current financial institution deposit on blockchain and what that does is permit banks to speak collectively on blockchain and be capable of carry a few of the innovation that we’ve seen born out of a crypto ecosystem into conventional monetary providers.

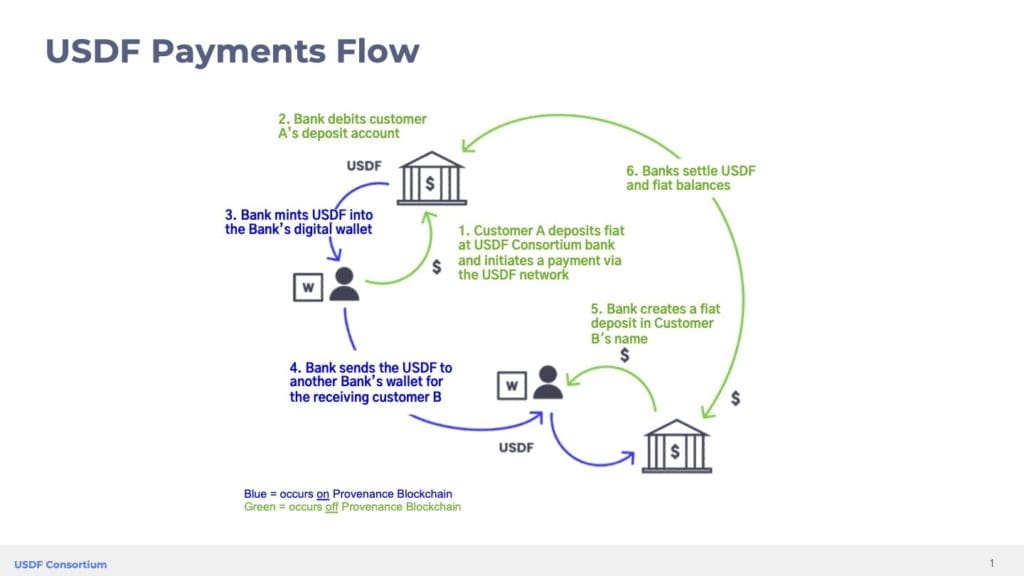

Peter: Perhaps let’s begin off with that fee move that you just simply touched on there. You might have a extremely nice slide that you just shared with me earlier than in our speak right here that describes the fee move. Perhaps you’ll be able to simply give us an instance of how does the fee move…..you talked about this, it isn’t a Stablecoin, it is a tokenized deposit, describe what which means within the context of this move.

Rob: In some ways, what we’re speaking about right here appears to be like much more from a move perspective like a messaging layer in conventional funds than it does a Stablecoin the place shoppers could purchase it by an trade transacted by their very own wallets and use it to both purchase or promote different items. Versus that, USDF is that illustration of a deposit on chain and what banks use it for is to speak with one another to impact funds in real-time in a blockchain-native method between the establishments.

So, the patron could by no means see USDF, they only see that the transaction occurs sooner, cheaper, extra effectively. What which means behind-the-scenes is {that a} financial institution will go on chain, they’ll take the cash that the client has instructed them to spend, whether or not it’s peer-to-peer, business-to-business, they’ll take the cash that the shoppers has instructed to spend, transfer it into an omnibus account and they’re going to then mint USDF below the Provenance blockchain and switch that USDF to a different establishment who will then burn the USDF and credit score their buyer’s account all in real-time. After we speak about that ledger what blockchain then facilitates is monitoring of these liabilities between these establishments all through the day. As we speak, these banks will in the end settle up with one another and that, on the finish of the day, through Fedwire.

Peter: Proper, okay, okay. So, give us examples of a few of the use instances that you just assume will probably be hottest and what you assume are the first advantages for utilizing USDF.

Rob: So, you already know, as everybody who talks about blockchain will say, the applicability is absolutely broad, there’s lots. We expect it is a new, extra environment friendly ledger, there are quite a lot of app units that may profit from it, however in the end, we’ll focus first on how can we have an effect on conventional funds after which we take into consideration this in two phases. The primary part is absolutely proving out that banks inside the 4 corners of the financial institution regulatory construction can transfer cash sooner, cheaper, extra effectively on chain so we’re on this first part targeted on these conventional bank-to-bank funds, issues like peer-to-peer funds, issues like business funds.

How can we make these extra environment friendly after which leverage a few of what blockchain brings to the desk as a few of the programmability so we will have smarter funds as we start integrating these. As soon as now we have confirmed out that these funds work, as soon as regulators are snug with that, we expect there’s a chance to carry different monetary providers belongings on chain, conventional belongings. So, let’s say a client mortgage, for instance, on this case blockchain provides a number of advantages. One is the transparency that comes together with that, so now if you wish to purchase or promote that mortgage, you will have a collection of blocks that has all the details about that mortgage. It has the underwriting standards, the documentation, provision of client disclosures, funds, amortization, all of that so as a substitute of getting to audit the financial institution that underwrote the mortgage, you’re in a position to provision entry to that information.

After which the second piece which I feel is absolutely thrilling is what occurs whenever you use the identical system of document for the fee and for the asset. So at the moment, if I wish to purchase a mortgage from you, now we have to ship cash into escrow after which in the end that escrow agent will look to a different system of document to see if the asset/the mortgage has moved from me to you after which in the end will launch funds to you after that’s occurred.

If you carry them on to the identical system of document, you’ll be able to have real-time switch that’s contingent on the opposite so the cash doesn’t transfer until the asset strikes and the 2 occur on the identical time with zero settlement threat between that. So, as we hit that phase base, we expect there’s quite a lot of alternative to decrease funding prices and create efficiencies that may permit these belongings to maneuver sooner and permit extra clients to entry them as a result of they’re cheaper.

Peter: Fascinating, attention-grabbing. So then, you touched on programmability and I feel that is one thing that few individuals have grasped but in conventional finance and I feel it’s simply, you already know, we is likely to be speaking of a number of years down the street earlier than this actually turns into mainstream, however I simply are inclined to assume that is going to be such an enormous recreation changer with programmable cash which……cash has been non-programmable for, effectively, because it started so inform us a bit bit in regards to the programmability of USDF and the way that may be leveraged.

Rob: Completely. And I feel this is among the actual powers behind blockchain is it permits that real-time collaboration between establishments and permits for the automation of duties which might be at the moment typically take quite a lot of time and might implement human error at every step. So. for instance, let’s take a look at that very same mortgage closing course of, proper, and as a substitute of sending cash to escrow after which having an escrow agent ship particular person funds to all the events related to that transaction, whether or not it’s the realtor, the title agent, that’s an entire different problem, however all the particular person items of that transaction at the moment, you must ship one lump sum of cash to the escrow agent who will then ship the person funds, name the banks, verify wires.

With programmability on the very first stage, which I feel we will obtain sooner, you’ll be able to create an automatic waterfall of funds the place below the correct circumstances the right amount is delivered to the proper get together on the appropriate time. It takes quite a lot of that friction out of the transaction and as we get farther alongside and begin digitizing a few of these different belongings, it’s also possible to tie the situations of the belongings to the funds themselves. So, let’s say it’s somebody who buys a participation in a mortgage, you’ll be able to have these funds mechanically redirect to the homeowners in the correct quantities and so actually assume again now to quite a lot of effectivity.

Peter: It’s superb. I really feel just like the use instances are infinite whenever you begin type of carrying that ahead, however I wish to contact on funds as a result of funds, proper now, now we have every thing settles by these Fed Grasp accounts. Should you obtained two banks which might be a part of your consortium they usually’re doing a transaction between the 2, you probably did point out that it’s nonetheless carried out by Fedwire, settled by Fedwire, are we going to get to a spot the place we utterly bypass the Fed system, whether or not it’s Fedwire or FedACH?

Rob: I don’t assume so and in the end, I feel we view this as complementary to quite a lot of their techniques. I do know we obtained information this week about when FedNow will probably be out there, it’s not now, nevertheless it’s coming. I feel, in the end, the banks nonetheless have to settle through a few of these wholesale techniques on the finish of the day, however what we expect this will do is be that messaging layer that permits for transactions within the real-world to occur on the identical time, occur on chain and make sure at the moment to leverage a few of these efficiencies, to leverage a few of that programmability and in the end, by cash will nonetheless have to settle by the Fed on the finish of the day or in real-time, relying on the use instances.

Peter: Proper, proper. , I had Mike Cagney on the present, that was in all probability over a yr in the past now, speaking about a few of the issues that you just’re mentioning right here and I simply wish to clarify, like Mike Cagney, clearly the CEO & Co-Founding father of Determine, they created the Provenance blockchain which I do know is separate from Determine and USDF, possibly you’ll be able to clarify how these three entities are associated. You’ve obtained the USDF Consortium, the Provenance blockchain and also you’ve obtained a personal firm, Determine, which sort of, you already know, created quite a lot of the know-how.

Rob: So, I’ll begin with USDF, we’re a gaggle of banks, we’re owned by our member banks, a gaggle of banks which have come collectively to construct what they assume is these future trendy blockchain-based funds rails they usually have achieved it on Provenance. So, Provenance, to your level, is the general public permissionless chain that Determine has constructed and we function as a walled backyard the place solely insured depository establishments can transact on that chain.

And so, what we’re doing is bringing financial institution stage funds on to that chain so Provenance is separate, after which Determine clearly has performed a key function and actually ahead trying when it comes to how can we carry conventional monetary providers belongings on-chain. So, they’ve constructed quite a lot of that infrastructure and the know-how that the banks will leverage as they do this.

Peter: Proper, okay. In your earlier function, clearly, you had been speaking with regulators on a regular basis and, you already know, it feels just like the regulatory piece goes to be key for the success of USDF. So, whenever you take a look at the important thing regulators just like the OCC, the FDIC and the Fed, the place are you at at the moment, what are your conversations like with these entities?

Rob: Yeah. So, what I’ll say is that I feel the general public coverage crucial is sufficient of a motive why I made this transfer and as we glance in direction of that way forward for tokenized cash, I feel it’s throughout the coverage of panorama throughout Washington. Coverage makers are taking a look at numerous dangers related to the crypto ecosystem at the moment and persistently what we’re beginning to hear is the way in which to handle these dangers is thru the financial institution regulatory framework. It seems we even have a regulatory framework for digital cash at the moment and it’s by banks, like financial institution deposits are regulated as digital cash.

And so, in some ways we’re answering the decision that Treasury made within the President’s Working Group Report, Treasury and the opposite banking companies, the place they regarded on the future regulatory framework for Stablecoins. Now, once more, we’re not a Stablecoin, we’re a tokenized deposit, however as they checked out how do you carry cash on-chain, what’s the acceptable regulatory construction and the reply is absolutely persistently banking regulation. So, what we expect we provide is a technique to carry quite a lot of these advantages of blockchain-based funds, however do it whereas sustaining the identical protections that the banking system provides and do it whereas sustaining a few of the identical advantages that the banking system brings to our economic system within the function it creates creating credit score.

So, from an enormous image perspective we expect there’s quite a lot of alternative right here to assist carry this innovation from the trusted regulated events that the shoppers are used to participating with. Now, we’ll proceed to work with the banking companies, we’re speaking to every of the companies and as you already know every of the banking companies now require some type of approval or discover earlier than any financial institution can interact in something deemed to be a crypto exercise So, we’re working actually intently with the companies at the moment to assist clarify our mannequin, assist them perceive that that is actually a brand new ledger, we’re constructing, conventional financial institution funds, not essentially constructing bridges to a few of the crypto ecosystem that exists outdoors of banking at the moment.

Peter: You’re not a crypto exercise, proper, it’s blockchain-based, it’s not crypto.

Rob: I feel something that touches blockchain at the moment in all probability falls below the OCC interpretive letter 1179 the place a few of the different steering from the FDIC and the Fed we’ve seen extra not too long ago. I feel something that engages with blockchain in all probability falls below these, however not each a kind of actions presents the identical dangers. What we’re attempting to show is absolutely it is a know-how query and we expect that there’s a new ledger that may be extra environment friendly for what banks have all the time achieved and the way to ensure now we have the suitable controls round that to ensure regulators are snug earlier than we transfer ahead.

Peter: Proper, proper. Talking of creating regulators snug, I really feel like, the Treasury put a request for remark out on digital belongings, you set an in depth response collectively, are you able to simply summarize the ten pages that you just wrote within the request for remark to Treasury.

Rob: Completely. And I feel the response is absolutely what we’ve talked about already that when you assume there’s worth to bringing cash on-, we expect that it’s essential to 1) keep the protections that exist inside the financial institution regulatory framework and, 2) keep the worth the banks carry within the credit score creation function that they play. So, as we take a look at that panorama at the moment and see whether or not it’s in direction of Stablecoins that more and more now we have a regulatory, or a legislative dialogue round how we should always regulate Stablecoins and may they be absolutely reserved.

We additionally see discussions round whether or not the Federal Reserve ought to problem a CBDC to carry cash on-chain. The case that we make is that we should always leverage the two-tier banking system that exists at the moment, that we should always keep these protections that financial institution regulation was designed to implement and we should always create a transparent path for banks to serve the identical function on-chain that they do in others in order that we will preserve shoppers protected whereas we carry blockchain innovation into the true phrase.

Peter: Proper, proper. So, I wish to contact on the CBDCs now as a result of that, in your feedback and listening to others speak about this, that USDF actually negates the necessity for CBDCs, is absolutely what I feel you’re saying, proper? Perhaps you could possibly speak about how would USDF work with a CBDC or are you feeling like that is, actually banks needs to be actually in management, like in relation to their…..they’ve the connection which is direct to client, we don’t need the Fed having 300 million relationships clearly with shoppers, however inform us a bit bit about how USDF views CBDCs.

Rob: In some ways, I feel {that a} CBDC accurately designed might be complementary to what we’re constructing. So, the dialog round CBDC is all the time a extremely exhausting one as a result of very like fintech, it means one thing totally different to everybody that claims it and the place a lot of the coverage dialogue has targeted, thus far, is on the idea of retail CBDCs and that is whether or not a CBDC is delivered immediately from the Fed to shoppers or achieved by the banking system in an intermediated mannequin. All of these retail fashions in the end are a Fed legal responsibility that customers can maintain direct so I feel the priority that you just’ve heard from the business about that retail mannequin is that each greenback that’s held in CBDC will in the end sit on the Fed’s stability sheet and never on particular person financial institution’s stability sheet the place it’s out there to be again into the communities that they serve.

Now, what hasn’t acquired the identical quantity of airtime is the thought of a wholesale CBDC, one which acts in the identical function, that you just see a FedNowor an RTP does the place shoppers by no means see it, shoppers nonetheless maintain their cash in financial institution accounts. So, the place we will leverage trendy backend infrastructure to create those self same type of real-time funds and leverage these efficiencies of blockchain and so what I’m hopeful we’ll see extra of as this coverage dialogue develops is a deal with the trade-offs between a retail and a wholesale CBDC.

So, our view is {that a} retail CBDC actually has main prices, significantly how can we keep the credit score entry of the communities that we’re attempting to assist serve if we’re taking deposits out of banks who’re the entities at the moment that create that credit score. We expect a wholesale CBDC is likely to be a lot better positioned to assist obtain the true objectives and empower banks to supply the newest services to their clients whereas sustaining the identical two-tier system that exists at the moment.

Peter: Okay. So, let’s speak a bit bit in regards to the Consortium itself, you’ve obtained many banks on there. Perhaps you could possibly simply inform us a few of the banks which might be truly a part of it and who else is on the consortium.

Rob: So, as I discussed, the Consortium is the group of banks which have come collectively. We’re owned by our member banks, now we have 9 banks within the Consortium at the moment, the banks are neighborhood and regional banks and I feel they’re the banks that 1) have been ahead leaning when it comes to their very own enterprise mannequin, how do they place themselves to ensure they’re able to reap the benefits of the efficiencies that this will carry. However 2) have additionally acknowledged the significance of the business standing up this sort of a performance and have opened the door for different banks who wish to be part of and wish to have that seat on the desk as we develop a blockchain-based trendy fee rail.

Peter: Okay. And you then’ve additionally obtained, I imagine, Determine is a member, proper and JAM FINTOP which is absolutely an investor group, what’s the pondering there?

Rob: Yeah. And people are two different teams once more, we talked a bit bit about Determine, they constructed quite a lot of the know-how, JAM is among the networks they’ve introduced collectively numerous the banks that had been pondering by, actually they had been ahead leaning pondering by how banks can interact thoughtfully on this area. And so, they’ve helped carry this group collectively, construct a few of the widespread infrastructure, however essential to notice that once we speak about tokenized deposits that actually is proscribed to insured depository establishments so solely the banks will be capable of interact within the enterprise of minting, transferring and burning USDF.

Peter: Proper, proper. So then, the place are you at in that course of, I imply, like is there a pilot taking place at the moment, when are we going to see banks truly minting USDF?

Rob: Yeah. So, now we have banks who’ve constructed the infrastructure, have constructed the check protocols and are actually able to go dwell. As I discussed, we’re nonetheless working with regulators to get that formal approval, that’s one thing that’s a little bit of a brand new dynamic in banking, having to ask permission moderately than ensuring regulators are snug. So, we’re engaged on getting that formal approval after which prepared to start shifting transactions.

Peter: Proper. And I think about, you clearly wish to broaden this past 9 banks and I additionally think about you talked to a lot of totally different banks earlier than you took this job so what are the considerations that banks have which have mentioned no to hitch the Consortium or no less than mentioned, I’m not prepared but.

Rob: Yeah, and it truly is that second piece. So, I did speak to numerous banks as I made my transition over earlier than and since, and I feel there’s actually quite a lot of curiosity, quite a lot of broad recognition of the significance for banks of getting these trendy blockchain-based funds choices and I feel enthusiasm about guaranteeing banks keep the identical function they do within the economic system. The banks that aren’t signing on at the moment are those who I feel, to your level, aren’t fairly prepared but and one of many issues I typically hear is I don’t essentially have the employees experience or my board will not be fairly in control on precisely what this implies and the way it matches into the large image.

And we’re truly beginning to see a few of these banks present actual curiosity within the consortium in addition to they work in direction of truly implementing USDF, however recognizing that we’re additionally bringing, as a type of bank-owned group, a little bit of that commerce affiliation mannequin. So, even for the banks that aren’t able to go dwell tomorrow, that we expect there’s quite a lot of worth in participating within the working teams, serving to get your employees, whether or not it’s the authorized crew, whether or not it’s the compliance crew up that actually steep studying curve in addition to serving to your board perceive that you’ve a holistic technique in your financial institution’s function in a blockchain economic system.

Peter: Proper, proper. So, I think about whenever you get approval, whenever you truly launch as a result of, I imply, proper now, every thing continues to be, you already know, considerably theoretical as a result of there isn’t a authorised product, proper. I think about, that’s going to, in your projections, that’s the place the momentum goes to return, is that proper?

Rob: Yeah. We’ve had quite a lot of curiosity, I feel we’ll see extra banks participating right here within the close to future and anticipate, particularly as we see these confirmed out in actual world transactions and from a aggressive standpoint, we expect there will probably be much more curiosity as effectively.

Peter: Okay. So then, let’s change to the lawmakers, you already know, you mentioned you’ve been round Washington a very long time, you’ve sort of obtained a reasonably good concept about how Washington works. There’s been speak about, like Stablecoins as being the one factor that’s going to get regulated first as a result of it looks like it’s a lighter carry and clearly now we have midterms developing in two months so, you already know, won’t occur within the brief time period, however what do you anticipate the following transfer from regulators to be in relation to digital belongings?

Rob: Sure. There’s actually two issues we’re watching. On the regulators, we’re watching the reviews which might be due out of the chief order so these reviews are due on September fifth, numerous them are. I feel we’ll get actually good readability when it comes to the place the companies are on all of those points once we see these reviews. I’m undecided when this can air, and this can be dated by then, however within the subsequent few weeks, we anticipate to get extra readability on that. I do know quite a lot of actually exhausting work has gone in over the summer time to craft these reviews and so these I feel will probably be a extremely considerate illustration of the place the banking companies and different companies round Washington are on these points.

The second piece we’re watching that you just talked about is the Stablecoin laws popping out of the Home Monetary Providers Committee in addition to different laws that’s been developed by actually considerate members of Congress. What I’ll say there’s it’s actually one thing we’re watching and fascinating in and once more, USDF shouldn’t be a Stablecoin and I feel, you already know, what we’re seeing is a extremely considerate bipartisan effort to grasp the advantages to assist put within the acceptable regulatory environments that now we have constant protections.

What we’re attempting to ensure as we take a look at that is that banks are in a position to play that very same function on a blockchain-based system that they do in each different economic system. So, once more, guaranteeing that banks have the flexibility to take deposits, to make loans and facilitate funds, I feel it’s actually essential that they’re in a position to serve that very same function as we transfer into this type of trendy infrastructure.

Peter: I additionally heard, I heard lots of people say that actually banks needs to be those that problem Stablecoins, proper. I imply, that’s turn out to be a part of the dialog, you already know, in a really possible way, it appears.

Rob: Yeah, completely. That hasn’t been our focus, proper, our members simply wish to be one of many choices on the market, however I feel there’s a broad recognition and we noticed this within the President’s Working Group Report that these are precisely the dangers of taking what’s successfully a deposit facilitating funds, are precisely the dangers of the banks’ regulatory construction is designed to manage, proper? There’s a motive that the complicated set of laws that banks are topic to, there’s a motive these are in place, they’ve been applied actually thoughtfully over an extended time frame and so if you wish to keep those self same protections, the banking regulatory construction is a extremely good place to begin.

Peter: Proper, proper, okay. So, let’s shut with a future-looking query and I’d like to sort of get your sense of what your imaginative and prescient is for USDF and for what the banking system will appear like let’s simply say in ten years time. I do know it’s not simple to gaze into the crystal ball that far sooner or later, however you have to have considered this deeply, I’m guessing.

Rob: Yeah, completely. And so, there are some things as I look ahead that I’m actually hopeful will materialize, whether or not it’s the following two, 4, ten years. , the primary is that I feel we’ll see blockchain getting used as widespread infrastructure for an increasing number of actual world belongings. So, at the moment what we see is that quite a lot of the crypto ecosystem has demonstrated the worth of this know-how, however now we have but to see it actually work together with the true world in significant methods and so what I’m hopeful is that we are going to see extra tokenized belongings, whether or not it’s in monetary providers or different industries and leveraging the ability of blockchain and I feel which means a number of issues.

The primary I feel, that widespread infrastructure will permit smaller establishments to punch above their weight so my hope is that we see much less consolidation within the banking business as neighborhood banks are in a position to leverage this shared infrastructure and actually be capable of do what neighborhood banks do effectively which is know and have interaction of their communities. The second piece that I feel is absolutely essential and one of many issues that will get me enthusiastic about that is that the efficiencies that may carry will decrease the barrier to entry for monetary providers, decrease the price of serving these communities and assist create extra inclusive entry to monetary providers to assist be certain that our nation’s banking system works for the whole nation.

Peter: Okay. That’s an awesome imaginative and prescient and we’ll all be following alongside to see how lengthy, whether or not it turns into actuality we actually hope that there’s quite a lot of motion right here within the brief and medium time period. So, Rob, thanks a lot for approaching the present, it’s all the time nice to speak with you, I actually respect it.

Rob: Thanks, Peter, all the time a great time, actually respect you having me.

Peter: , you typically hear the crypto lovers speak about bypassing the banks, shifting past the banks as even the actually in style neighborhood referred to as “bankless” that we are literally concerned with right here with Fintech Nexus, however my place is that we aren’t going to go “bankless” any time quickly as a tradition, as a rustic, you already know, actually internationally. I imply, the banks on this nation, particularly, they’re the core of our monetary system, this isn’t crypto, it’s blockchain-based, nevertheless it will get thrown into that bucket as he mentioned.

However banks are right here to remain and banks needs to be collaborating in bringing the fruits of the blockchain motion to bear on shoppers, for shoppers and small enterprise and that’s precisely what USDF is designed to assist facilitate. I see it as, you already know, banks are going to alter dramatically over the following decade, we aren’t going “bankless,” we’re, effectively by no means say by no means, however we’re actually not going to do it within the subsequent a number of many years. We’re going to have a extra environment friendly monetary system nonetheless centered round banks, nevertheless it’s a system that’s going to be way more environment friendly, less expensive and a lot better than what we’ve had previously.

Anyway on that observe, I’ll log out. I very a lot respect you listening and I’ll catch you subsequent time. Bye.

(music)

{kind=link}