{kind=link}

A brand new paper from Yale professor Kelly Shue argues that customers mistakenly wait to take out mortgages and different long-term loans when the Fed is predicted to chop charges.

Their confusion appears to be associated to conflating short-term and long-term charges, which don’t essentially transfer in tandem.

In reality, short-term price strikes are sometimes already baked in to long-term charges, which means there’s no want to attend till the lower is official for a fair decrease rate of interest.

The financial savings of short-term price cuts ought to already be mirrored within the rate of interest of a long-term mortgage equivalent to a 30-year mounted mortgage.

Regardless of this, residence patrons and even skilled forecasters are likely to get this fallacious in accordance with the analysis.

Brief-Time period Charges vs. Lengthy-Time period Charges

Customers have lengthy misunderstood the connection between the Fed and mortgage charges.

Many incorrectly consider that the Fed straight controls mortgage charges. So when the Fed proclaims a price lower, potential residence patrons anticipate mortgage charges to come back down as nicely.

For instance, the Fed is extensively anticipated to decrease its fed funds price by 25 (or perhaps 50 foundation factors) at its September 18th assembly.

When this takes place, there can be a slew of articles written about how “mortgage charges fall” and the like.

Some might even assume that the 30-year mounted fell by the identical quantity, whether or not it’s 0.25% or .50%.

So if the 30-year mounted was 6.50% the day earlier than the assembly, a hypothetical residence purchaser may assume the going price is 6.25% and even 6% the following day.

In all probability, they’ll most likely be dissatisfied if and after they communicate to their mortgage officer or mortgage dealer.

Likelihood is mortgage charges gained’t budge a lot in any respect. And maybe worse, they may truly rise after the Fed proclaims a price lower!

This all has to do with short-term and long-term charges, with the fed funds price a short-term price and the 30-year mounted a long-term price.

Whereas they’ll affect each other, there isn’t a direct correlation. This is the reason you don’t hear mortgage price specialists telling you to make use of the fed funds price to trace mortgage charges.

As a substitute, the 10-year bond yield is an effective technique to monitor mortgage charges, since traditionally they’ve a really robust correlation.

Merely put, they’re each long-term charges and performance pretty equally as a result of many residence loans are paid off in a decade or so regardless of being supplied a full 30 years .

Ought to You Anticipate the Fed to Lower Charges Earlier than Refinancing (or Shopping for a House)?

That brings us to client conduct surrounding price cuts and hikes. Earlier than we speak about price cuts, that are lastly on the desk, let’s speak about price hikes.

When the Fed is predicted to hike charges, folks are likely to rush out and lock their mortgage earlier than charges go up much more.

The researchers, which embrace Professor Shue, Richard Townsend, and Chen Wang, argue that this too is “a mistake.”

They word that understanding “that the Fed plans to step by step improve brief charges doesn’t imply that lengthy charges will step by step improve in tandem.”

Conversely, they are saying “the lengthy price jumps instantly in response to such an announcement,” which means there isn’t a rush to lock your price earlier than the Fed acts.

Now once we flip the script and think about a price lower, the identical logic applies. In case you’re ready to purchase a house or refinance your mortgage on account of an impending price lower, it could be a mistake.

The Fed price cuts are principally telegraphed upfront and recognized to market individuals. So there gained’t be a giant shock on the day of the announcement that results in a big enchancment.

At the least not with regard to the speed lower announcement itself. This is the reason mortgage charges typically defy logic on the day Fed bulletins happen.

Typically the Fed raises its price and mortgage charges fall. And typically the alternative occurs.

And once more, that is as a result of disparity between short-term and long-term charges.

What About Lengthy-Time period Financial Coverage?

Whereas I agree with the researchers on the purpose of short-term price cuts already being baked in to longer-term charges like 30-year mortgages, there’s one different factor to contemplate.

The anticipated long-term financial coverage of the Fed. If they’re simply starting to chop short-term charges, there’s a probability long-term charges proceed to enhance over time.

I do know, the researchers already debunked this with their speak about step by step rising charges, saying folks “fail to acknowledge that the present lengthy price already displays future anticipated modifications in brief charges.”

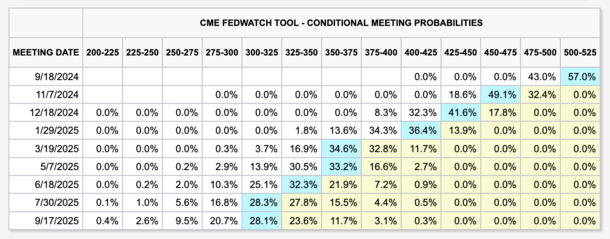

And in the intervening time, the consensus is for the Fed to chop charges 200 foundation factors or extra over the following yr, per CME.

By the September seventeenth, 2025 assembly, the fed funds price might be in a variety of three% to three.25%, down from 5.25% to five.50% at present.

Positive, you can argue that this too is considerably baked in to long-term charges in the intervening time, however there’s nonetheless a level of uncertainty.

If and when the Fed does truly start reducing charges, as an alternative of merely hinting at it, we may see longer-term charges trickle down additional.

After all, that can rely on financial information and issues like inflation and unemployment, which can solely reveal themselves over time.

However when you take a look at the speed tightening cycle, which concerned 11 Fed price hikes between early 2022 and mid-2023, you’d see that mortgage charges saved getting worse and worse.

Granted that too was pushed by the underlying financial information, particularly out-of-control inflation.

Nonetheless, the 30-year mounted surged from roughly 3% in early 2022 to round 8% throughout that span of time. So those that did exit and lock their price ASAP had been rewarded.

Even somebody who selected to take out a 30-year mounted in March 2022 was capable of snag a ~3% price versus a price of practically 6% by as early as June of that very same yr.

In different phrases, what the Fed has already indicated could be baked in to charges right this moment, however what we’ve but to seek out out may push charges even decrease as time goes on.

There’s no assure mortgage charges will proceed to lower from right here, but it surely’s decently seemingly if financial information continues to come back in chilly.

Earlier than creating this web site, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 18 years in the past to assist potential (and present) residence patrons higher navigate the house mortgage course of. Observe me on Twitter for decent takes.