The rise of fintech and the transfer of economic companies to a extra digital aircraft profit the plenty.

The rise of “customer-centric” fintech has added competitors to the monetary market, creating improved accessibility and inclusion whereas providing shoppers an expanse of additional companies.

Nonetheless, this has come at a worth. Tales of knowledge breaches and hacks have gotten extra commonplace. In 2021 there have been a reported 1,862 knowledge breaches within the U.S.

As well as, the nebulous nature of how knowledge is saved, used, and bought to 3rd events, has prompted concern for shoppers.

Rising strain to create digital identities, whether or not to streamline monetary processes or enhance competitors for the consumer’s profit, has made securing digital privateness extra crucial.

The concept of digital id has been fraught with controversy, many seeing it as an “finish to freedom.” Nonetheless, the idea of Self-Sovereign Id (SSI) turns these issues considerably on their head.

SSI – A rising market

SSI is a type of digital id which permits shoppers to retain full management of their knowledge.

“The entire function is to provide shoppers possession and management over their knowledge and privateness. Permitting them to have the ability to management what they share and with who,” mentioned Landon Glenn, CEO, and founding father of ASA.

In Europe, exams with digital id are underway; many member states have already got government-issued digital id keys. Nonetheless, 72% are unsure about how their knowledge is used.

The US authorities has additionally began exploring the thought of digital id, though they’re dealing with comparable client issues.

SSI acts like a personal ledger or digital pockets primarily based on the blockchain. Customers have direct management of the data they share, which is just accessible with digital keys. Utilizing certificates inside the pockets can even give the consumer credentials and entry to monetary merchandise with out sharing particular knowledge.

Curiosity within the expertise is rising. Based on Juniper Analysis, SSI income is anticipated to succeed in $53.2 billion by 2026, rising at a charge of 15.16% per 12 months between 2022 and 2026.

“One of many ideas that ring the truest to me is which you could show issues about your self with out giving up non-public info,” continued Glenn.

“For instance, you could possibly show that you’ve got a credit score rating over a sure quantity with out sharing your social safety quantity, rating, or another figuring out info you don’t wish to share.”

He defined that as a blockchain-based expertise, SSI had, till now, encountered lowered adoption. “If you should situation tens of millions of credentials, generally it might probably take every week or extra. I believe the following steps for this as an trade is to get it into the arms of the customers, get them utilizing the vault, get them connecting and managing their identities.”

Benefitting monetary inclusion and empowerment

This various approach of sharing knowledge advantages monetary inclusion and empowerment.

Primarily, it may improve accessibility to a extra aggressive market, permitting entry to fintechs with lowered belief issues. Though 90% of People now use not less than one kind of fintech, Ondot discovered that 74% thought of fintechs extra prone to promote on their knowledge. Pew Analysis discovered 81% of the general public really feel the potential dangers they face due to knowledge assortment by corporations outweigh the advantages, with many feeling a scarcity of management over their knowledge.

“I’ve gone into sure apps a number of occasions, after which they begin asking me for extra info; I simply stopped giving it,” mentioned Lisa Gold Schier, CSO of ASA. “If you consider it that approach, after we discuss monetary empowerment, that’s protecting me from utilizing some expertise I would need.”

“Now, you not need to share that info as a result of we’ll anonymize that. So that you at the moment are in a position to get the expertise you need. With out feeling like you need to give the factor away.”

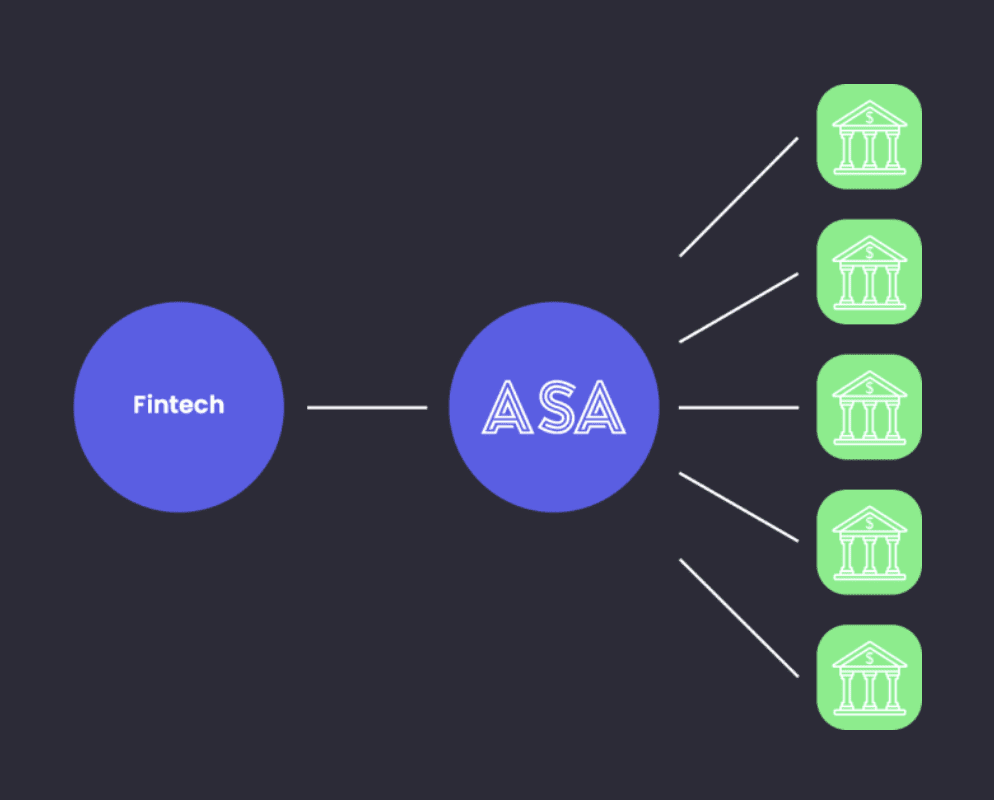

ASA employs the idea of SSI in collaboration with monetary establishments and fintechs. Very like a digital pockets, customers can retailer their credentials inside the ASA account, which is able to then be tokenized. That is connected to their trusted major financial institution after which connects with fintechs which have added the ASA open API.

“It’s permitting the financial institution to not need to do one-to-one integrations with every fintech on the market,” she continued. “It brings that belief and safety.”

“As an end-user client, I now really feel extra comfy utilizing the fintech that’s on the market; I don’t need to share any identifiable info. And it brings scale to all as a result of now all of us have that entry. So it permits each side to scale once more, for the advantage of the top client.”

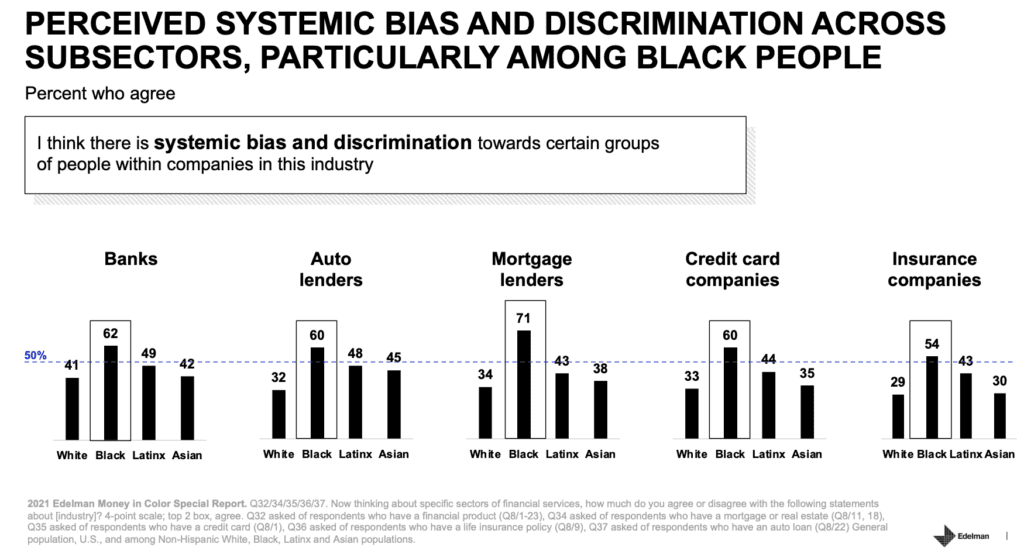

Moreover, SSI may assist with monetary inclusion. Quite a few research have discovered {that a} systematic bias exists inside monetary companies. Based on Fortune, 68% of black respondents incomes over $100,000 reported a damaging expertise, in comparison with 36% of white respondents. The anonymity proposed by SSI may straight facilitate entry to monetary companies primarily based on impartial knowledge.

“All that may have been used previously, whether or not or not it was meant for use to decide, that gained’t be seen,” Gold Schier continued.

The corporate solves the expertise situation presently dealing with full SSI fashions by combining the elements of SSI inside its third-party framework as an alternative of conducting all verifications by blockchain expertise.

“Because the expertise progresses, we see it as us ending out the loop, adopting a full SSI mannequin. We’re ready for the expertise to hit the purpose it must hit the dimensions that we’re going to require to service our prospects,” mentioned Glenn.

Creating influence by collaborative banking

“I believe one of many largest impacts is the accessibility of expertise,” mentioned Glenn. “Once you surprise why hasn’t expertise been accessible earlier than? Why can’t I get apps by my financial institution? Individuals don’t perceive the regulatory burden that banks have. They don’t perceive the compliance hurdles that cripple them from with the ability to innovate, the time it takes for the approvals.”

“The trade is at a fork. Both we’ve got to let fintechs attempt to develop into banks, which suggests they’re now promoting bank cards and loans and accounts. However it extends that regulatory burden to them. And now they’ve to fret about lending, KYC, AML, and on and on. They usually need to have that safety as a result of they’ll entry the shoppers’ funds.”

“The opposite path is one thing we discuss with as collaborative banking or embedded fintech, and that path permits the fintech to go to market with out seeing that regulated knowledge. And so what meaning is it opens up the world to the place you’ll be able to have a limiteless variety of options that go to market in a short time. They usually don’t put the client in danger in any approach.”

He defined that by sustaining this flexibility, the market may benefit from fintechs in very area of interest markets, creating merchandise for particular teams.

“Monetary empowerment is getting this expertise within the arms of the individuals who crave and want it, they usually don’t have entry to it immediately. They don’t have that form of assist.”

Associated:

{kind=link}