{kind=link}

The data offered on this web site doesn’t, and isn’t meant to, act as authorized, monetary or credit score recommendation. See Lexington Regulation’s editorial disclosure for extra info.

The statute of limitations on debt sometimes ranges 3 – 6 years, relying on the debt sort and the state you reside in.

Is there a statute of limitations on debt? It is dependent upon the kind of debt and which state’s regulation governs it. Discover out extra in regards to the statute of limitations on suing to gather a debt by state beneath.

Desk of contents:

What’s a statute of limitations on debt?

A statute of limitations on debt limits how lengthy collectors or assortment companies can solely take authorized motion towards you to gather a debt. The size of that interval is dependent upon the statute of limitations within the state the place the debt originated.

Statutes of limitations are legal guidelines that govern the deadlines for sure authorized actions. However don’t be mistaken—you aren’t off the hook for a debt simply because the statute of limitations has handed. The debt may nonetheless present up in your credit score report, and for those who don’t pay it, you might face bother getting future credit score, particularly a mortgage.

The statute of limitations does forestall you from being efficiently sued for time-barred money owed. Which means the creditor gained’t have the ability to get a judgment towards you that enables them to garnish wages or levy your accounts.

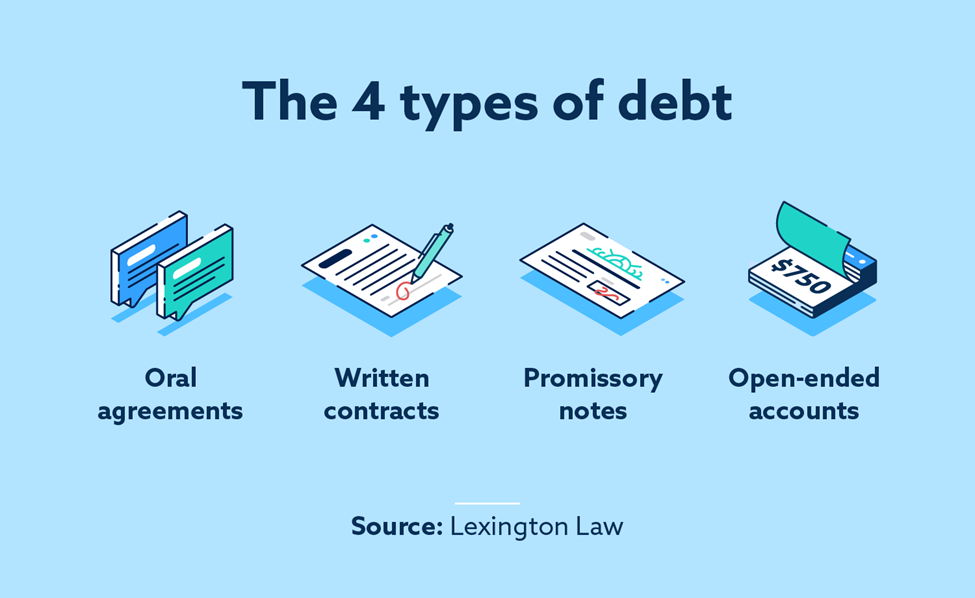

The 4 forms of debt

The kind of debt you’re coping with determines which statute of limitations is likely to be related. Learn on to be taught in regards to the 4 various kinds of debt.

Oral agreements

Oral agreements happen while you borrow cash from somebody and conform to pay it again in line with particular phrases, however the settlement isn’t in writing.

That is the proverbial handshake settlement, and it’s not extraordinarily widespread between conventional lending organizations and debtors right now. That is primarily as a result of they’re troublesome to show. Oral contracts usually tend to exist between members of the family or associates.

Written contracts

Written contracts document the small print of a lending settlement, together with the borrow quantity and date, the aim of the mortgage, curiosity quantity, when and easy methods to make funds and different phrases. Each events concerned within the contract—the borrower and the lender—signal the doc to validate it.

Written contracts are simpler to show than oral contracts. Automobile loans are written contracts. Medical debt or funds for providers you agreed to in writing are additionally written contracts.

Promissory notes

Promissory notes are just like written contracts however with much less element. As well as, they solely must be signed by the borrower to be enforceable. You usually signal a promissory be aware while you take out a mortgage or scholar mortgage.

Open-ended accounts

Usually, these are revolving accounts resembling bank cards or traces of credit score. Open-ended accounts stay open for an undetermined size of time so long as you make common and agreed-upon funds. You can even carry a steadiness on these accounts so long as you make common minimal funds.

Statutes of limitations by state

This information to statutes of limitations on debt assortment by state is for informational functions solely. Debt legal guidelines change now and again, and it is best to all the time test with a authorized skilled or your state Lawyer Normal’s workplace for present info.

| State | Oral Agreements | Written Contracts | Promissory Notes | Open-Ended Accounts |

| Alabama | 6 years | 6 years | 6 years | 3 years |

| Alaska | 3 years | 3 years | 3 years | 3 years |

| Arizona | 3 years | 6 years | 6 years | 6 years |

| Arkansas | 3 years | 5 years | 5 years | 5 years |

| California | 2 years | 4 years | 4 years | 4 years |

| Colorado | 6 years | 6 years | 6 years | 6 years |

| Connecticut | 3 years | 6 years | 6 years | 6 years |

| Delaware | 3 years | 3 years | 3 years | 3 years |

| Florida | 4 years | 5 years | 5 years | 5 years |

| Georgia | 4 years | 6 years | 6 years | 6 years |

| Hawaii | 6 years | 6 years | 6 years | 6 years |

| Idaho | 4 years | 5 years | 5 years | 4 years |

| Illinois | 5 years | 10 years | 10 years | 5 years |

| Indiana | 6 years | 6 years | 10 years | 6 years |

| Iowa | 5 years | 10 years | 10 years | 5 years |

| Kansas | 3 years | 5 years | 5 years | 5 years |

| Kentucky | 5 years | 10 years | 15 years | 10 years |

| Louisiana | 10 years | 10 years | 10 years | 3 years |

| Maine | 6 years | 6 years | 20 years | 6 years |

| Maryland | 3 years | 3 years | 6 years | 3 years |

| Massachusetts | 6 years | 6 years | 6 years | 6 years |

| Michigan | 6 years | 6 years | 6 years | 6 years |

| Minnesota | 6 years | 6 years | 6 years | 6 years |

| Mississippi | 3 years | 3 years | 3 years | 3 years |

| Missouri | 5 years | 10 years | 10 years | 5 years |

| Montana | 5 years | 8 years | 5 years | 5 years |

| Nebraska | 4 years | 5 years | 5 years | 4 years |

| Nevada | 4 years | 6 years | 3 years | 4 years |

| New Hampshire | 3 years | 3 years | 6 years | 3 years |

| New Jersey | 6 years | 6 years | 6 years | 6 years |

| New Mexico | 4 years | 6 years | 6 years | 4 years |

| New York | 6 years | 6 years | 6 years | 6 years |

| North Carolina | 3 years | 3 years | 3 years | 3 years |

| North Dakota | 6 years | 6 years | 6 years | 6 years |

| Ohio | 6 years | 6 years | 6 years | 6 years |

| Oklahoma | 3 years | 5 years | 6 years | 3 years |

| Oregon | 6 years | 6 years | 6 years | 6 years |

| Pennsylvania | 4 years | 4 years | 4 years | 4 years |

| Rhode Island | 10 years | 10 years | 10 years | 10 years |

| South Carolina | 3 years | 3 years | 3 years | 3 years |

| South Dakota | 6 years | 6 years | 6 years | 6 years |

| Tennessee | 6 years | 6 years | 6 years | 6 years |

| Texas | 4 years | 4 years | 4 years | 4 years |

| Utah | 4 years | 6 years | 6 years | 4 years |

| Vermont | 6 years | 6 years | 6 years | 6 years |

| Virginia | 3 years | 5 years | 6 years | 3 years |

| Washington | 3 years | 6 years | 6 years | 6 years |

| West Virginia | 5 years | 10 years | 6 years | 5 years |

| Wisconsin | 6 years | 6 years | 10 years | 6 years |

| Wyoming | 8 years | 10 years | 10 years | 8 years |

Supply: The Stability

When does the statute of limitations clock begin?

Based on the Federal Commerce Fee, the statute of limitations clock begins while you fail to make an agreed-upon fee. Nonetheless, you possibly can reset the statute of limitations clock in some circumstances by making a fee on the debt or agreeing to make such funds in response to a debt collector contacting you.

Earlier than you make any guarantees or make a fee on previous debt, make sure you perceive your rights below the Honest Debt Assortment Practices Act and the statute of limitations in your debt.

Delinquent debt and your credit score report

Usually, damaging gadgets resembling delinquent accounts or unpaid collections will fall off your credit score report after seven years. That’s seven years from the date that the account first turned delinquent.

As you possibly can see from the desk above, many states’ statutes of limitations are beneath seven years. That implies that your credit score might replicate an account that’s previous the date for authorized assortment strategies. In case you legitimately owe the debt in query, your selections embrace:

- Pay the debt off to have it present up as paid—which will be higher within the eyes of potential collectors;

- Attempt to negotiate with the creditor, doubtlessly for a pay for delete or a settlement that allows you to pay lower than you owe to have the account marked paid in full; or

- Await the merchandise to fall off your credit score report.

FAQ

Under are a couple of widespread questions in regards to the statute of limitations on debt.

What can restart the debt statute of limitations clock?

Making a fee on a debt in some states will restart the statute of limitations clock. As well as, promising to pay a debt additionally revives the previous debt, and a brand new statute of limitations will start.

Why are there statutes of limitations on debt?

Statutes of limitations set a time restrict for when debt collectors and collectors can take authorized motion towards a borrower who defaulted on their debt. After the statute of limitations time restrict has expired, collectors and debt collectors can now not file a lawsuit to gather on the debt. These limitations assist shield debtors from being accountable for previous money owed.

What occurs after 10 years of not paying debt?

Usually, after 10 years of not paying debt, the statute of limitations can have handed. Which means that when you technically nonetheless owe the debt, debt collectors could attempt to acquire it, however they sometimes can not pursue authorized motion towards you.

The statute of limitations varies by state, so you’ll want to reference your state’s particular statute of limitations to find out what authorized motion a creditor can take towards you.

Speak to an expert you probably have questions

If a set company contacts you a few debt after the statute of limitations has handed, they sometimes haven’t any authorized standing to sue to gather the debt. That doesn’t imply they could not attempt to acquire, and for those who’re coping with an aggressive creditor or aren’t certain how the regulation impacts your debt, chances are you’ll wish to contact an expert. Moreover, if a set company is reporting very previous money owed to the credit score bureaus, you may have the ability to dispute the data to enhance your credit score profile. Work with Lexington Regulation Agency to be taught extra about credit score restore and the way to make sure the accuracy of your credit score report.

Be aware: Articles have solely been reviewed by the indicated legal professional, not written by them. The data offered on this web site doesn’t, and isn’t meant to, act as authorized, monetary or credit score recommendation; as an alternative, it’s for basic informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or assets contained throughout the website don’t create an attorney-client or fiduciary relationship between the reader, person, or browser and web site proprietor, authors, reviewers, contributors, contributing companies, or their respective brokers or employers.