{kind=link}

The info given on this web site does not, and is not meant to, work as lawful, economic or credit score guidance. See Lexington Regulation’s content disclosure to find out more.

Structure wide range in America isn’t obtaining any type of less complicated, specifically for the more youthful generations. From climbing grocery store expenses to record-breaking real estate rates, several Americans are really feeling the stress.

According to the U.S. Bureau of Labor Data, the expense of living has actually risen greater than 20 percent over the previous 4 years, and salaries are having a hard time to maintain. For Millennials and Gen Zers specifically, the course to economic flexibility really feels longer and unreachable. What variables are forming the economic trips of Americans today?

We checked 1,000 individuals ages 18 and as much as discover just how various generations see wealth-building possibilities, contrasted to the ones their moms and dads had. We additionally inquired about their economic overview, the influence of adult assistance and whether they think today’s financial plans are operating in their support.

The outcomes exposed some striking facts.

Secret takeaways

- High income earners are 2.5x most likely to have actually obtained $50K+ in economic aid from their moms and dads.

- Gen Z continues to be extremely confident concerning their economic future, in spite of thinking the system is set up and dealing with postponed self-reliance.

- Almost fifty percent of Infant Boomers got to economic self-reliance by age 22, faster than any type of various other generation.

- Gen X has the highest possible earnings of any type of generation and the most awful economic overview.

- Increasing expenses are the #1 challenge to constructing wide range, according to every generation.

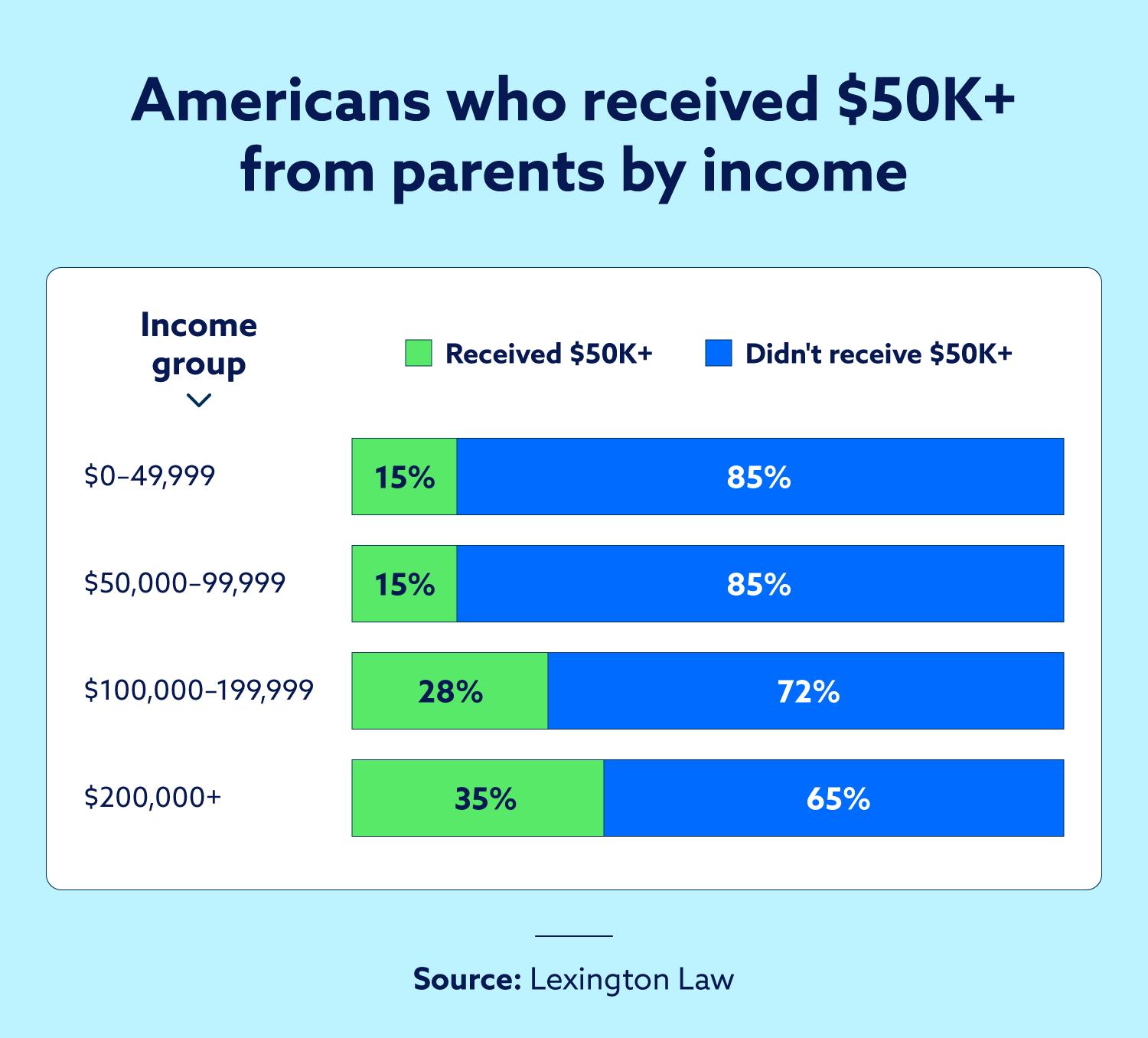

High income earners are 2.5x most likely to have actually obtained large cash from their moms and dads

While several high income earners are usually viewed as “self-made,” our study tests the concept that they arrived on grit alone. It located that individuals making $125,000 or even more each year are 2.5 times most likely to have actually obtained at the very least $50,000 in economic aid from their moms and dads—that’s 36 percent contrasted to simply 14 percent of lower-income income earners.

In Addition, Gen Xers checked reported the highest degree of financial backing from moms and dads, with virtually 1 in 4 getting over $50,000. That sort of assistance, nonetheless, isn’t the standard; majority of Americans (53 percent) got $10,000 or much less, if anything.

From a home deposit to settling pupil fundings, a monetary increase can greater than most likely produce lasting benefits. For those without it, economic security can really feel out of reach.

The fantastic generational wide range misconception / Gen Z remains confident in spite of recognizing a set up system

Also when dealing with financial debt and greater expenses of living, Gen Z remarkably continues to be confident concerning their economic future.

Our study exposed that 87 percent think they’ll be equally as or even more effective than their moms and dads. Component of this self-confidence might originate from very early financial backing, where 49 percent of Gen Z participants reported getting greater than $10,000 from their moms and dads, assisting them take care of very early their adult years.

Positive outlook, nonetheless, isn’t restricted to those with a high total assets. Actually, those making under $25,000 yearly reported an extra favorable economic overview than those making $125,000 or even more (31 percent contrasted to 49 percent that really feel cynical).

Furthermore, 72 percent of those participants additionally think the system is set up for older generations. This reveals cash and state of mind don’t constantly work together, specifically for more recent generations redefining success.

Americans concur: Infant Boomers had the most effective wealth-building possibilities

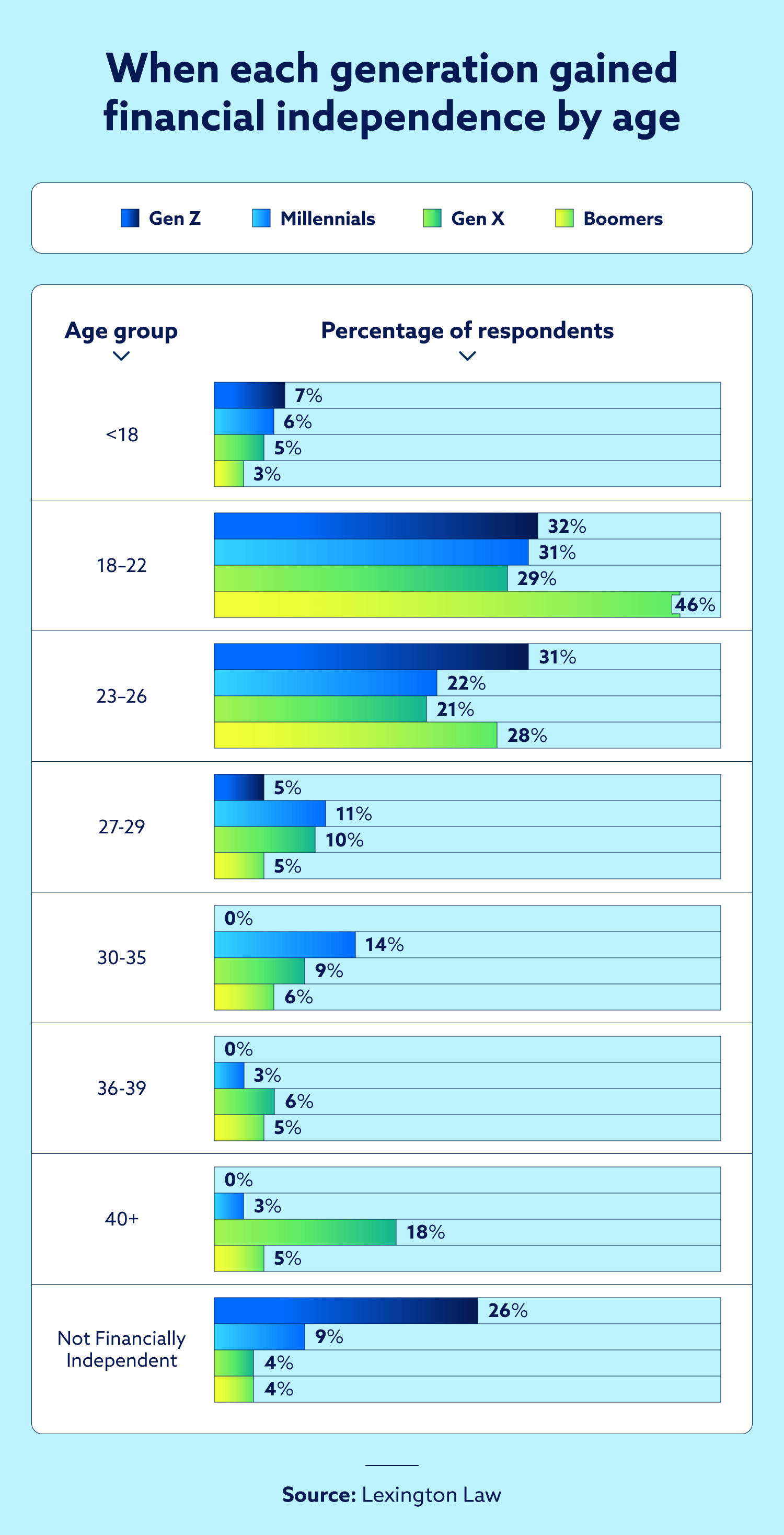

An additional fascinating searching for from our study is that 36 percent of Americans think Infant Boomers had the most effective possibility to develop wide range—greater than any type of various other generation. It’s not simply assumption. Almost fifty percent of Boomers (48 percent) state they got to economic self-reliance by age 22.

That very early self-reliance offered Boomers a beneficial running start on conserving, spending and constructing wide range. More youthful generations, on the various other hand, are economically dependent on household well right into their 20s and also 30s, according to the U.S. Division of the Treasury. With climbing expenses of living, today’s roadway to economic freedom looks a lot various from it provided for Boomers.

Gen X has one of the most cash (and the most awful overview)

Gen Xers might be making one of the most, yet they’re additionally really feeling the weight of it. Our study located that majority (54 percent) record earnings over $100,000, the highest possible throughout all generations. Still, virtually fifty percent (49 percent) state they’re cynical concerning their economic future.

Gen Xers additionally reported having one of the most assistance from their moms and dads—23 percent of them getting over $50,000—yet still having the bleakest 10-year overview.

It’s feasible this generation really feels captured between: taking care of maturing moms and dads while sustaining their grown-up youngsters. For Gen Xers, economic success might include equally as much tension.

Economic self-reliance maintains obtaining pressed even more out

Economic self-reliance is visibly showing up a lot behind it when did. While virtually fifty percent of Boomers (49 percent) were economically independent by age 22, just 36 percent of Gen Z got to that landmark in between 23 and 29, with 26 percent of them still relying upon adult assistance. Also 36 percent of Gen Xers didn’t end up being independent till after age 30.

As it ends up, greater earnings doesn’t constantly indicate an earlier begin. The study reported that 26 percent of those making $125,000-$149,999 were probably to end up being independent at age 40 or older, and a quarter (25 percent) of those making $200,000 or even more didn’t get to self-reliance till ages 30-35.

According to the U.S. Federal Book, climbing real estate expenses, stationary salaries and pupil funding financial debt all contribute. These financial problems, most likely lasting results of the 2008 economic downturn, appear to press economic self-reliance even more in the future.

This understanding can suggest just how typical—and essential—adult assistance has actually ended up being. With virtually 1 in 4 young people (ages 18-29) still relying upon aid from household, one can concur that today’s course to their adult years is extra rooted in household sources. While economic self-reliance is still the objective, its postponed timeline highlights the financial changes for several.

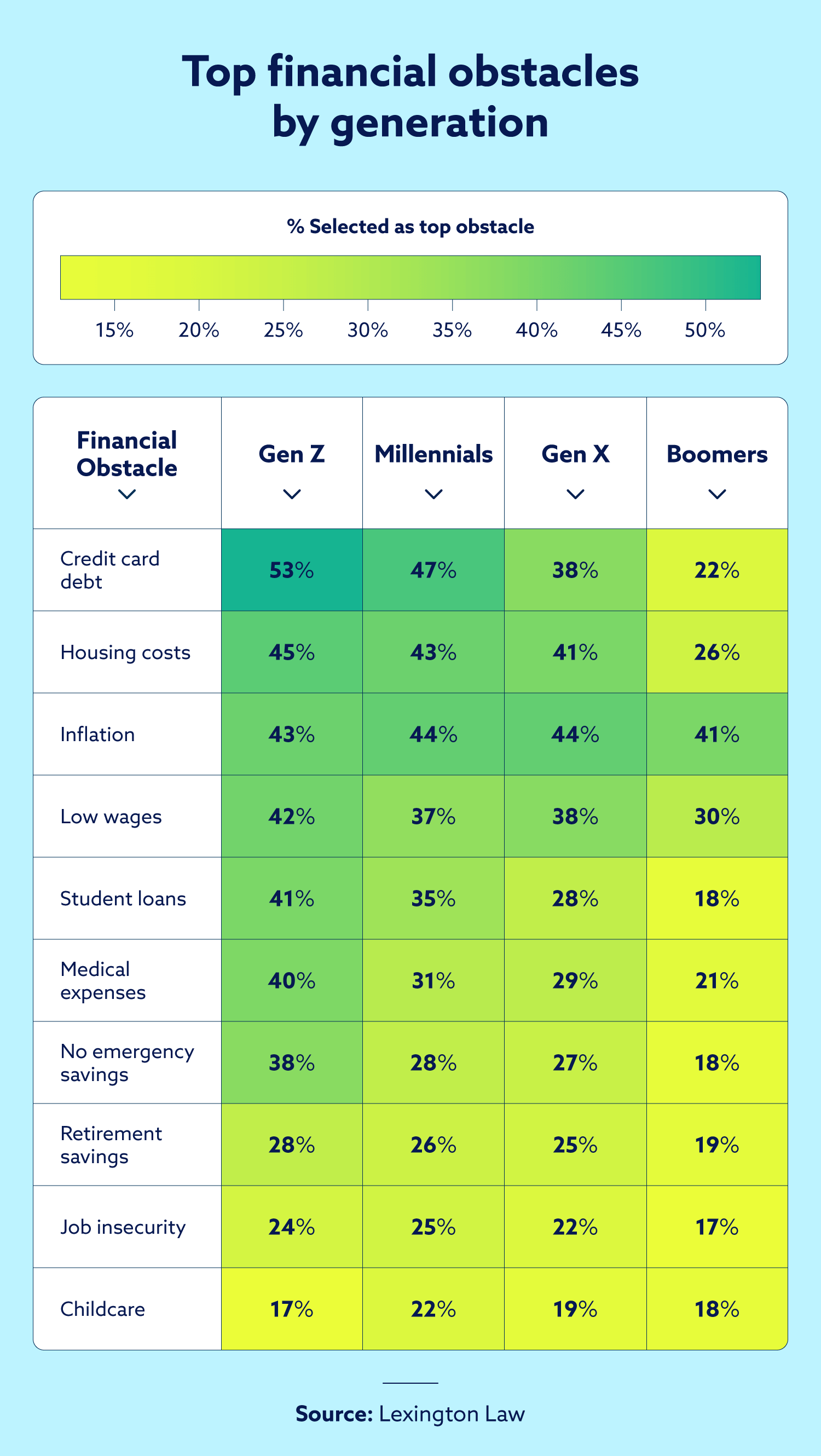

The #1 challenge to wide range structure, according to every generation

Throughout every generation, the greatest barricade to constructing wide range is clear: climbing expenses. Almost three-quarters (73 percent) state the climbing expense of living is squashing their capacity to conserve and develop wide range. From gas to grocery stores, basic American costs behaviors currently require a bigger earnings.

Real estate expenses can be found in 2nd at 65 percent, revealing simply exactly how way out of reach homeownership has actually ended up being for several. Additionally, while financial debt usually leads economic discussions, just 28 percent of participants stated it was their leading problem. Stationary salaries are the significant challenge, according to 49 percent of participants.

It doesn’t quit there. For Boomers specifically, medical care expenses are front and facility, with 62 percent calling it their greatest difficulty. These numbers appear to recommend that wide range structure isn’t nearly budgeting far better yet additionally making it through a pricey economic climate.

Long-lasting wide range begins with a tidy credit scores record

If there’s something this information explains, it’s that constructing wide range isn’t nearly what you can gain—it’s about where you begin and just how you expand from there. While some individuals obtain a monetary running start, several are dealing with climbing expenses and minimal assistance. That’s why variables you can regulate, like constructing credit score, end up being progressively essential for getting to economic objectives.

A solid credit rating can aid you receive far better prices and accessibility possibilities quicker. If you’re uncertain where you stand, obtain your complimentary credit score analysis to see what’s perhaps holding you back and what can be taken care of.

Technique

The study was carried out by SurveyMonkey Target market for Lexington Law Office. It was fielded in between June 20, 2025 and June 22, 2025. The outcomes are based upon around 1,000 finished studies.

In order to certify, participants were evaluated to be homeowners of the USA and over 18 years old. Information is unweighted, and the margin of mistake is around +/-2 percent for the general example with a 95 percent self-confidence degree.

Note: Articles have actually just been examined by the indicated lawyer, not created by them. The info given on this web site does not, and is not meant to, work as lawful, economic or credit score guidance; rather, it is for basic educational functions just. Use, and accessibility to, this web site or any one of the web links or sources included within the website do not produce an attorney-client or fiduciary connection in between the visitor, customer, or internet browser and web site proprietor, writers, customers, factors, adding companies, or their particular representatives or companies.