An business consortium within the UK is launching a CBDC retail pilot that includes a stay stablecoin asset.

“We’re wanting rigorously at how a UK central financial institution digital forex (CBDC) may work. However we now have not but determined to introduce one,” the Financial institution of England explains.

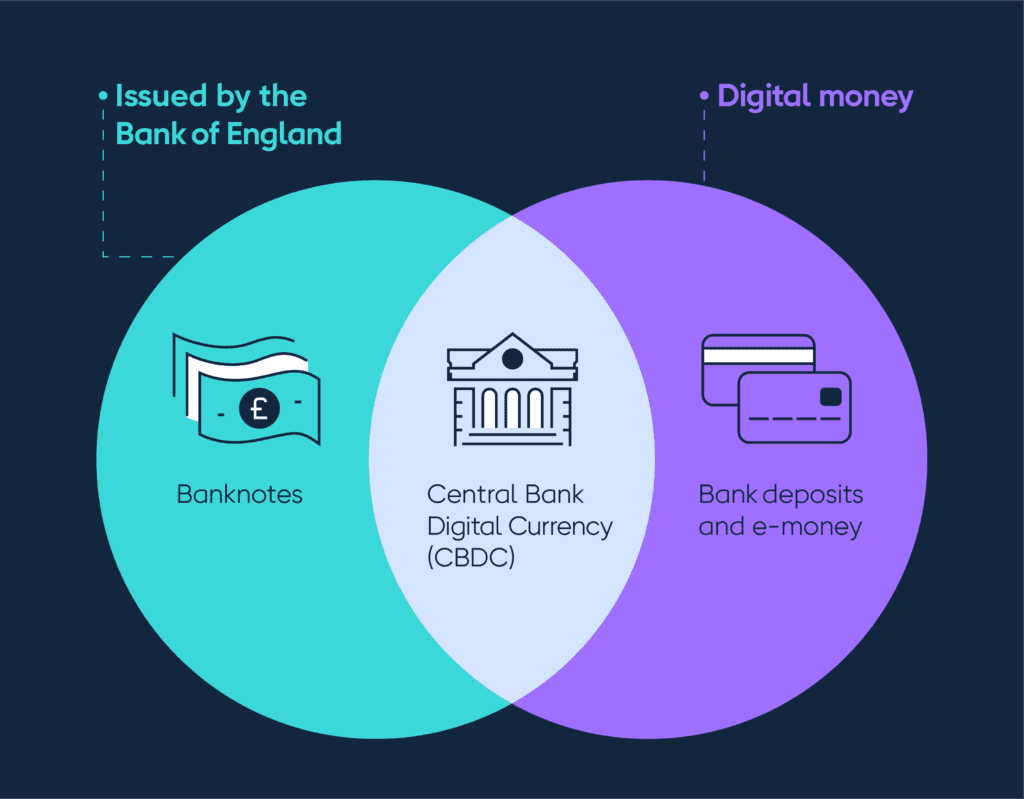

Their web site mentions names equivalent to ‘digital sterling’ or ‘Britcoin’ and emphasizes the distinction between CBCDs and cryptocurrencies.

Along with HM Treasury (HMT), they arrange a Central Financial institution Digital Foreign money Taskforce to supervise their work. They’re additionally working intently with different public authorities.

Jim Mignano, a former know-how marketing consultant and present assistant coverage researcher at RAND specializing within the intersection of cyber, finance, and worldwide relations, takes a constructive strategy to the initiative “The mission acknowledges that a number of, coexisting new digital cost programs have gotten more and more believable. It additionally seems to acknowledge that experimentation and session will probably be very important to illuminating and overcoming technical, business, and regulatory obstacles to implementation. I will probably be anticipating classes from the mission about hanging the suitable steadiness of publicly and privately administered programs, interoperability between programs, and harmonizing requirements throughout jurisdictions. It might additionally supply precious classes for making finance extra inclusive, primarily via fostering an business that embraces contributions from numerous walks of life in any respect ranges of duty. The UK has lengthy been a frontrunner in monetary innovation, and Mission New Period is poised to proceed this pattern into the period of latest digital funds.”

The panorama

In March 2020, the Financial institution of England revealed a dialogue paper on CBDC and outlined one potential strategy to design a central financial institution digital forex. In July 2021, they revealed their responses and produced a webinar based mostly on suggestions from the funds business, teachers, and different events.

In June 2021, they set out their pondering on the potential alternatives and dangers it might carry to the dialogue paper on new types of digital cash.

In November 2021, with HMT, they set out the subsequent steps for a UK CBDC. These subsequent steps embrace session in 2022 to assist them assess the case for a UK CBDC. Moreover, it can look at whether or not extra work must be achieved to develop an operational and technological mannequin.

How will it work?

The Financial institution of England already produces digital currencies for banks and different monetary establishments to make use of (reserves), however this proposal would create a digital forex for all residents.

Nonetheless, Molly Elmore, an analyst centered on the way forward for cash, digital belongings, blockchain & geopolitics, factors out, “there are only a few benefits for residents if nations transfer in direction of retail CBDCs. Presently, most individuals use digital money to pay for items and providers utilizing bank cards, debit playing cards, and Venmo. Residents at present have decisions, so in case you are sad along with your financial institution or bank card supplier, you may change to a different competitor providing the same service. If there’s a CBDC, client selection is gone. Nations solely have ONE central financial institution with management over the financial coverage. Except you might be able to maneuver to a different nation, you can’t merely change central banks.”

Massimo Buonomo, a global AI, metaverse, and blockchain skilled and former advisor to UN Economics Fee For Europe, added his ideas.

“CBDCs usually are not in place besides in just a few international locations. Even there, they don’t seem to be used extensively however simply in pilot circumstances. These centralized programs are good for Know Your Shopper (KYC) and Anti-money laundering (AML) functions. In different phrases, the cash provide continues within the arms of centralized establishments. I’d say that each decentralized cryptocurrencies can’t be in contrast totally to worldwide cost programs as a result of they obey completely different guidelines and have completely different goals. In fact, KYC/AML points needs to be thought-about when discussing bitcoin and stablecoins. Additionally, volatility is much less a problem for stablecoins than for bitcoins. Nonetheless, stablecoins need to be severely audited to see whether or not they have severe belongings that again the stablecoins in circulation.”

Motivations behind CBDCs

However what the funds system appears to be like like and the motivations behind their manufacturing as digitalization continues generally is a regarding query for central banks and residents worldwide.

Up to now, Elmore factors out the potential political penalties of CBDCs. “Residents aren’t more likely to need an unelected group of central bankers deciding what we will purchase or what we even owe in taxes. In most international locations, together with the US and the UK, the central financial institution officers usually are not elected, so you may’t vote out corrupt or ineffective central financial institution leaders.”

For instance the potential influence of CBDCs, she makes use of China for instance. “China has been utilizing retail CBDCs to subdue and management their residents. A social credit score rating system is linked, so if a citizen speaks towards the state, their checking account can routinely be fined. It’s unlikely that Chinese language residents discover such a system useful. Nonetheless, they weren’t given a selection. In case you have a selection and stay in a rustic the place the voting inhabitants can voice their pursuits, say no to retail CBDCs.”

In keeping with the European Union, Institute for Safety Research, the Chinese language authorities is already utilizing blockchain to collect proof towards dissidents on-line.

Of their report ‘China’s Blockchain and Cryptocurrency Ambitions, ‘ the authors look at how blockchain-based platforms have been used to collect proof on on-line media defaming Chinese language revolutionary martyrs. Blockchain might additionally be certain that knowledge within the social credit score system is at all times accessible and can’t be modified by unauthorized actors. This isn’t that far-fetched as, in December 2019, a seminar was organized in Beijing with the title ‘blockchain know-how helps China’s new social credit score system.’

Thus to Elmore’s issues, there’s some precedent.

She continues, “If retail CBDCs solved a painful and costly downside in society, it will be price discussing to see if the professionals outweigh the cons. However for residents, they don’t. Wholesale CBDCs are a really separate concern, the place funds are despatched between banks utilizing the blockchain. They fill a significant position and can enhance the prices and effectivity of sending cash across the globe. However retail CBDCs, though they may sound related, are fairly completely different.

China’s motivation can nonetheless be multifaceted, because the Carnegie Endowment for Worldwide Peace factors out.

That China has solely a two % share on this planet’s overseas change reserves, and due to this fact CBDCs could also be their approach of constructing a dent within the U.S.-dominated international monetary system.

Within the report ‘China’s Digital Yuan: An Various to the Greenback-Dominated Monetary System,’ the authors recommend that the digital yuan might show to be China’s most influential and noteworthy assault on the US, which can even be an element behind establishing a CBDC.

“To problem the greenback’s hegemony and internationalize its forex, China must transfer away from the greenback and the cost rails dominated by the greenback. One of the simplest ways to concurrently do each could be by introducing greenfield cost rails like CBDC. However to take action, China must work out agreements and mechanisms for exchanging its digital yuan with the remainder of the world. As CBDCs are a comparatively new know-how with no worldwide requirements and design, China might develop into the usual setter.”

UK motivations

The Financial institution of England states that the motivation behind their consideration of CBDCs are as a result of the best way folks select to pay for issues is altering. Individuals are utilizing money much less and have new methods of paying for gadgets as a result of fintech revolution and open banking.

In keeping with UK Finance, throughout 2020, the variety of contactless funds made within the UK elevated by 12percentto 9.6 billion. Over 1 / 4 (27%) of all UK funds have been contactless funds. 83% of individuals within the UK now use contactless, with no age group or area falling under 75% utilization. There are over 135 million contactless playing cards in circulation, masking 88percentof debit playing cards and 81percentof bank cards.

These modifications imply new alternatives and dangers for which the Financial institution of England must plan.

Nonetheless, the Financial institution of England notes, “we all know some folks like to make use of money. So, if we did create a CBDC for the UK, we’d preserve issuing money too. That approach you might select the way you’d wish to pay for one thing.

What’s subsequent?

The Financial institution of England is talking to companies and communities to find out what influence a CBDC would have on them.

Additionally they work with worldwide companions and organizations such because the Financial institution for Worldwide Settlements. And they’re working with finance ministries and central banks in different international locations, particularly within the G7.

Additionally they have the Engagement and Expertise Discussion board to maneuver this ahead.

The CBDC Engagement Discussion board appears to be like in any respect points of a central financial institution’s digital forex other than the know-how it would use.

The discussion board helps them perceive the sensible challenges of designing, implementing and working a CBDC, which embrace:

- How a forex will probably be used (‘use circumstances’)

- Useful wants of customers

- The position of the private and non-private sectors

- Monetary and digital inclusion

- Information and privateness implications

It consists of representatives from monetary establishments, civil society organizations, and retailers. They this discussion board collectively with HM Treasury.

CBDC Expertise Discussion board examines the know-how {that a} central financial institution may use to create a digital forex. The discussion board allows them to contain folks with a variety of experience and views. This helps them perceive the technological challenges of designing, implementing, and working a CBDC.

The discussion board’s members come from numerous monetary establishments, universities, fintechs, infrastructure suppliers, and know-how companies.

Purposes for each boards have closed.

Associated:

{kind=link}