{kind=link}

The knowledge offered on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation. See Lexington Regulation’s editorial disclosure for extra info.

A credit score restrict is the utmost sum of money an individual can at the moment borrow from a monetary establishment.

Bank cards and features of credit score allow us to borrow funds from banks, credit score unions and numerous firms. Credit score limits decide simply how a lot cash we will borrow with out incurring penalties like overdraft charges. People are likely to progressively enhance their credit score limits as they age; Experian® reported that the typical bank card restrict for Era Z in 2022 was $11,290, whereas the typical credit score restrict for Child Boomers was $40,318 that very same 12 months.

“What’s a credit score restrict?” could also be such a standard query as a result of a number of components can affect an individual’s restrict. We’ll discover this query and focus on tips on how to enhance your credit score restrict.

Key takeaways:

- Monetary establishments largely set credit score limits primarily based on a borrower’s credit score historical past.

- Credit score utilization relies in your credit score restrict and your obtainable credit score.

- Frequently working towards good credit score habits can enhance your restrict

Desk of contents:

How are bank card limits decided?

Your credit score restrict is set by the establishment you borrow cash from, whether or not they’re a financial institution, a credit score union or a authorities company. Credit score limits take a number of components under consideration, together with your revenue and credit score rating. Individuals with larger credit score scores and revenue are usually accepted for larger credit score limits as a result of lenders view them as financially accountable folks.

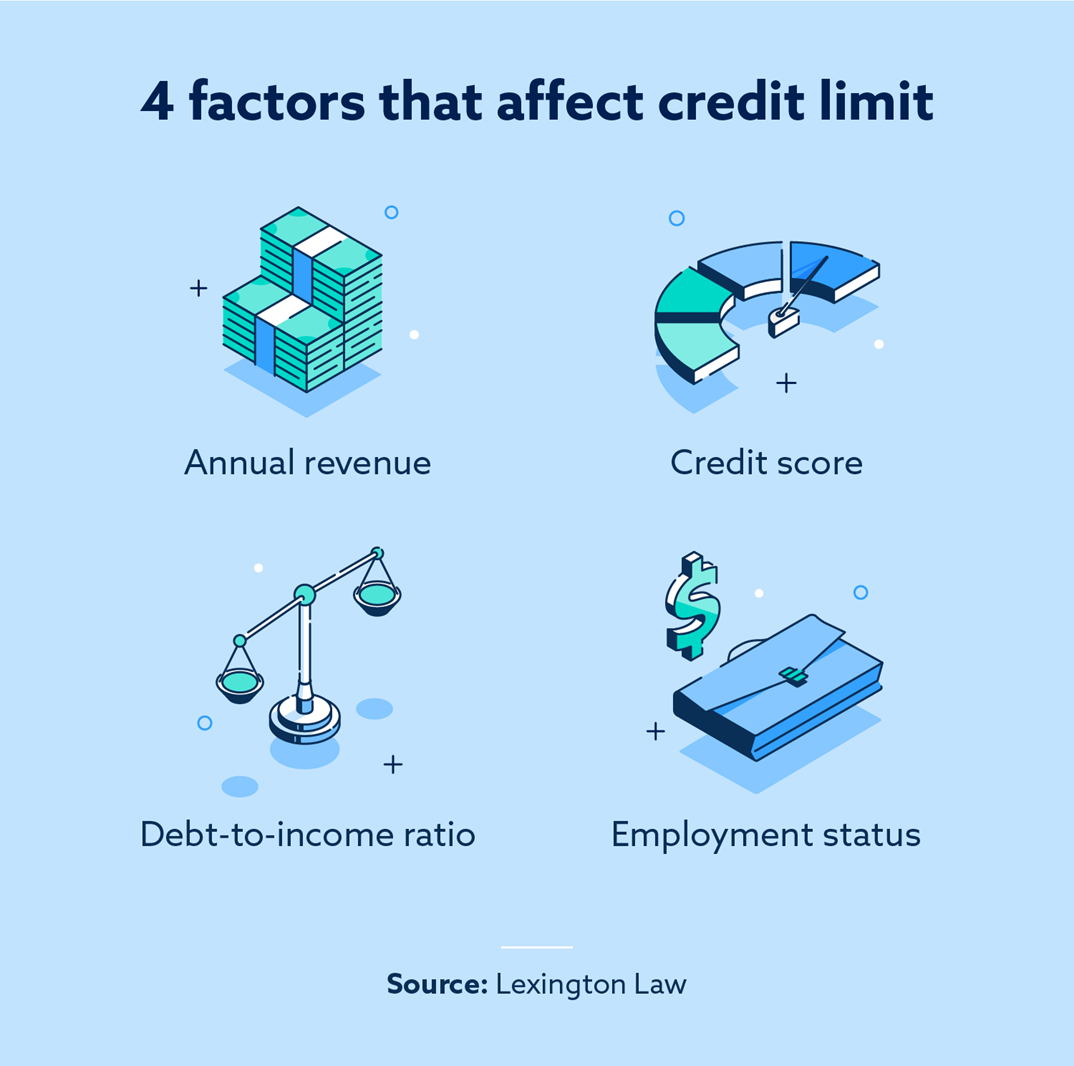

Annual income

When a borrower applies for credit score or asks for a credit score restrict enhance, lenders have a look at annual income. From their perspective, a borrower with extra revenue is extra prone to make their funds on time—and vice versa.

Credit score rating

Credit score scores assist us qualify for auto loans, mortgage rates of interest and bank cards—plus the bounds we’ll obtain when accepted. In case you have good credit score, then you definately’ll possible be eligible for high-limit bank cards from the get-go.

Debt-to-income ratio

Lenders can use your debt-to-income ratio to set your credit score restrict by weighing your month-to-month debt funds towards your whole revenue. A low debt-to-income ratio can immediate lenders to supply larger credit score limits since your spending habits present you frequently make accountable monetary selections.

Employment standing

Your employment standing can even have an effect on your credit score restrict largely attributable to timing. When you apply for a bank card or ask for a restrict enhance whilst you’re looking for a job, you’ll more than likely obtain a decrease restrict than you’ll as a full-time worker.

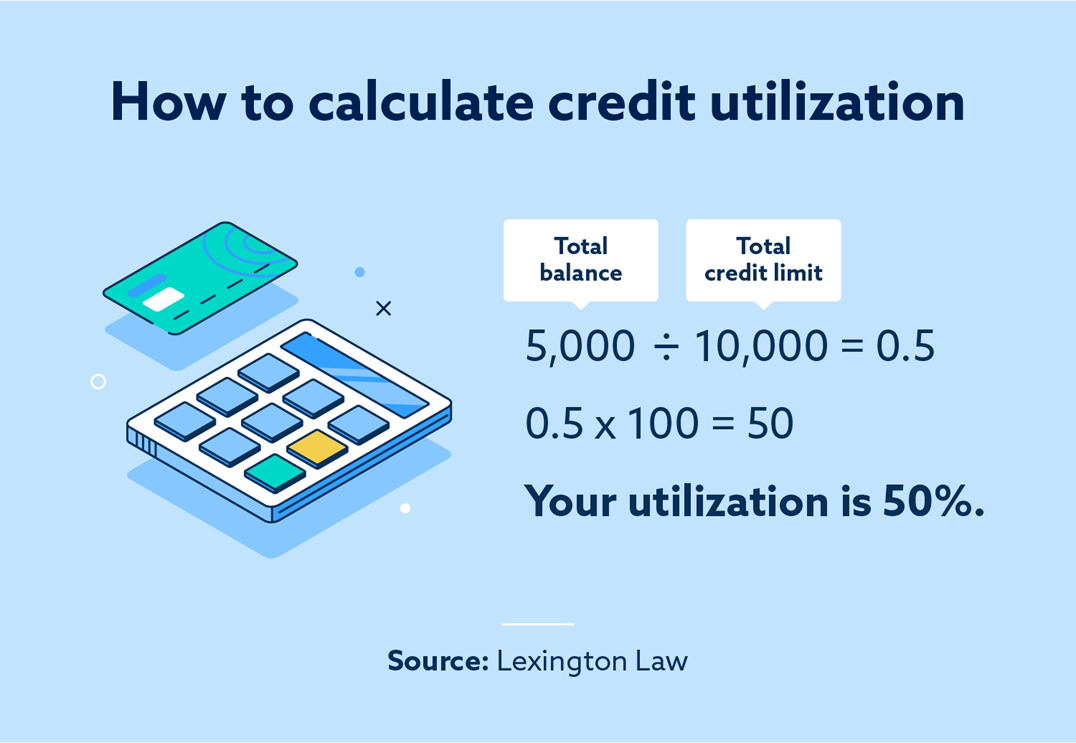

Credit score restrict vs. obtainable credit score

An individual’s credit score restrict and their obtainable credit score are closely tied collectively, which may trigger folks to confuse these two phrases. To make clear, your obtainable credit score refers back to the sum of money you may nonetheless borrow after calculating your debt. However, your credit score restrict refers back to the whole sum of money that your lender permits you to borrow.

For instance, in case you have a $10,000 credit score restrict and spend $5,000, you’ll nonetheless have one other $5,000 in obtainable credit score that you could entry throughout this billing cycle. Your credit score utilization ratio is calculated by weighing your obtainable credit score towards your whole credit score restrict. On this case, your credit score utilization could be 50 p.c.

How does your credit score restrict have an effect on your credit score rating?

Everytime you ask a lender to extend your credit score restrict, they’ll carry out a exhausting inquiry to assessment your credit score historical past and assist inform their choice. Inquiries briefly trigger your rating to dip, which is why standard knowledge recommends not making an attempt to extend your credit score restrict proper earlier than making use of for one thing very important—like a house or a brand new automotive.

Credit score limits can even have an effect on your rating when you persistently have a excessive utilization ratio. Bank cards with excessive limits sometimes assist debtors preserve decrease utilization ratios, which is helpful for credit score well being.

What occurs when you go over your credit score restrict?

Exceeding your credit score restrict can have adverse penalties, particularly when you achieve this repeatedly. A number of the drawbacks you may encounter embrace:

- Account assessment: A lender might assessment your longtime credit score habits, which might probably result in a credit score restrict discount.

- Credit score rating adjustments: Credit score utilization makes up 30 p.c of your FICO® credit score rating. Repeatedly going over your credit score restrict might considerably harm your credit score.

- Elevated rates of interest: Relying in your lender’s insurance policies, they might situation a penalty APR on the offending account, which could be a lot larger than your commonplace price.

- Overdraft charges: Most lenders will cost a $35 overdraft (or over-the-limit charge) after a specified time interval when you don’t repay your stability.

The right way to enhance your credit score restrict

When you persistently make your month-to-month funds on time and preserve your utilization low, the bank card issuer might approve your request to extend your restrict. However bear in mind to permit six to 12 months earlier than asking. Your issuer in all probability received’t elevate your restrict after only one or two months of opening the account or when you’ve been making late funds.

Some bank card issuers will actively enhance your restrict after they assessment your account historical past. Typically, they’ll ask you to replace your revenue. When you’ve earned a elevate lately, you may present that info, and the lender might enhance your restrict. When an issuer evaluations your account like this, it doesn’t trigger a tough inquiry since you didn’t ask for them to assessment the account.

Work in your credit score with Lexington Regulation Agency

Bank cards are unbelievable sources that may positively affect your life when used responsibly. Even when you get accepted for a excessive credit score restrict, it’s finest to observe your spending and borrowing habits. Lexington Regulation Agency provides nice companies like credit score training instruments and credit score report evaluation which will enable you along with your credit score.

Notice: Articles have solely been reviewed by the indicated legal professional, not written by them. The knowledge offered on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation; as a substitute, it’s for normal informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or sources contained inside the website don’t create an attorney-client or fiduciary relationship between the reader, person, or browser and web site proprietor, authors, reviewers, contributors, contributing corporations, or their respective brokers or employers.