{kind=link}

Is a good credit score rating good?

In case your credit score rating falls into the “truthful” vary, lenders might view you as a subprime borrower or a monetary danger and should hesitate to give you a line of credit score. Decrease scores point out a less-than-desirable credit score historical past, and lenders might contemplate these with truthful scores extra prone to default on loans.

You would possibly nonetheless qualify for bank cards and loans with a good rating, however they may seemingly include higher-than-average rates of interest and up-front deposits. The truth is, debtors with truthful scores pay about far more in curiosity on bank cards and different mortgage sorts than debtors with excellent scores. Some lenders would possibly even reject your utility altogether in case your rating falls beneath their minimal requirement for approval.

To keep away from this, it’s best to attempt to enhance your credit score. Transferring your rating into the next class over time might earn you decrease rates of interest on house, pupil and private loans and enhance your possibilities of approval when submitting rental functions.

Thankfully, for these with a decrease rating, lenders additionally contemplate different components when calculating the danger related to lending to the person, comparable to proof of revenue or employment historical past. Minimal necessities for approval additionally differ by lender, so a decrease credit score rating doesn’t routinely disqualify a person from taking out credit score.

What’s the common credit score rating?

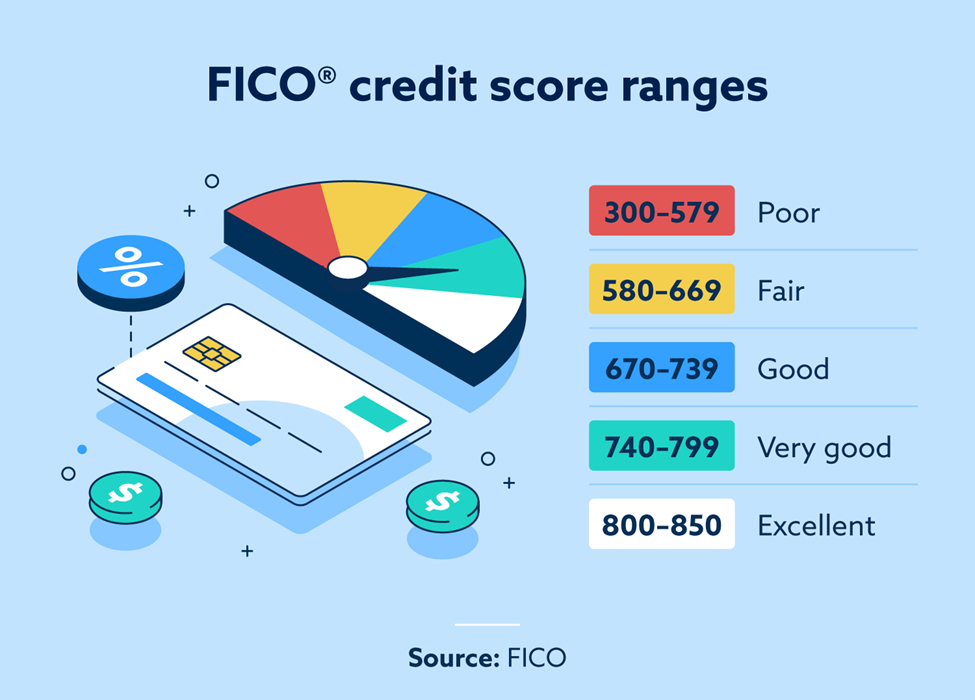

The common FICO rating within the U.S. was 714 as of Q3 2022. A median FICO rating of 711 falls into the “good” class, indicating that an rising variety of People have a credit score rating that’s both good, excellent or distinctive.

That stated, lenders don’t contemplate the nationwide common when deciding what an appropriate credit score rating is. It may be useful to see how your rating stacks up, however the nationwide common received’t have an effect on your possibilities of being permitted for brand new credit score.

What lowers your credit score rating?

In case your credit score rating is decrease than you need it to be, it’s necessary to contemplate what components may be hurting it. A number of the most typical actions that trigger credit score scores to drop embrace lacking funds, defaulting on accounts and constantly utilizing greater than 30 p.c of your accessible credit score.

Making use of for lots of credit score in a brief interval may harm your rating. Credit score inquiries stay in your report for 2 years, and plenty of inquiries displaying up directly might point out to lenders that you’re in a tricky monetary scenario or have utilized for extra credit score than you possibly can deal with. After you have recognized the actions hurting your credit score, you can begin taking steps to treatment them.

Honest vs. good credit score rating

In the case of making use of for loans and opening new traces of credit score, a very good credit score rating can qualify you for implausible alternatives. Good credit score is one rung above truthful credit score and one stage beneath excellent credit score, based on FICO. Nonetheless, people with truthful credit score shouldn’t really feel discouraged—having a rating inside the 580 to 669 vary can nonetheless qualify you for higher loans than you could have been restricted to when you had poor credit score.

And fortuitously, it’s doable to progressively rework a good credit score rating into a very good one by training accountable monetary habits.

How one can enhance your truthful credit score rating

Thankfully, credit score scores can simply change over time. You’ll be able to entry your credit score report free of charge every year from Equifax®, Experian® and TransUnion® to determine enchancment areas. When you observe any components that may very well be hurting your credit score, strive the next steps to enhance your possibilities of qualifying for higher phrases and charges over time.

Preserve your credit score utilization ratio low

Your credit score utilization ratio refers back to the share of accessible credit score that you’re utilizing at any given time. Attempt to hold your credit score utilization share beneath 30 p.c. It might enhance your credit score, and lenders might be extra prone to approve your future credit score functions.

Pay payments on time

Your cost historical past makes up 35 p.c of your FICO credit score rating, so it’s necessary to pay your payments on time if you wish to enhance your credit score. When you’ve struggled to pay on time, contemplate organising computerized funds. It’s additionally necessary to get present on any late funds as quickly as you possibly can.

Verify your credit score stories and dispute any errors

Inaccuracies seem on credit score stories extra typically than you would possibly assume. Inaccurate data might hurt your credit score, so it’s necessary to commonly monitor your stories from all three credit score bureaus and dispute any errors. The method is free and mustn’t harm your credit score.

Seek the advice of a credit score restore guide

When you’re struggling to enhance your credit score by yourself, contemplate searching for out a credit score restore guide. They may also help you design a plan to handle your credit score and enhance your credit score over time. Looking for out credit score restore providers can even not harm your credit score. Realizing how a good credit score rating can influence your possibilities of approval is step one within the course of of higher managing your credit score. If you wish to begin bettering your credit score, bear in mind to commonly monitor your credit score stories, keep updated in your funds and tackle errors or search out a credit score restore service while you discover inaccuracies in your credit score stories.

Be aware: Articles have solely been reviewed by the indicated legal professional, not written by them. The knowledge supplied on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation; as an alternative, it’s for basic informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or sources contained inside the web site don’t create an attorney-client or fiduciary relationship between the reader, consumer, or browser and web site proprietor, authors, reviewers, contributors, contributing corporations, or their respective brokers or employers.