{kind=link}

The data offered on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation. See Lexington Legislation’s editorial disclosure for extra info.

A pupil mortgage grace interval is a set period of time granted to college students earlier than they have to pay down their loans. Grace interval phrases differ based mostly on mortgage varieties.

A pupil mortgage grace interval is a set period of time granted to college students earlier than they have to pay down their loans. Grace interval phrases differ based mostly on mortgage varieties, and a few pupil loans don’t have grace durations in any respect.

The common pupil mortgage debt in 2022 was $37,104 per borrower, which helps reinforce why grace durations are so necessary to current graduates. Studying how grace durations work—and whether or not they are often prolonged—might help college students be extra ready for all times after commencement.

Key takeaways

- Federal pupil loans often have a six-month grace interval.

- A pupil mortgage grace interval might be prolonged underneath sure circumstances, similar to army service.

- Chances are you’ll be eligible for pupil mortgage forgiveness afterward in your profession.

Desk of contents:

How lengthy is my pupil mortgage grace interval, and when does it begin?

Most pupil loans have a grace interval of six months. Right here’s the breakdown:

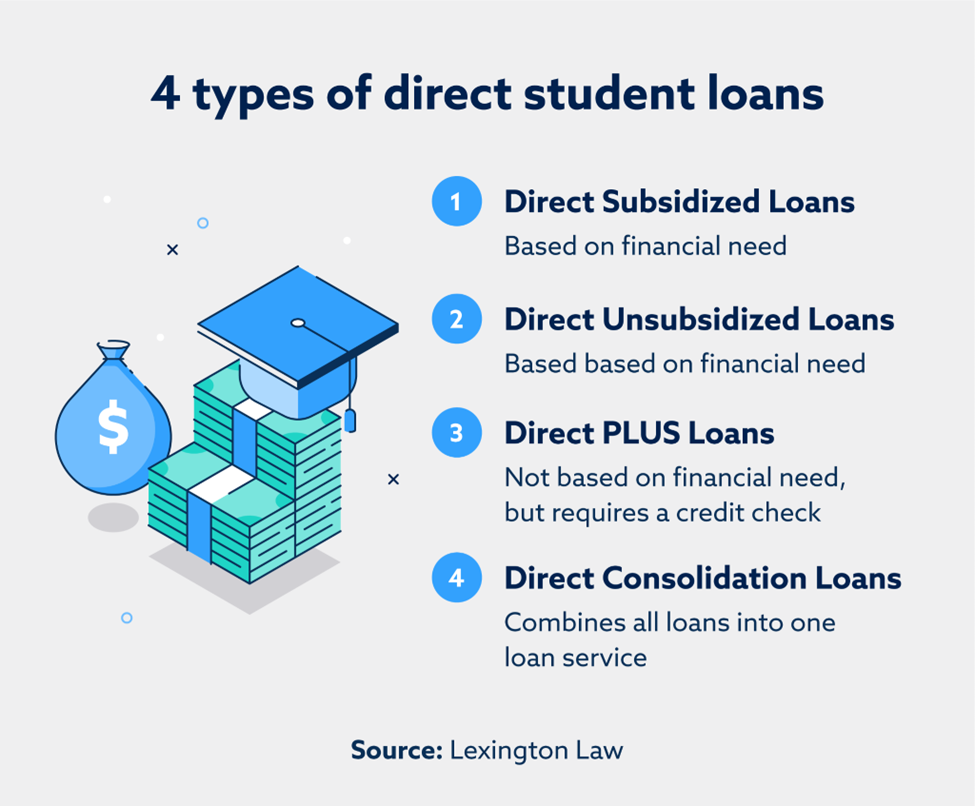

- Federal direct sponsored loans and direct unsubsidized loans: Six months

- Federal Stafford sponsored and unsubsidized loans: Six months

- Federal PLUS loans: Six months (mother and father of scholars could must request the six-month grace interval on the mortgage utility)

- Federal Perkins loans: 9 months

- Personal loans: Grace durations differ by the lender. Many non-public pupil loans supply a six-month grace interval, however some require reimbursement as quickly because the mortgage is disbursed. The mortgage settlement ought to state when funds are due.

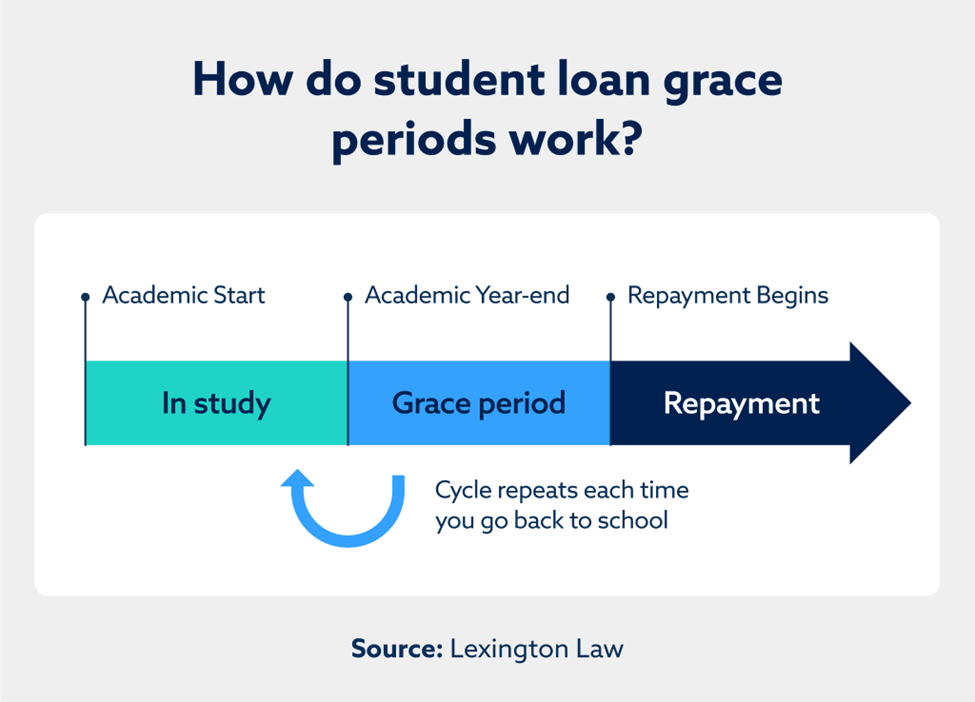

For many loans, together with federal pupil loans and the vast majority of non-public pupil loans, the grace interval begins as quickly as a pupil drops under half-time enrollment. This implies dropping sufficient courses, taking a spot yr or graduating are all conditions that may set off the beginning of your grace interval.

The definition of “half-enrollment” varies at every establishment, so be sure you verify along with your college and perceive the brink.

Can my grace interval change?

Sure, your pupil mortgage grace interval can change, both by being minimize quick or by restarting. Much like a bank card grace interval, some elements that may have an effect on your pupil mortgage embody:

- Lively army obligation: In case you’re known as to lively army obligation for greater than 30 days earlier than your grace interval formally ends, your six-month grace interval will restart when you’re discharged from service.

- Consolidating your loans: Consolidation can forfeit/cancel out no matter time stays in your pupil mortgage grace durations. You can even wait to consolidate till the tip of your grace interval to take full benefit of the payment-free time available.

- Re-enrolling in class: Re-enrolling in class with a half-time course load or extra earlier than your grace interval ends will successfully lengthen your grace interval. Do you have to drop under half-time enrollment (through withdrawing, dropping courses or graduating), you’ll be given a six-month grace interval.

What occurs when the grace interval ends?

Earlier than your grace interval ends, it’s best to obtain a reimbursement schedule out of your mortgage servicer that particulars how a lot your funds are and after they’re due.

For these questioning who to contact for questions on reimbursement plans, we suggest contacting your mortgage servicer. They might help you request a unique reimbursement plan (similar to income-driven reimbursement plans) and be taught what different choices you might have for reimbursement (similar to mortgage consolidation, deferment and forbearance). These requests usually take months to approve, so contact your mortgage supplier as quickly as doable.

Regarding reimbursement plans, it’s completely tremendous to contact your supplier when you really feel that you could’t afford the preliminary proposed cost schedule. It’s finally higher to vary the reimbursement plan than funds sooner or later.

Can I make funds throughout the pupil mortgage grace interval?

Sure, and you’ll even make funds whilst you’re nonetheless in class. Early funds are a good way that will help you repay your mortgage sooner and graduate with a smaller mortgage and fewer stress. In case you can’t afford full funds, protecting the price of curiosity is one other good way that will help you repay your pupil loans sooner.

In case you’re questioning what will increase your complete mortgage steadiness, it’s best to know that unpaid curiosity can doubtlessly trigger a debt to balloon over time. It’s best to obtain a letter or e mail out of your mortgage supplier reminding you that you could repay your curiosity earlier than it’s added to your steadiness or capitalized.

How do pupil loans have an effect on credit score?

Scholar loans can have an effect on credit score each positively and negatively, similar to all loans. For instance, persistently making well timed funds in your mortgage could cause your credit score to enhance over time. Nevertheless, when you miss or make late funds, you’ll see a drop in your credit score as a result of a damaging cost historical past.

A pupil mortgage going into default can even drastically influence your credit score. Default occurs when you miss no less than 9 months of funds, which is able to immediate collectors so as to add this as a derogatory mark in your credit score stories. This damaging merchandise can keep in your stories for as much as seven years, presumably shifting you nearer to a weak credit rating and impacting your skill to be accredited for future credit score.

Notice that your mortgage going into default doesn’t imply you’ll be able to ignore your funds. In case you do, mortgage suppliers can take motion towards you, leading to wage garnishment, withholding tax refunds and making use of extra mortgage charges or curiosity accruals.

In case you can’t make your mortgage funds anymore, attain out to your mortgage supplier to grasp your choices.

Capitalize in your pupil mortgage grace interval with Lexington Legislation Agency

As you repay your pupil loans, you should watch your credit score stories to verify every little thing is reported precisely. Even one misreported late or missed cost can considerably influence your credit score. In case you’re uncertain the place to begin with credit score report errors, let the staff at Lexington Legislation Agency assist. We are able to give you a free credit score report evaluation to assist get you began.

Notice: Articles have solely been reviewed by the indicated legal professional, not written by them. The data offered on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation; as a substitute, it’s for basic informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or assets contained throughout the website don’t create an attorney-client or fiduciary relationship between the reader, person, or browser and web site proprietor, authors, reviewers, contributors, contributing corporations, or their respective brokers or employers.