{kind=link}

The data offered on this web site doesn’t, and isn’t meant to, act as authorized, monetary or credit score recommendation. See Lexington Legislation’s editorial disclosure for extra data.

A certified consumer is a person added to a bank card by the proprietor of the account or major cardholder. The approved consumer, additionally known as the extra cardholder, could make purchases utilizing the bank card, though the duty to make funds falls on the first cardholder.

Constructing credit score from scratch generally is a tough job, particularly for these with restricted credit score information. One approach to get your toes moist with credit score is by changing into a licensed consumer on another person’s account. As a licensed consumer, you possibly can leverage another person’s constructive credit score habits to enhance your individual creditworthiness.

Nonetheless, there are essential elements to contemplate earlier than changing into a licensed consumer your self or including a licensed consumer to your account. Learn on to be taught extra.

Desk of contents:

What’s a licensed consumer?

A certified consumer is an individual added to another person’s bank card account who has permission to make costs. The principle consumer who owns the account is the first cardholder, whereas a licensed consumer is typically known as a further cardholder.

Who may be a licensed consumer?

Anybody may be a licensed consumer, offered they meet the cardboard issuer’s necessities and the first cardholder provides them to the account. Sometimes, the first cardholder and approved consumer have a longtime, trusted relationship.

Listed below are the most typical eventualities the place including a person to your account is useful.

- Mother or father/little one: Mother and father could add their kids as approved customers to their account to assist them construct credit score historical past and provides them entry to the road of credit score for emergencies or household bills.

- Employer/worker: Enterprise homeowners could add trusted staff as approved customers for business-related bills.

- {Couples}: {Couples} could designate one partner as the first cardholder and the opposite partner because the approved consumer, particularly when one accomplice has the next credit score rating than the opposite.

Is a licensed consumer answerable for bank card debt?

No, being a licensed consumer doesn’t make you answerable for paying bank card debt. Whereas a licensed consumer could make purchases, fee duties fall to the first cardholder. Licensed customers don’t have any obligation to make funds.

How does being a licensed consumer have an effect on your credit score?

Accounts you’re a licensed consumer of are usually included in your credit score report, which may help you construct credit score historical past. Often known as piggybacking credit score, this lets you use the first cardholder’s constructive credit score habits to construct your credit score.

Whereas being a licensed consumer may help improve your credit score rating, it could actually even have the alternative impact. If the first cardholder falls behind on funds or maintains a excessive credit score utilization ratio, this will negatively impression your credit score.

It’s essential to notice that not all bank card issuers report approved consumer exercise to the three main credit score bureaus. Take into account checking with the first cardholder’s issuer earlier than changing into a licensed consumer to ensure they report back to the credit score bureaus.

The way to add a licensed consumer

So as to add a licensed consumer, attain out to your bank card firm on-line, by telephone or in-person. Your bank card firm will doubtless require the approved consumer’s identify, tackle, start date and Social Safety quantity so as to add them to the account.

When you add somebody as a licensed consumer, your bank card firm will mail you a second card that the approved consumer can use, though you possibly can resolve whether or not or not you give it to them. Take into account that you don’t want to offer the approved consumer a bodily card for them to obtain the credit-building advantages.

Listed below are further tricks to keep in mind when including a licensed consumer:

- Solely add approved customers you belief since they’ll have entry to your credit score line.

- In case your bank card firm presents this selection, contemplate establishing spending limits for approved customers to forestall overspending.

- Arrange alerts to inform you when a licensed consumer makes a purchase order.

The way to take away a licensed consumer

You’ll be able to simply take away a licensed consumer in case your circumstances have modified. Equally to including a licensed consumer, simply contact your bank card firm and request the approved consumer be faraway from the account. Take into account additionally contacting the approved consumer to inform them that you simply’re eradicating them from the account.

Listed below are some circumstances in which you’ll need to take away a licensed consumer out of your account:

- There’s been a change in relationship: For instance, in case your accomplice is a licensed consumer in your account and also you break up

- The account has been misused: If a licensed consumer is overspending in your account and negatively affecting your funds. For instance, in case your teen’s spending habits are uncontrolled

There are additionally eventualities in which you’ll need to take away your self as a licensed consumer from another person’s account, comparable to:

- You achieved monetary independence: In case you’ve established a credit score historical past and not want entry to the account, contemplate eradicating your self to handle your funds independently.

- The first cardholder’s poor credit score habits are affecting your credit score rating: If the first cardholder is falling behind on funds, your credit score may additionally take successful, so it’s greatest to chop ties.

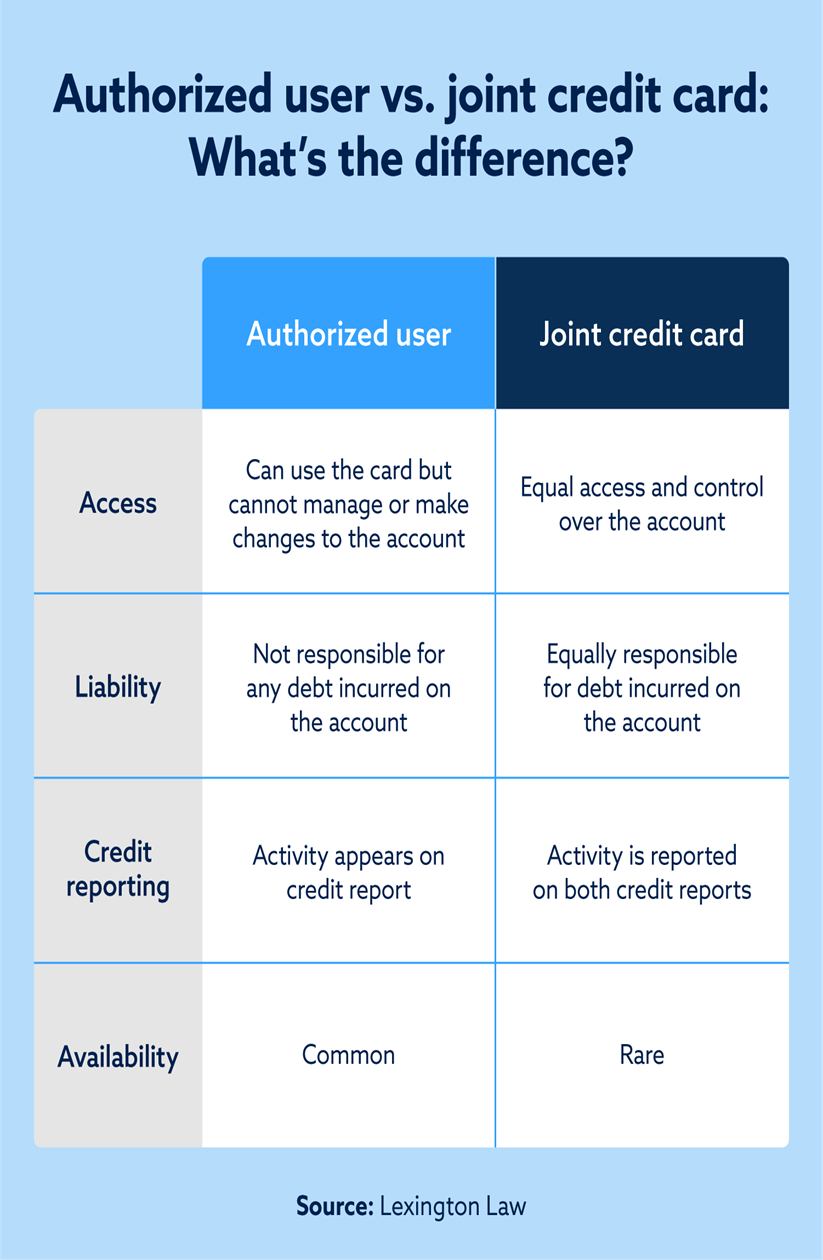

Joint bank card vs. approved consumer

A joint credit score card permits two folks to share one account equally. The principle distinction between a licensed consumer and a joint bank card is who’s legally obligated to make funds. Whereas each events are answerable for paying debt on a joint card, a licensed consumer isn’t required to make funds.

Take into account that fewer bank card issuers are providing joint accounts since corporations choose that just one particular person is chargeable for the account. In the meantime, most bank card issuers supply the choice so as to add approved customers.

Licensed consumer FAQ

Nonetheless not sure whether or not changing into a licensed consumer is best for you? We’ve answered some widespread questions under.

How previous do you must be to be a licensed consumer on a bank card?

Some bank card issuers have age necessities starting from 13 to 16, whereas others don’t have any minimal age requirement.

How lengthy does it take for approved consumer accounts to indicate in your credit score report?

Licensed consumer accounts will usually seem in your credit score report inside 30 to 45 days after you’re added to the account, so long as your bank card issuer stories to the credit score bureaus.

What’s the distinction between having a cosigner and changing into a licensed consumer?

A cosigner shares duty for repaying the debt, whereas a licensed consumer isn’t legally obligated to make funds.

Monitoring your credit score as a licensed consumer

Changing into a licensed consumer is a good way to kick-start your credit score journey. As you begin to construct credit score, it’s essential to observe your credit score and be sure that no inaccurate destructive objects are impacting your rating.

Once you join a free credit score evaluation with Lexington Legislation Agency, you’ll obtain your credit score rating, credit score report abstract and a credit score restore suggestion. View your credit score snapshot immediately.

Observe: Articles have solely been reviewed by the indicated lawyer, not written by them. The data offered on this web site doesn’t, and isn’t meant to, act as authorized, monetary or credit score recommendation; as an alternative, it’s for common informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or assets contained throughout the website don’t create an attorney-client or fiduciary relationship between the reader, consumer, or browser and web site proprietor, authors, reviewers, contributors, contributing corporations, or their respective brokers or employers.