{kind=link}

The data supplied on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation. See Lexington Regulation’s editorial disclosure for extra data.

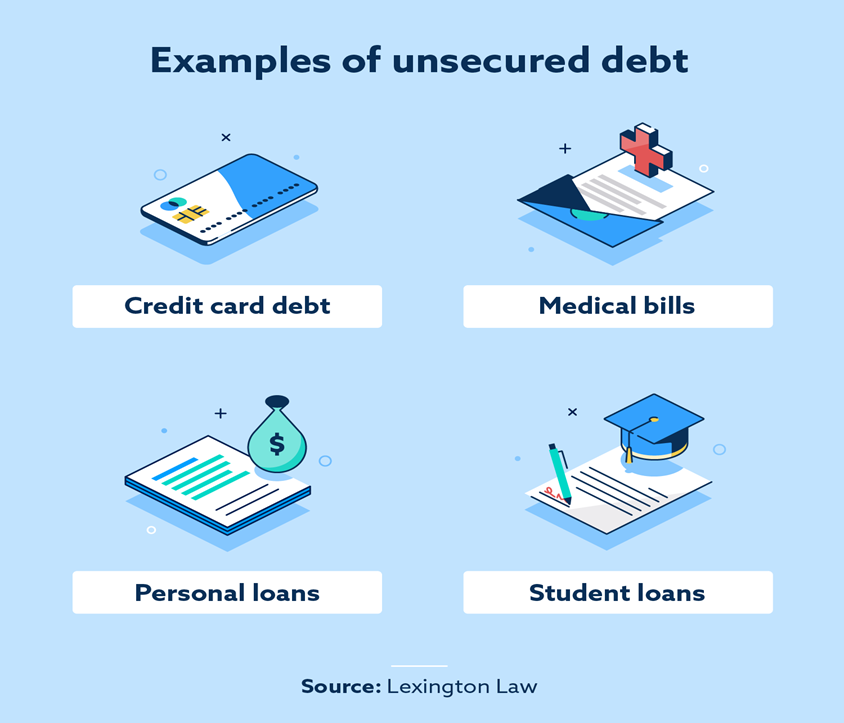

Unsecured money owed are loans or credit score strains with out collateral. This contains bank card debt, medical payments, private loans and pupil loans. Failure to pay unsecured debt can lead to assortment efforts and injury to credit score.

Are you overwhelmed by all of the totally different mortgage choices? Are you trying to find a sustainable debt answer? Relying in your monetary state of affairs, unsecured debt could be the proper possibility for you.

You can also make knowledgeable monetary judgments by understanding unsecured debt and its implications. This text will delve into the world of unsecured debt, clarify its definition and provides examples, discover the variations between secured and unsecured debt, make clear the affect of chapter and extra.

Let’s discover unsecured debt and the way it can affect your funds.

Key takeaways:

- Unsecured debt refers to loans or credit score strains with out collateral.

- Bank card debt, medical payments and private and pupil loans are widespread examples of unsecured debt.

- Failing to pay unsecured money owed can result in assortment efforts and harm your credit score.

- Prioritizing debt reimbursement is essential, and understanding the variations between secured and unsecured money owed may also help you make strategic choices.

What’s an unsecured debt?

Unsecured debt is a monetary obligation that doesn’t require collateral. Not like secured debt, backed by particular belongings, unsecured debt depends solely on the borrower’s creditworthiness and promise to repay. Examples of unsecured debt embody bank card debt, medical payments, private loans and pupil loans.

- Bank card debt: Once you make purchases utilizing a bank card, you accumulate unsecured bank card debt. The bank card firm extends you a line of credit score with out requiring collateral.

- Medical payments: Unexpected medical bills can lead to vital unsecured debt. These payments usually come up from medical procedures, therapies or hospital stays.

- Private loans: You may get hold of these from banks, credit score unions or on-line lenders. They’ve numerous functions, similar to debt consolidation, house enhancements and surprising bills.

- Scholar loans: Scholar loans are used to finance training bills. The federal government or non-public lenders provide them, they usually can have lengthy reimbursement phrases.

What occurs when you don’t pay an unsecured debt?

In the event you fail to pay your unsecured debt, there could also be vital penalties. Whereas particular actions might range relying on the creditor, listed here are some potential outcomes to watch out for:

- Assortment efforts: Collectors might make use of assortment companies or pursue authorized motion to get better the debt. These efforts can contain cellphone calls, letters and even lawsuits.

- Unfavorable affect on credit score: Unpaid unsecured debt can hurt your credit score. Late funds, defaults and charge-offs can contribute to a decrease credit score rating, making acquiring future credit score or loans tougher.

- Authorized proceedings: In excessive circumstances, collectors can file lawsuits to acquire a judgment in opposition to you. This can lead to wage garnishment or liens in your property.

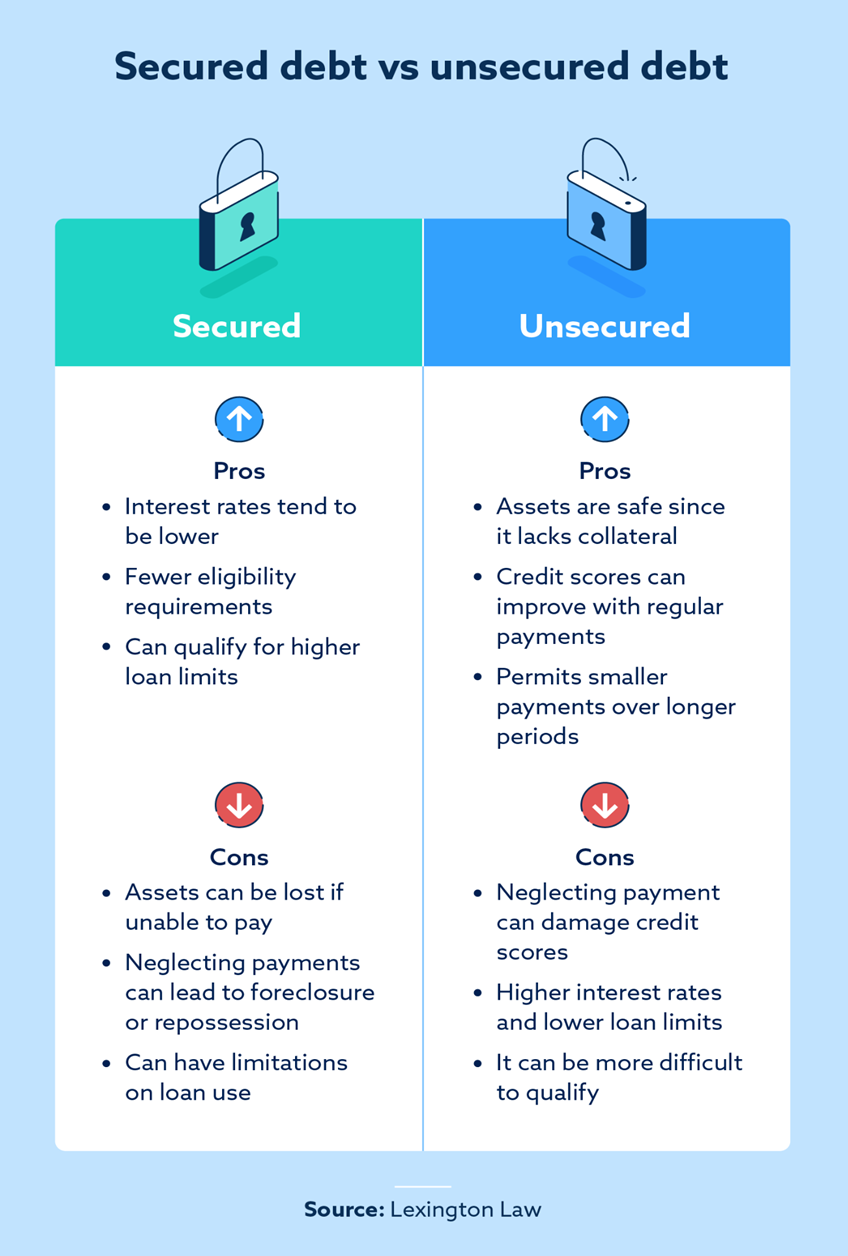

Secured debt vs. unsecured debt

Understanding the variations between secured and unsecured debt is essential for efficient monetary administration. Merely put, secured debt is backed by particular collateral, similar to a automotive or home, whereas unsecured debt lacks collateral. Within the occasion of default, secured collectors can seize the required belongings, whereas unsecured collectors wouldn’t have this feature.

Moreover, secured debtors normally want fewer eligibility necessities, their rates of interest could also be decrease they usually can qualify for increased mortgage limits since there may be much less danger from the lender’s standpoint. However there generally is a few disadvantages, like coping with foreclosures, repossession or shedding belongings if the borrower can not pay.

For unsecured debtors, the mortgage restrict is normally decrease, and rates of interest are typically increased. Nonetheless, there are just a few benefits of unsecured loans, like there is no such thing as a danger of shedding belongings, your credit score can enhance over time and you’ll arrange the mortgage to require smaller funds for a extra prolonged interval.

What occurs to secured and unsecured money owed throughout chapter?

Chapter impacts secured and unsecured money owed otherwise. In response to Chapter 7 of the United States Chapter Code, unsecured money owed are usually discharged, which means you now not must repay them. Nevertheless, secured money owed might require surrendering the collateral or restructuring the debt by means of a reaffirmation settlement.

In Chapter 13 chapter, usually referred to as “reorganization chapter,” you create a reimbursement plan to progressively repay your money owed over a particular interval, normally three to 5 years. Each secured and unsecured money owed are included on this plan, with precedence given to secured money owed.

Do not forget that chapter legal guidelines and procedures can range by nation, and the chapter designations talked about above particularly apply to chapter filings in america. It’s at all times advisable to seek the advice of with a authorized skilled or guide educated concerning the chapter legal guidelines in your particular jurisdiction.

Is secured or unsecured debt higher?

Whether or not secured or unsecured debt is best for you is dependent upon various factors, together with your monetary state of affairs and credit score, what you may or can not danger and your targets. It’s typically advisable to prioritize secured money owed because of the potential collateral loss. Falling behind on mortgage or automotive mortgage funds can result in foreclosures or repossession. Nevertheless, neglecting unsecured money owed can nonetheless have vital penalties, together with injury to credit score scores and assortment efforts.

It’s also vital to see it from the lender’s perspective—secured debt tends to be higher for them since it’s much less dangerous. Lenders can at all times declare the collateral to allow them to regain the misplaced funds. This makes secured debt riskier for debtors since they’ll lose their belongings if funds are unattainable.

Unsecured debt FAQ

As you proceed to discover the world of unsecured debt, we need to deal with some incessantly requested questions.

What’s an instance of unsecured debt?

An instance of an unsecured debt is bank card debt. Once you make purchases utilizing a bank card, you incur an unsecured debt with the cardboard issuer with out requiring collateral.

What are two sorts of unsecured debt?

Two different sorts of unsecured debt are private loans and medical payments. Private loans are funds you borrow from a lender with out collateral, whereas medical payments accumulate if you obtain healthcare providers and don’t require collateral.

What’s an unsecured debt referred to as?

Unsecured debt is often known as private debt. It’s a monetary obligation that’s not tied to particular belongings.

What occurs if an unsecured debt is just not paid?

In the event you don’t pay an unsecured debt, the creditor might make use of assortment efforts or pursue authorized motion to get better the debt, and your credit score will doubtless take a success.

Can unsecured money owed hurt your credit score?

Defaults, assortment actions and late or unpaid funds can hurt unsecured debtors’ credit score scores. Prioritizing well timed debt reimbursement is essential to sustaining wholesome credit score. Then again, your credit standing can enhance when you pay on time commonly since that reveals your dedication.

In conclusion, understanding unsecured debt is important for making knowledgeable monetary choices. By greedy the idea, differentiating it from secured debt and recognizing its implications, you may strategize debt reimbursement and shield your credit score.

Unsecured money owed and credit score restore

In the event you’re involved about your credit score, see if the group at Lexington Regulation Agency may also help. Empower your self with the data to make knowledgeable choices and work in your credit score with our providers. Attain out to Lexington Regulation at this time to get a free credit score evaluation and study extra about how we might assist.

Notice: Articles have solely been reviewed by the indicated legal professional, not written by them. The data supplied on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation; as a substitute, it’s for basic informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or sources contained throughout the website don’t create an attorney-client or fiduciary relationship between the reader, consumer, or browser and web site proprietor, authors, reviewers, contributors, contributing corporations, or their respective brokers or employers.