{kind=link}

The knowledge offered on this web site doesn’t, and isn’t meant to, act as authorized, monetary or credit score recommendation. See Lexington Legislation’s editorial disclosure for extra data.

The 28/36 rule is a monetary rule of thumb that measures a borrower’s means to repay their mortgage by evaluating their monetary well being.

Round 27 p.c of householders in the USA who maintain mortgages are grappling with housing price burdens. How ought to householders higher put together themselves for dealing with a house mortgage earlier than accruing an excessive amount of debt?

Attaining a safe and balanced monetary life includes navigating via steered tips and finest practices. Amongst these is the 28/36 rule—a framework for monetary decision-making.

On this article, we’ll break down what the 28/36 rule entails and the way it can function a priceless software for householders seeking to price range extra successfully.

Desk of contents:

- What’s the 28/36 rule?

- Entrance-end ratio: the 28 p.c

- Again-end ratio: the 36 p.c

- How does the 28/36 rule have an effect on my means to get a mortgage?

- Exceptions and particular concerns

- 28/36 rule FAQ

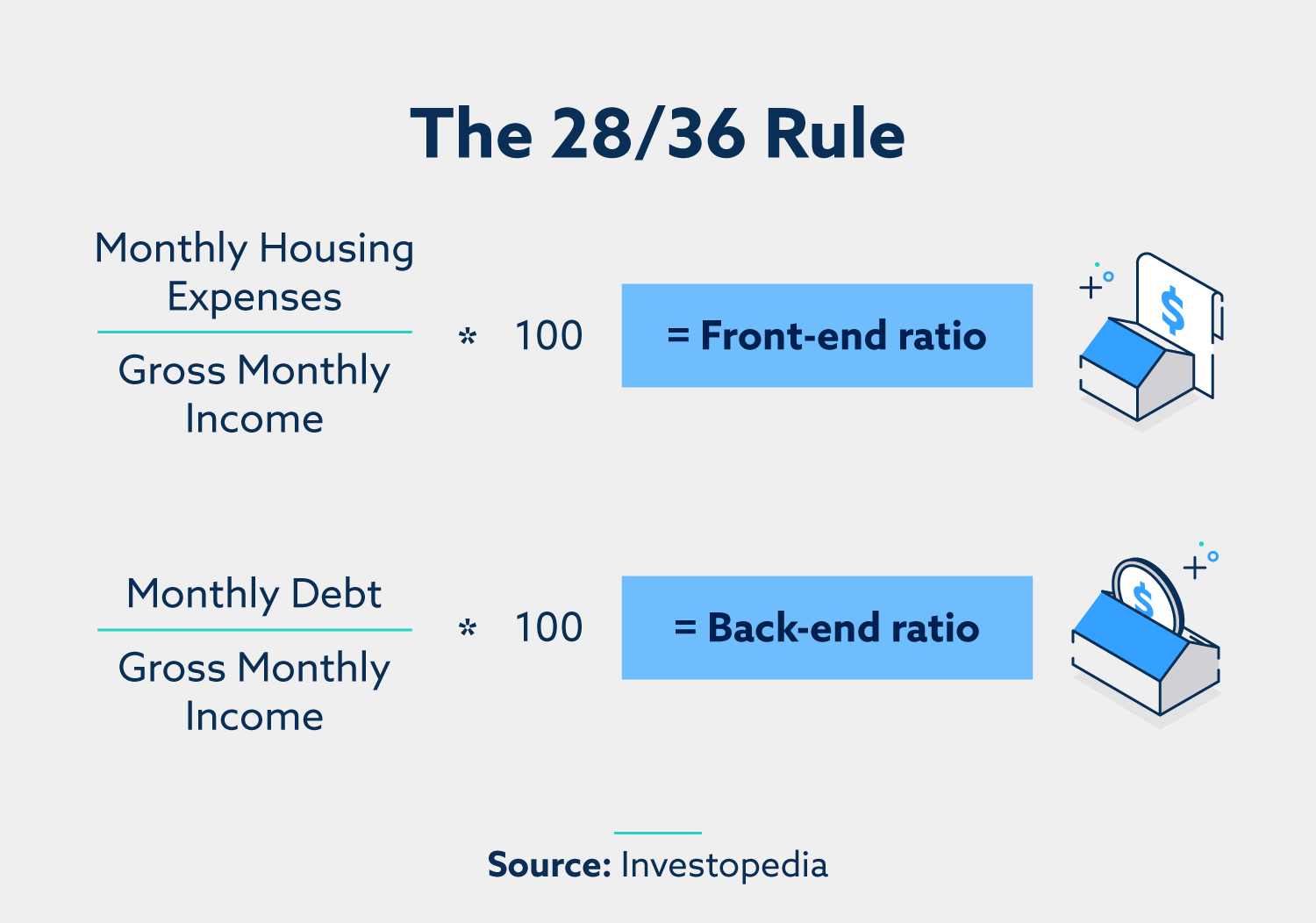

What’s the 28/36 rule?

The 28/36 rule is a monetary rule of thumb that measures a borrower’s means to repay their mortgage by evaluating their monetary well being.

The rule advises households to restrict their spending on housing bills to beneath 28 p.c of their gross month-to-month revenue and their spending on all debt to beneath 36 p.c of their gross month-to-month revenue.

This suggestion is especially essential for households planning to tackle a mortgage, as lenders use it to determine if they’ll lengthen credit score to debtors.

Entrance-end ratio: the 28 p.c

The front-end ratio, or the housing expense ratio, is a ratio that describes how a lot of 1’s revenue goes towards housing funds. It’s calculated by dividing housing bills by gross revenue and will make up beneath 28 p.c of whole month-to-month revenue, in response to the 28/36 rule.

Chances are you’ll be questioning what constitutes a housing fee. The next record particulars every thing included on this class:

- Mortgage funds: This constitutes each how a lot cash you borrow (principal) and the curiosity you pay on that borrowed cash.

- Property taxes: It’s essential to concentrate on how excessive your space’s property taxes are, as they will differ drastically from locale to locale.

- Insurance coverage: This consists of each householders insurance coverage and any added insurance coverage on your own home (twister, earthquake, flood, and many others.).

- HOA dues: House owner’s associations cost month-to-month dues. If you happen to stay beneath an HOA’s jurisdiction, remember to add them to the equation.

You may need seen that utility payments, web and cable TV providers will not be listed. Though they’re usually grouped beneath the umbrella time period of “housing bills,” they aren’t a part of the calculation that lenders make to find out your monetary well being.

To higher visualize the front-end ratio, think about you may have a gross month-to-month revenue of $4,500 per thirty days ($54,000 yearly). Each month, your mortgage funds come out to $1,250, your property taxes are $200, and your home-owner’s insurance coverage prices $100. You don’t stay in a neighborhood with a householders affiliation, so there aren’t any HOA dues.

Added collectively, your housing funds come out to $1,550. Divide that by your month-to-month revenue ($4,500), and you’ve got a front-end ratio of 0.34, or 34 p.c. As a result of it’s greater than 28 p.c, this could signify that you must pursue further revenue, transfer someplace that’s cheaper to stay or each to have an opportunity at an honest mortgage.

Again-end ratio: the 36 p.c

The back-end ratio, represented by the “36” within the 28/36 rule, is the ratio measuring how a lot of 1’s revenue is used to repay debt each month. This encompasses mortgage funds, pupil loans, automobile loans, bank card debt and all debt in between.

It’s calculated by dividing the quantity of month-to-month debt owed by gross month-to-month revenue.

Since baby help and alimony funds are additionally included, it’s essential to take a complete take a look at all your bills on this class to make sure you fall under the 36-percent threshold earlier than taking over any further debt.

Think about you may have a gross month-to-month revenue of $3,500 per thirty days ($42,000 yearly). You haven’t accrued bank card debt, however your automobile mortgage and pupil mortgage funds come out to a month-to-month whole of $600. Divide your whole debt ($600) by your month-to-month revenue ($3,500), and your back-end ratio totals 0.17, or 17 p.c.

How does the 28/36 rule have an effect on my means to get a mortgage?

If taking out a mortgage would trigger your front-end ratio to go above 28 p.c, or your back-end ratio to go above 36 p.c, then it can most likely be tough to get the excessive mortgage mortgage and low APR you have been hoping for. You should still qualify for a mortgage, however the lender will doubtless flip down your preliminary request and provide a smaller quantity.

The 28/36 rule is only one of many elements that go into figuring out your means to get a perfect mortgage. These elements decide the dimensions of your mortgage, and thus what proportion of revenue ought to go to mortgage funds. They embrace:

- Credit score rating. Your credit score rating has a main impression in your mortgage fee. Lenders rely closely on debtors’ credit score scores to find out their threat every time contemplating whether or not to lend cash. This holds very true for a really massive buy like a house.

- Revenue. Whether or not you intend to tackle a brand new mortgage or refinance a present mortgage, your revenue has an impression in your lender’s willingness to assist out. The next revenue communicates a greater means to repay a mortgage, so we suggest pursuing a aspect revenue in case your revenue received’t impress lenders because it stands.

- Dimension of down fee. Just like revenue, bigger down funds on a home (20 p.c and better) ship a constructive message to lenders by positively impacting each your front- and back-end ratios. It’s value taking further time to save lots of as much as make a bigger down fee.

Exceptions and particular concerns

Whereas the 28/36 rule tends to be the gold commonplace for profitable lenders’ belief, this rule primarily applies to typical mortgages. If attaining these ratios doesn’t really feel reasonable for the time being however you’re critical about shopping for a house quickly, you need to be conscious of different kinds of mortgage loans which are an exception to the rule.

Other than having wonderful credit score and making a bigger down fee, chances are you’ll qualify for a government-insured mortgage. For instance, the Federal Housing Administration (FHA), the U.S. Division of Veterans Affairs (VA) and the U.S. Division of Agriculture (USDA) all provide mortgages that enable for approval at increased front- and back-end ratios. If your property is vitality environment friendly, it could additional enhance your ratio’s threshold.

| Kind of mortgage | Entrance-end ratio | Again-end ratio |

|---|---|---|

| Typical | 28% | 36% |

| FHA | 31% | 43% |

| FHA (Vitality-efficient residence) | 33% | 45% |

| VA | N/A | 41% |

| USDA | 29% | 41% |

28/36 Rule FAQ

Under are generally requested questions concerning the 28/36 rule and funds.

What occurs for those who exceed the 28/36 rule?

If you happen to discover that you simply’re placing more cash towards paying again debt and exceeding the 36 p.c rule, you’ll want to scale back your debt earlier than making use of for a mortgage.

We suggest that you simply:

- Assess your monetary state of affairs: Decide your sources of revenue and money owed.

- Create a price range: Develop a price range along with your month-to-month gross revenue and bills. Embody your requirements, like groceries and utilities, in addition to optionally available bills, like consuming out or going to the films.

- Determine pointless bills: Consider your optionally available bills and determine which ones you possibly can realistically in the reduction of on.

- Prioritize your money owed: Begin paying your smallest debt stability first and work your means up, or begin along with your largest stability and work downward. Add this to your month-to-month price range plan.

Keep away from allocating any new debt whilst you give attention to paying off your present debt. That means, you possibly can keep targeted on assembly the 28/36 rule and constructing a greater monetary portfolio for residence shopping for.

What’s included in housing bills?

Housing bills embrace all prices related to renting or proudly owning a house. Housing bills differ for those who hire or personal the house, however these are the commonest for householders:

- Month-to-month mortgage fee

- Mortgage insurance coverage premium (MIP)

- Property taxes

- Owners affiliation (HOA) charges

- Dwelling upkeep and repairs

- Owners insurance coverage

As a substitute of mortgages, renters can embrace hire funds, renters insurance coverage and utilities as a few of their housing bills.

What’s gross revenue?

Gross revenue is the entire revenue you earn earlier than deductions and taxes are taken out. After deductions are taken out, the result’s thought-about your “internet revenue.” That is the quantity you are taking residence to repay bills and debt.

Your whole debt from all loans mustn’t exceed what proportion of your gross month-to-month wage?

Your whole debt from all of your loans mustn’t exceed the 28/36 rule. Exceeding the rule places you at the next threat and will sway your lender to not approve you for a house mortgage.

Along with various mortgage choices, it’s essential to think about what sort of mortgage you need to pursue, whether or not it’s a residence fairness mortgage or a line of credit score. The way you’re going to purchase a house is likely one of the most vital life selections to make. As such, it’s essential that you simply do your due diligence and suppose forward. From enhancing your credit score with the assistance of a credit score monitoring service to paying off debt, there are all kinds of how to observe good private finance with a purpose to doubtlessly qualify for the mortgage you need.

Be aware: Articles have solely been reviewed by the indicated legal professional, not written by them. The knowledge offered on this web site doesn’t, and isn’t meant to, act as authorized, monetary or credit score recommendation; as an alternative, it’s for normal informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or assets contained inside the web site don’t create an attorney-client or fiduciary relationship between the reader, person, or browser and web site proprietor, authors, reviewers, contributors, contributing corporations, or their respective brokers or employers.