{kind=link}

The knowledge supplied on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation. See Lexington Regulation’s editorial disclosure for extra data.

There are not less than 16 distinct variations of FICO scores at the moment in use, with new ones probably developed to cater to the precise wants of various industries and customers.

FICO scores are a vital factor in understanding your credit score well being and dealing in the direction of enchancment. They take into account a number of components in your credit score report, like fee historical past, credit score utilization ratio and size of credit score historical past. They play a serious function in figuring out your mortgage approval odds and rates of interest.

Nonetheless, in contrast to a single credit score report, there isn’t only one common FICO rating. FICO provides a vary of scores, sometimes falling between 300 and 850, tailor-made to particular bank card varieties, mortgage purposes and industries. Understanding the several types of FICO scores and what they symbolize empowers you to handle your credit score successfully and obtain your monetary objectives. Under, we’ll discover the several types of FICO scores and what they imply for you.

Desk of contents:

What number of kinds of FICO scores are there?

FICO provides a variety of scores, with experiences of not less than 16 distinct variations at the moment in use. These variations cater to particular credit score wants like mortgages, auto loans or bank cards. It’s essential to notice that regardless that there are a number of FICO scores, credit score scores usually play a serious function in figuring out your mortgage approval odds and rates of interest.

Whilst you have one credit score historical past, the story behind your credit score rating can fluctuate barely relying on the credit score bureau. It’s because Experian®, TransUnion®

and Equifax® won’t obtain the identical data from all collectors. Because of this, every bureau would possibly generate a barely totally different FICO rating for you.

FICO scores 8 and 9

FICO Scores 8 and 9, developed in 2009 and 2017, are the 2 most generally used variations. These scores present a extra subtle evaluation of your creditworthiness in comparison with earlier fashions. Whereas each take into account components like fee historical past, credit score utilization and credit score historical past size, FICO Rating 9 provides current credit score exercise barely extra weight.

They’re the go-to alternative for lenders throughout numerous mortgage varieties, together with mortgages, auto loans and private loans. A robust exhibiting in both FICO Rating 8 or 9 considerably boosts your possibilities of mortgage approval and probably unlocks extra favorable rates of interest.

FICO rating classes by {industry}

Past the bottom FICO scores, there are additionally industry-specific variations tailor-made to evaluate creditworthiness inside a selected sector. Business-specific examples embody:

- FICO scores for auto lending: FICO auto scores place better emphasis in your historical past of constructing automobile funds on time and managing mortgage balances. They’re much less involved together with your general bank card utilization in comparison with your base FICO rating.

- FICO scores for mortgage lending: FICO mortgage scores delve deeper into your long-term monetary stability. Components like your employment historical past and housing stability carry extra weight than a base FICO rating.

- FICO scores for bank card lending: FICO bankcard scores focus closely in your revolving credit score historical past. They weigh your bank card balances and fee conduct on current playing cards extra closely than a base FICO rating.

Take into accout: New FICO rating variations are launched periodically, so that you would possibly encounter industry-specific scores tailor-made to different lending sectors.

| Experian | Equifax | TransUnion | |

|---|---|---|---|

| Scores most generally used | FICO® Rating 9, FICO® Rating 8 | FICO® Rating 9, FICO® Rating 8 | FICO® Rating 9, FICO® Rating 8 |

| Scores used for auto lending | FICO® Auto Rating 9, FICO® Auto Rating 8, FICO® Auto Rating 2 | FICO® Auto Rating 9, FICO® Auto Rating 8, FICO® Auto Rating 5 | FICO® Auto Rating 9, FICO® Auto Rating 8, FICO® Auto Rating 4 |

| Scores used for mortgage lending | FICO® Rating 2 | FICO® Rating 5 | FICO® Rating 4 |

| Scores used for bank card lending | FICO® Bankcard Rating 9, FICO® Bankcard Rating 8, FICO® Bankcard Rating 2, FICO® Rating 9, FICO® Rating 3 | FICO® Bankcard Rating 9, FICO® Bankcard Rating 8, FICO® Bankcard Rating 5, FICO® Rating 9 | FICO® Bankcard Rating 9, FICO® Bankcard Rating 8, FICO® Bankcard Rating 4, FICO® Rating 9 |

| Newly launched scores | FICO® Rating 10, FICO® Auto Rating 10, FICO® Bankcard Rating 10 FICO® Rating 10T | FICO® Rating 10, FICO® Auto Rating 10, FICO® Bankcard Rating 10 FICO® Rating 10T | FICO® Rating 10, FICO® Auto Rating 10, FICO® Bankcard Rating 10 FICO® Rating 10T |

Why are there numerous FICO rating variations?

Whereas a single FICO rating might sound perfect, the fact is that totally different credit score wants require a extra nuanced strategy. Right here’s why we’ve got numerous FICO rating variations:

Evolving know-how

The best way we use credit score is continually evolving. This evolution occurs by means of periodic updates that incorporate new analytical instruments for improved danger prediction. These updates end in new FICO rating variations being launched. Lenders can select whether or not they’ll undertake the newest model or persist with their present one.

Business specificity

Not all loans are created equal, and neither are FICO scores. For instance, a FICO auto rating prioritizes your automobile fee historical past, whereas a FICO mortgage rating focuses on long-term stability, like employment historical past. These industry-specific scores give lenders a extra clear image of your skill to repay the precise mortgage you’re making use of for.

How are FICO scores calculated?

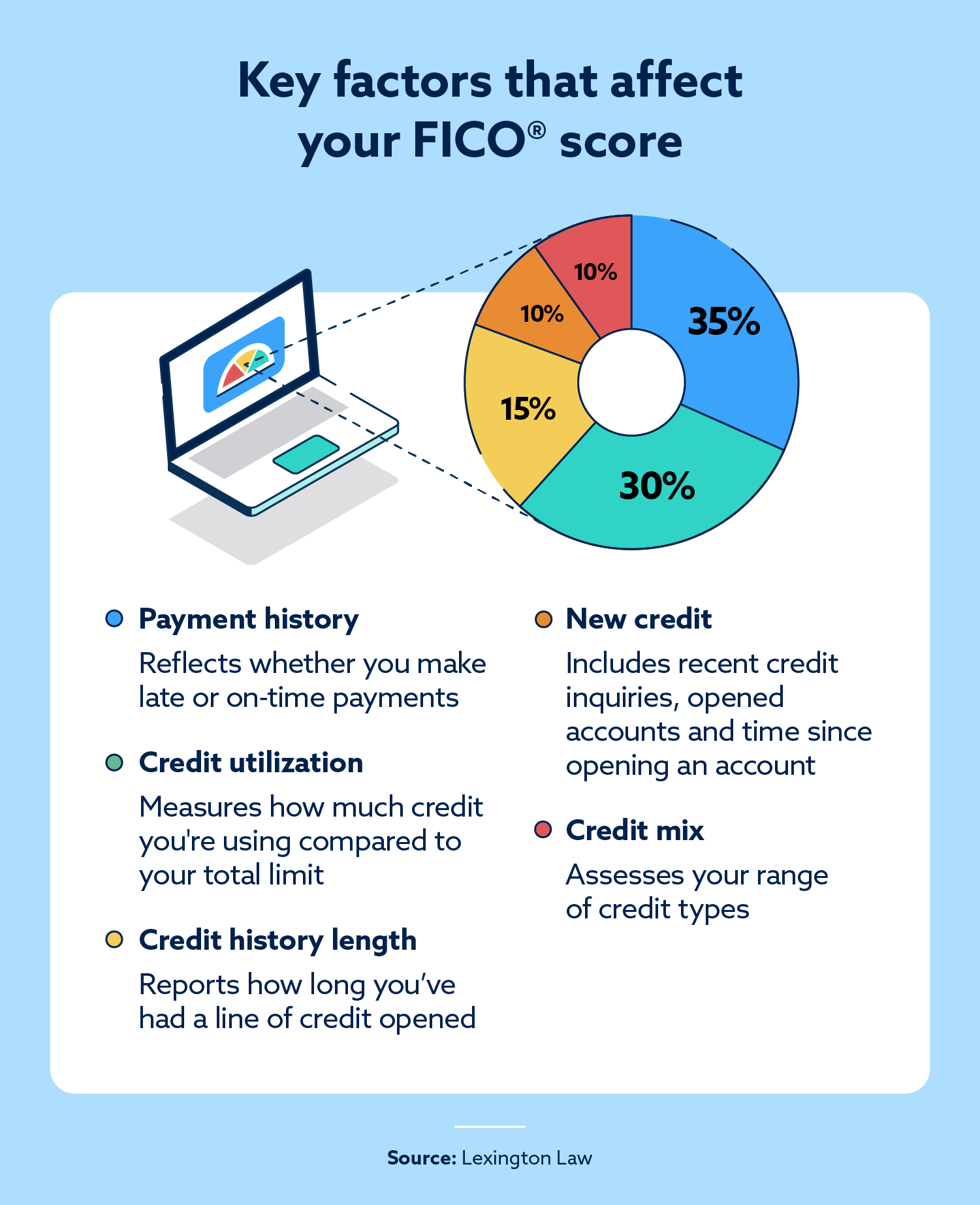

These scores are derived from data in your credit score experiences maintained by the three main bureaus: Experian, TransUnion and Equifax. Whereas particular weightings fluctuate between FICO variations, all scores depend on 5 key components out of your credit score historical past. Under is a breakdown of the components thought of in a single common mannequin, FICO Rating 9 and their approximate weightings:

- Cost historical past (35 %): That is probably the most essential issue. It displays your monitor file of constructing well timed funds for bank cards, loans and different obligations. Late funds or delinquencies can considerably decrease your rating.

- Credit score utilization (30 %): This refers back to the quantity of credit score you’re utilizing in comparison with your complete credit score restrict. You must ideally hold your utilization beneath 30 %.

- Credit score historical past size (15 %): An extended credit score historical past with accountable administration usually interprets to a better rating.

- New credit score (10 %): Making use of for a number of traces of credit score in a brief interval can briefly decrease your rating.

- Credit score combine (10 %): Having a wholesome mixture of credit score varieties, akin to bank cards and installment loans, can positively impression your rating.

By monitoring your credit score experiences and specializing in these key areas, you possibly can work towards a sturdy credit score rating, make knowledgeable choices to enhance your FICO rating and obtain your monetary objectives.

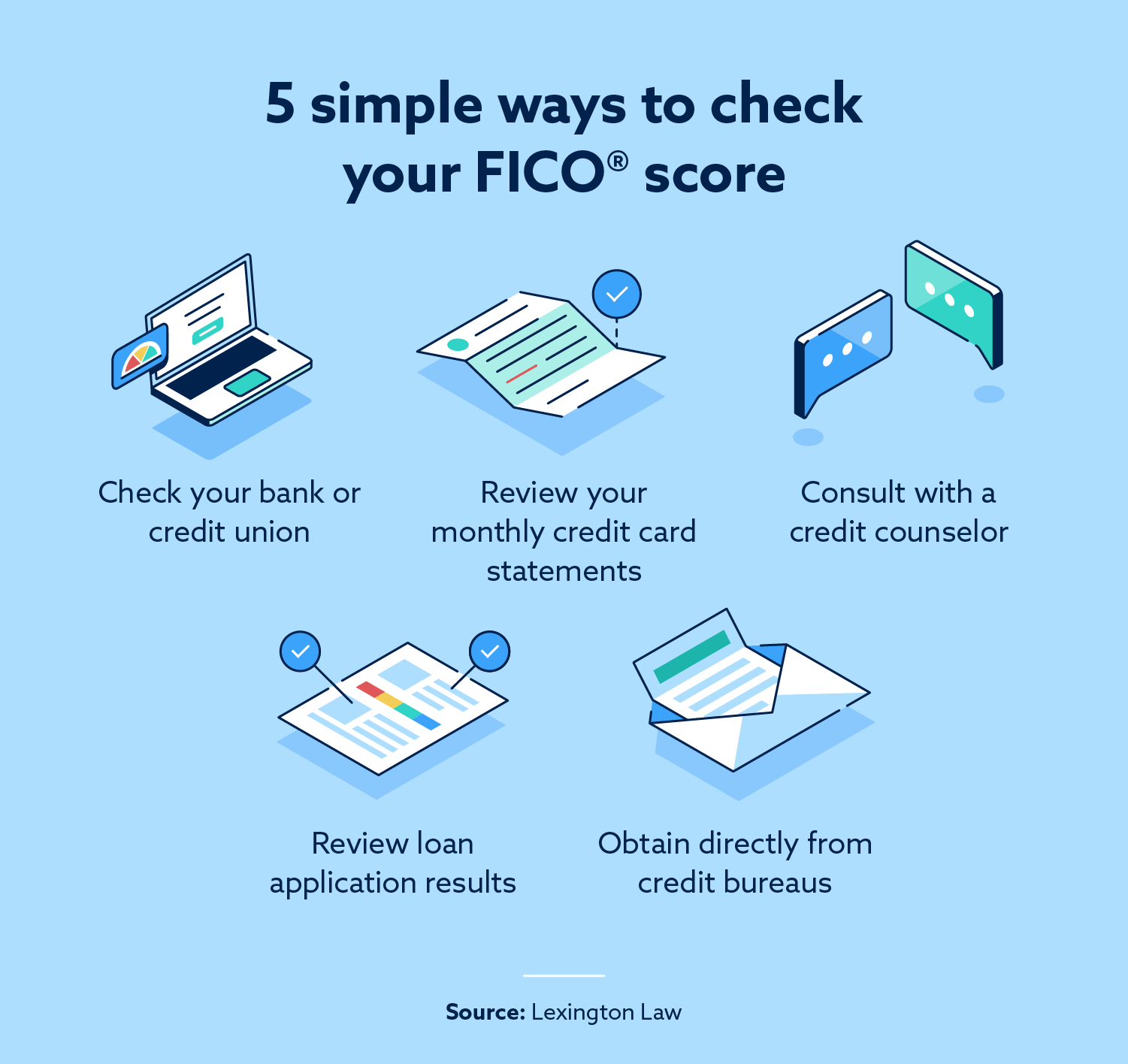

How one can test your FICO rating

Realizing your FICO rating is essential for taking cost of your monetary well being. Listed below are some methods to entry your rating:

- Examine your financial institution or credit score union: Look on-line or inside your cellular banking app to see if this selection is out there.

- Evaluation your month-to-month bank card statements: Some bank card issuers embody your FICO rating or a variation, akin to Vantage Rating, in your month-to-month statements. Evaluation the main points to know any related charges.

- Seek the advice of with a credit score counselor: Non-profit credit score counseling businesses can present steering in your credit score report and should provide entry to your FICO rating as a part of their companies.

- Evaluation mortgage software outcomes: When making use of for sure loans, lenders could present your FICO rating as a part of the appliance course of.

- Get hold of your rating immediately from credit score bureaus: You may entry a free credit score report from every of the three main bureaus (Experian, TransUnion and Equifax) yearly at Annual Credit score Report.

Vital observe: Whereas some companies would possibly promote a “free” FICO rating, be cautious of any hidden charges or recurring expenses related to signing up for extra options. It’s all the time greatest to learn the high quality print earlier than coming into any private data.

Which FICO rating must you test?

Since your credit score report data from all three main bureaus (Experian, TransUnion and Equifax) influences your FICO scores, you’ll need to test your credit score report from every bureau. Lenders have the pliability to make the most of any model they deem acceptable for the precise mortgage kind. This may make it difficult to pinpoint the precise rating a selected lender would possibly use.

Many bureaus provide a glimpse of the FICO scores related together with your credit score report, providing you with a common thought of the vary you would possibly fall inside. Whilst you won’t know the precise model a lender will use, specializing in enhancing your general credit score well being throughout all components will positively impression all of your FICO scores, in the end strengthening your scores.

How one can enhance your FICO rating

How do you attain for a honest credit score rating (sometimes 640 to 699) or climb even increased? Listed below are key methods you possibly can implement:

- Make funds on time: Delinquencies and late funds considerably decrease your rating. Give attention to making all of your bank card payments and mortgage funds on time, each time. Arrange computerized funds to keep away from missed due dates.

- Don’t shut outdated accounts abruptly: An extended credit score historical past usually interprets to a better rating. Don’t make the error of closing outdated bank card accounts as soon as they’re paid off. The size of your credit score historical past, with a constructive monitor file, is efficacious.

- Dispute errors in your credit score report: Evaluation your credit score experiences commonly and dispute any errors you discover. Inaccurate data can negatively impression your rating. The three main bureaus (Experian, TransUnion and Equifax) every have a web based dispute course of.

- Preserve balances low: Don’t max out your bank cards. Attempt to maintain your credit score utilization ratio low, ideally beneath 30 % of your credit score restrict. This demonstrates your skill to handle credit score responsibly.

Whereas outcomes could fluctuate relying in your credit score historical past, constantly following these steps may help elevate your rating.

Understanding your FICO rating is essential to make sure you’re on monitor for a wholesome monetary future. Join your free credit score evaluation and see the place you stand in your credit score journey.

Be aware: Articles have solely been reviewed by the indicated lawyer, not written by them. The knowledge supplied on this web site doesn’t, and isn’t supposed to, act as authorized, monetary or credit score recommendation; as an alternative, it’s for common informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or assets contained inside the website don’t create an attorney-client or fiduciary relationship between the reader, consumer, or browser and web site proprietor, authors, reviewers, contributors, contributing companies, or their respective brokers or employers.