{kind=link}

The knowledge offered on this web site doesn’t, and isn’t meant to, act as authorized, monetary or credit score recommendation. See Lexington Regulation’s editorial disclosure for extra info.

When you cease paying your bank card, you possibly can anticipate late charges, elevated rates of interest, and a considerably decreased credit score rating.

When you cease paying your bank card, you possibly can anticipate late charges, elevated rates of interest and a broken credit score rating. If sudden circumstances—comparable to unemployment or medical payments—go away you with extra debt than you possibly can afford to pay, it could be tough to remain on prime of bank card payments.

The results could appear small at first, however as extra time passes, the consequences of not paying your bank card turn out to be extra severe. Our information will cowl the most typical drawbacks for negligent card funds and share a few of Lexington Regulation Agency’s debt reduction options.

Key takeaways:

- Most bank cards supply a grace interval earlier than funds are thought of late.

- Fee historical past makes up 35 % of your FICO® credit score rating.

- Closing your oldest bank cards can harm your credit score.

Desk of contents:

Late charges and curiosity start to accrue

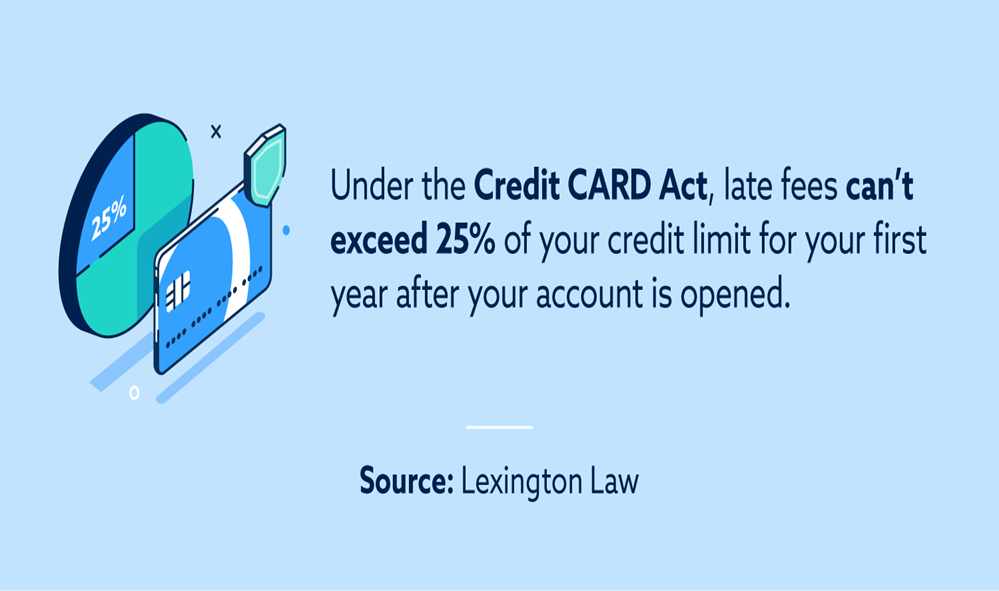

Late charges are capped at 25 % of your credit score restrict for the primary yr after you’ve opened an account. That is a part of your rights outlined within the Credit score Card Accountability Accountability and Disclosure Act of 2009 (often known as the Credit score CARD Act).

The price is added to your bank card steadiness and turns into topic to curiosity expenses based mostly in your APR, or annual proportion charge.

After two missed funds (60 days), your curiosity will usually enhance to the upper penalty APR outlined in your card’s phrases and circumstances settlement. The cardboard issuer could not decrease the rate of interest for six months.

Late charges and finance expenses will proceed to extend your month-to-month cost, making it tougher to catch up.

Collections efforts from collectors enhance

Your collectors will start to contact you to gather the cost you owe them. They may proceed to contact you usually and with growing frequency till the lacking cost is fulfilled.

Below the Honest Debt Assortment Practices Act, debt collectors should abide by debt assortment legal guidelines about communication with customers. For example, they don’t seem to be allowed to name at uncommon hours. Shoppers have the best to request the debt collector to cease contacting them. Nonetheless, these legal guidelines solely apply to debt collectors and never your unique collectors.

Credit score rating drops

When you miss a cost by 30 days, the creditor will report it to the three credit score bureaus: Equifax®, Experian® and TransUnion®. Since cost historical past determines 35 % of your FICO credit score rating, this implies your credit score rating will possible drop. If the account goes to collections, it is going to be thought of a severe delinquency.

A low credit score rating will make it tough to acquire a bank card, mortgage, or perhaps a job sooner or later. It is going to additionally lower your potential to get accredited for a lease or mortgage.

Account could go to collections

When you’ve reached 180 days late, the creditor will usually cost off the debt and promote it to a set company. The time period “charged off” doesn’t imply the debt will go away—not solely are you continue to accountable for the quantity owed, however extra charges and curiosity could also be added to your steadiness.

Cost-offs can stay in your credit score report for seven years. Nonetheless, the unique creditor or debt collector can sue you for the debt up till the statute of limitations expires.

When do the collectors report a cost missed or late?

FICO credit score scores think about the small print of a missed cost, comparable to how late it was. Collectors usually report late funds in set intervals:

- Late by 30 to 59 days

- Late by 60 to 89 days

- Late by 90 to 119 days

- Late by 120 to 149 days

- Late by 150 to 179 days

- Late by 180 or extra days

What occurs to bank card debt if I transfer in a foreign country?

Your collectors should still ship you to collections or file a lawsuit in opposition to you when you have debt after transferring overseas. Collectors can go after any belongings you allow behind in a checking, financial savings, or funding account. When you proceed working for an employer based mostly within the U.S., your wages could possibly be garnished.

When you transfer overseas, you’ll proceed to accrue penalties and vital injury to your credit score, which could possibly be problematic in case you ever resolve to return to the US.

Can I am going to jail for not paying my bank cards?

There isn’t a debtors’ jail in the US, but when a creditor sues you in a court docket of legislation and wins a judgment, they are able to garnish your wages or file a lien in your property.

Handle your credit score with Lexington Regulation Agency

One of the necessary elements figuring out your credit score is whether or not or not your funds have been made on time. Late or missed bank card funds can decrease your rating, stopping you from acquiring loans or bank cards with higher phrases and decrease rates of interest. When you discover an inaccurate late cost or one other error in your credit score report, our companies can probably enable you to deal with inaccurate destructive objects and work to enhance your credit score.

Word: Articles have solely been reviewed by the indicated lawyer, not written by them. The knowledge offered on this web site doesn’t, and isn’t meant to, act as authorized, monetary or credit score recommendation; as an alternative, it’s for normal informational functions solely. Use of, and entry to, this web site or any of the hyperlinks or assets contained inside the web site don’t create an attorney-client or fiduciary relationship between the reader, consumer, or browser and web site proprietor, authors, reviewers, contributors, contributing companies, or their respective brokers or employers.