{kind=link}

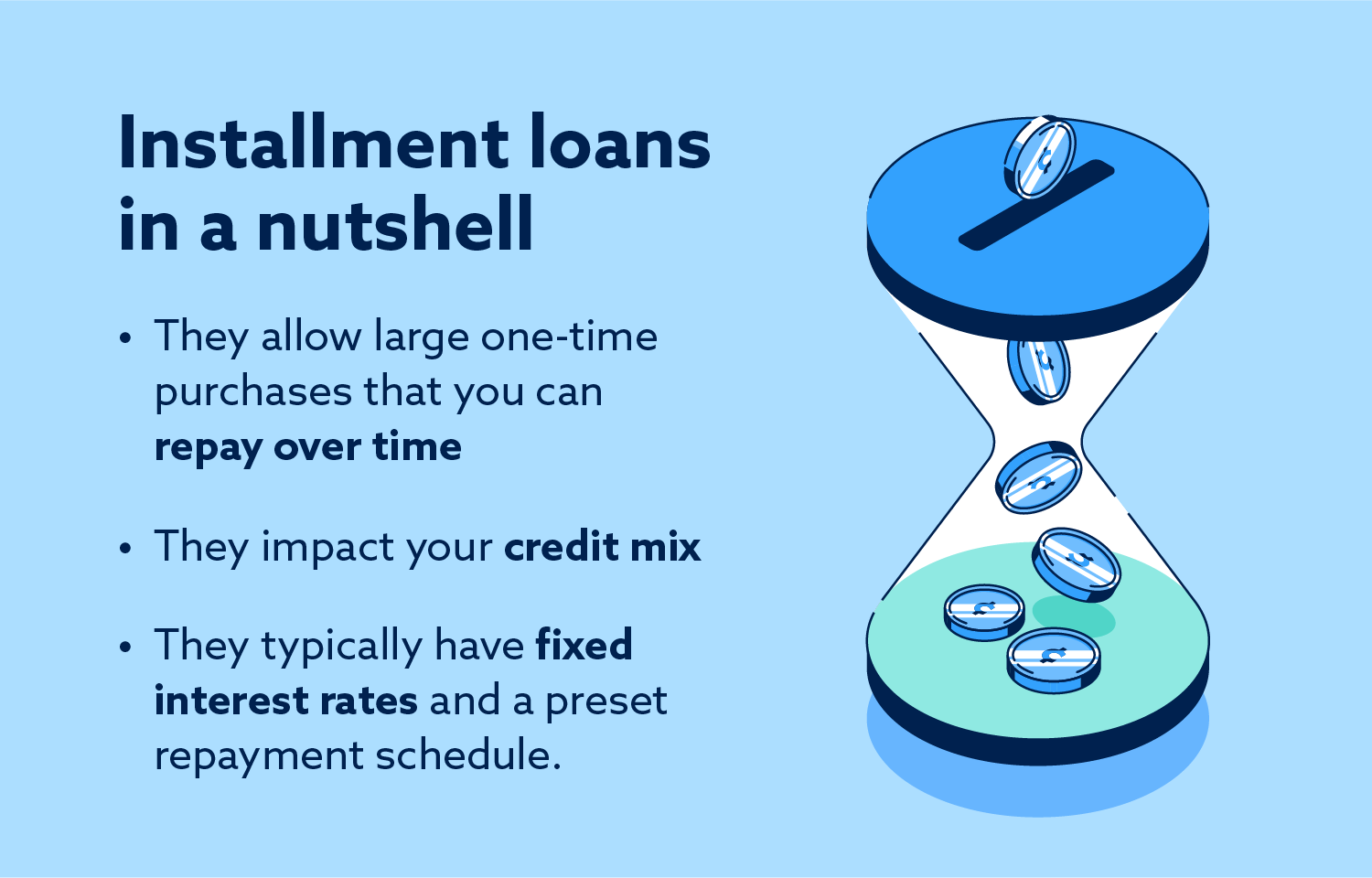

An installment mortgage consists of a lump sum of cash you repay over time. Auto loans, private loans and mortgages are widespread examples of installment loans.

The time period installment mortgage, generally known as “installment credit score,” refers to a monetary settlement whereby a lender provides you a lump sum of cash you’ll need to repay over time. Folks have a tendency to hunt installment loans for giant purchases like a brand new automobile or financing for a house. Successfully repaying your mortgage in full and on time can elevate your credit score rating.

We’ll totally talk about installment loans on this information, weigh their execs and cons and enable you determine if this funding is best for you.

How do installment loans work?

An individual can purchase an installment mortgage by making use of with a monetary establishment comparable to a financial institution or credit score union. Every lender has distinct standards they’d like candidates to satisfy and particular mortgage phrases.

On common, installment loans can provide debtors wherever from $1,000 to $100,000 and sometimes have reimbursement durations that vary from one to 30 years.

For those who’re accredited for an installment mortgage, the lender will offer you the funds to make use of for whichever objective is printed in your mortgage settlement. Then, you’ll be anticipated to repay the cash you borrowed in weekly or month-to-month installments — plus any curiosity generated by your mortgage’s annual share charge (APR).

Rates of interest play a considerable function in your mortgage reimbursement plan. If you carry a steadiness on a mortgage, your APR might be factored in to find out how a lot curiosity you’ll be chargeable for. When you have a six p.c rate of interest and you’ve got a steadiness of $100 due, you’ll find yourself paying 50 cents in curiosity. The decrease your remaining steadiness is, the much less curiosity you’ll pay for the rest of your mortgage.

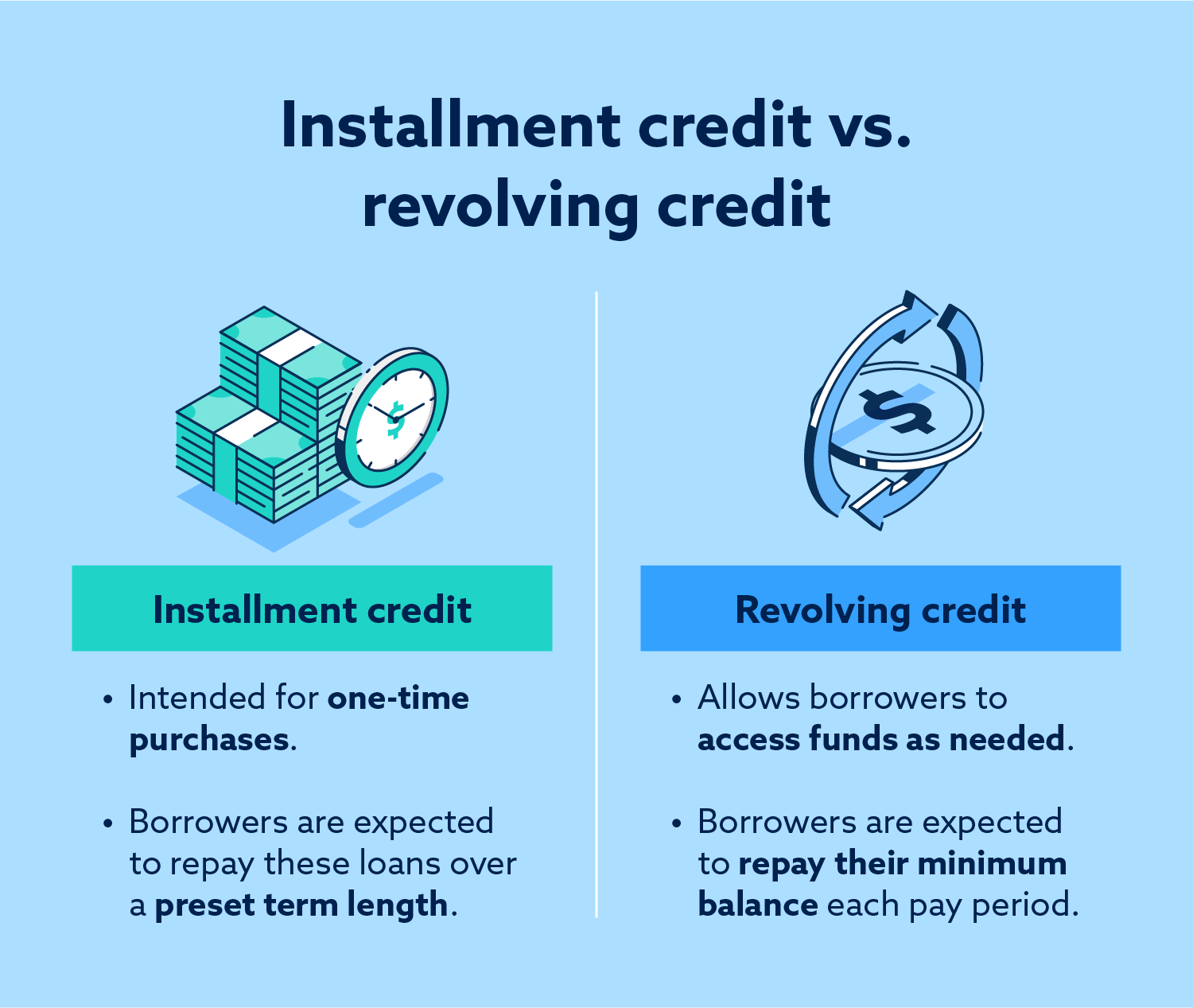

Installment loans differ from revolving credit score (like a bank card) by way of use. With an installment mortgage, you borrow cash for a selected buy after which pay it off for good. With revolving credit score, you repeatedly borrow and repay funds for numerous purchases in perpetuity.

Do installment loans have an effect on your credit score rating?

Installment loans affect your rating in a number of methods. If you first apply for funds, lenders will overview your credit score report. This counts as a arduous inquiry to the main credit score bureaus and will briefly decrease your rating.

The way you handle your mortgage repayments may also have an effect on your rating for higher or worse; persistently paying your minimal steadiness for every billing cycle can considerably improve your credit score rating by demonstrating monetary accountability and vice versa.

Managing an installment mortgage additionally contributes to your credit score combine — an element that may doubtlessly increase your credit score rating primarily based in your present variety of open accounts.

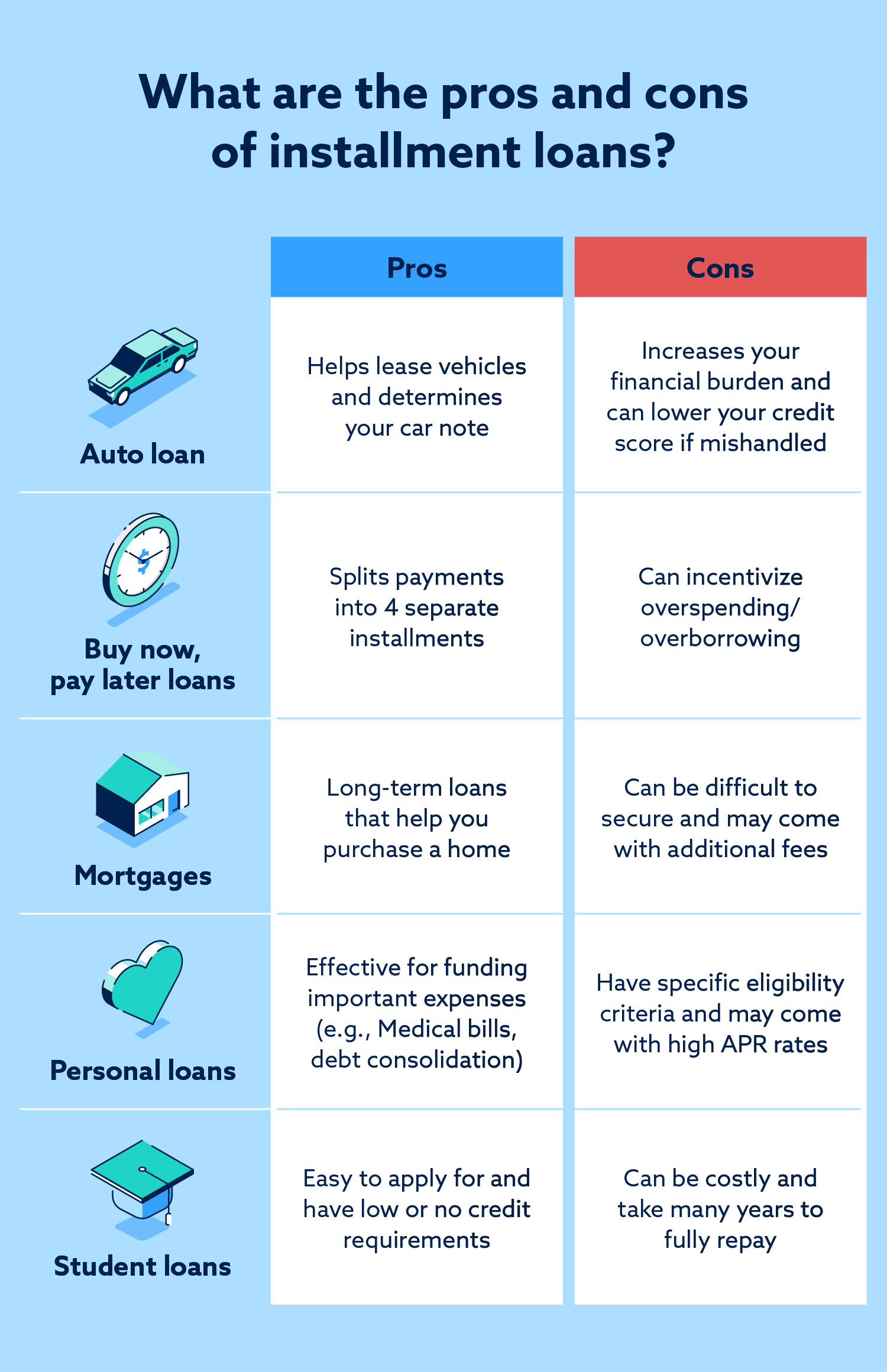

5 varieties of installment loans

A wide range of installment loans can be found for eligible debtors. Beneath are 5 examples of among the commonest loans you’ll encounter.

Auto Loans

Auto loans assist debtors receive autos with relative ease and progressively repay what they owe over a number of years. An individual’s month-to-month automobile be aware is basically decided by auto mortgage charges, APR and their down fee quantity. Auto loans for bad credit report debtors may provide smaller quantities or have stricter reimbursement phrases.

- Primary benefit: Assist debtors lease or finance autos.

- Primary drawback: Good credit score or extra is required for one of the best auto charges.

Purchase Now, Pay Later Loans

When buying on-line, you could possibly apply for a purchase now, pay later mortgage. These funding choices allow you to cut up a purchase order into installments and unfold throughout a number of weeks or months. These loans usually cowl purchases between $50 to $1,500.

- Primary benefit: Splits eligible purchases into installment funds.

- Primary drawback: It’s straightforward for individuals to borrow greater than they will afford.

Mortgages

Mortgages are among the largest and longest-lasting installment loans an individual can apply for. Banks sometimes provide mortgages with 30-year phrases, although this could fluctuate relying on issues just like the economic system and a borrower’s credit score profile.

- Primary benefit: This may also help you buy a house which you could finally personal.

- Primary drawback: Mortgages are arduous to acquire and may be costly in the long run.

Private Loans

Private installment loans can are available a number of types, together with debt consolidation, medical loans and joint loans.

- Primary benefit: Lump sum funding that may have versatile makes use of.

- Primary drawback: Usually comes with excessive rates of interest and extra charges.

Pupil Loans

These are among the first installment loans that individuals may be eligible for as a result of they’ve extra open-ended eligibility necessities. Authorities establishments and banks are often keen to supply these loans to college students with little or no credit score historical past. They could even defer reimbursement till after commencement.

- Primary benefit: Low or no credit score rating necessities for college students, eligible for debt forgiveness and deferment plans.

- Primary drawback: Include mortgage caps and might take 10 to 30 years or extra to repay.

Ought to I exploit an Installment Mortgage?

Installment loans are useful for making vital purchases, although one can doubtlessly overborrow in the event that they take out too many loans and not using a stable reimbursement plan set. You must use installment loans if you happen to consider you’ll be able to reliably make your minimal fee quantities every interval.

In case your monetary scenario adjustments, it’s vital to inform your lender as quickly as attainable. Writing a goodwill letter that precisely explains your circumstances can pave the best way for leniency and provide you with extra time to marshal your funds.

How understanding your credit score rating may also help you get a mortgage

Folks can use installment loans to assist make main purchases and enhance their credit score, as long as they’ve a plan to repay what they owe. Realizing your credit score profile can provide you a greater sense of the loans you’re at the moment eligible for. Get a free credit score evaluation from Lexington Regulation Agency at present.