{kind=link}

Selecting the flawed reimbursement plan may price you tens of 1000’s of {dollars} — or add years to your reimbursement timeline.

That’s not a scare tactic. It’s simply the truth of how completely different IBR and RAP truly are. For some debtors, IBR would be the clear winner. For others, RAP will lower their month-to-month fee considerably. The issue is that no person goes to inform you which one is best for you.

That’s what this information is for.

Fast Reply: IBR vs. RAP

Unsure which plan suits you? Right here’s the brief model. The detailed breakdown follows.

| Your Scenario | Higher Plan |

| Excessive revenue (sometimes $80k+) | IBR |

| Low-to-moderate revenue (sometimes beneath $80k) | RAP |

| Shut to twenty or 25-year forgiveness | IBR |

| Nervous about curiosity rising your stability | RAP |

| Pursuing PSLF | Whichever has the decrease month-to-month fee |

| Borrowing after July 1, 2026 | RAP (major IDR choice) |

| Married with very completely different incomes | Probably IBR — run the numbers |

| Have dependent kids | RAP could also be aggressive — $50/baby deduction |

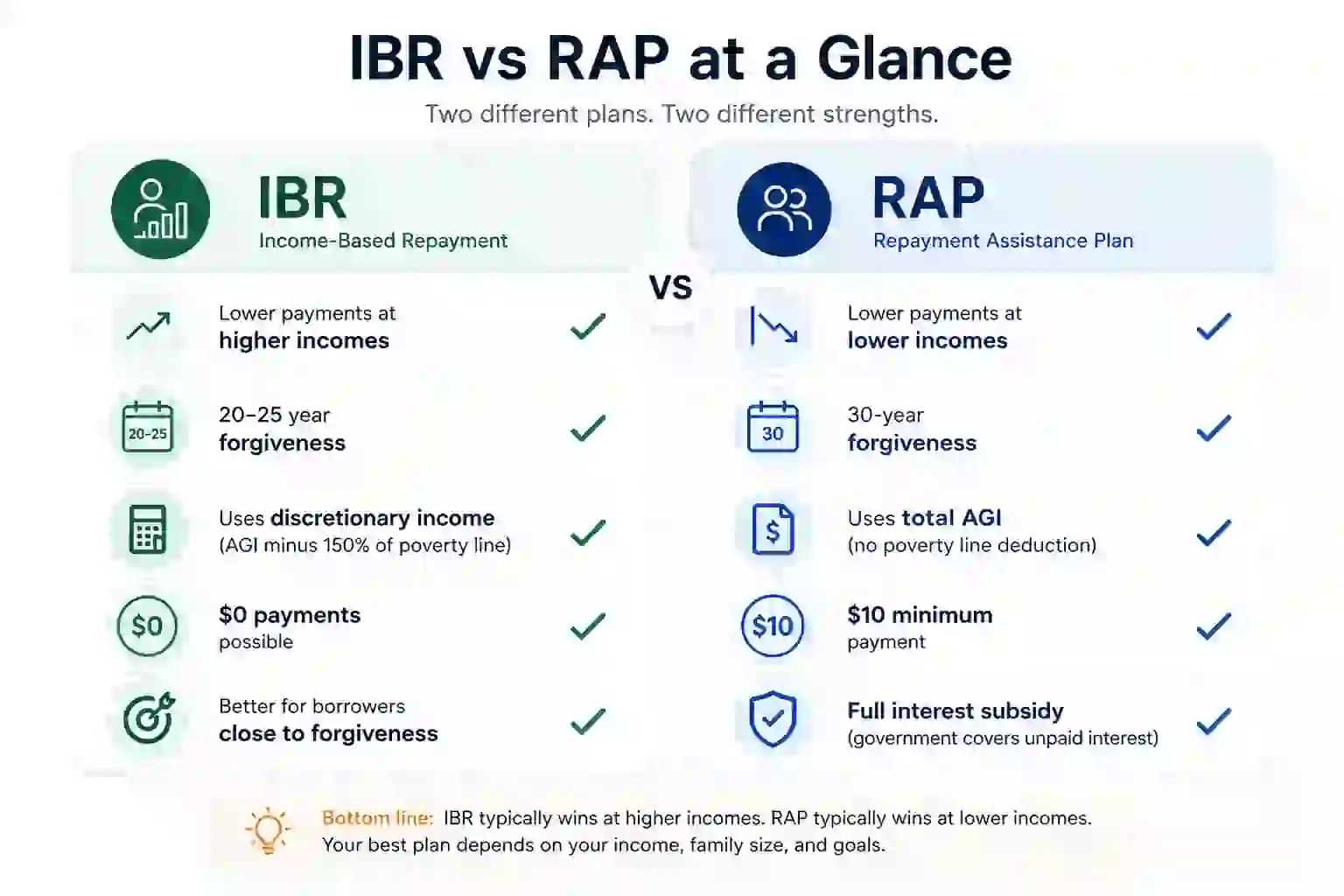

What Is IBR?

Revenue-Primarily based Reimbursement (IBR) has been round since 2009. It ties your month-to-month fee to your revenue, not your mortgage stability, and affords forgiveness after 20 or 25 years.

Right here’s the place it will get complicated: there are literally two variations of IBR, and which one you’re on depends upon while you borrowed.

- Previous IBR (had an impressive federal mortgage stability as of July 1, 2014): Cost is 15% of discretionary revenue. Forgiveness after 25 years.

- New IBR (borrowed on or after July 1, 2014, with no excellent federal mortgage stability as of that date): Cost is 10% of discretionary revenue. Forgiveness after 20 years. The larger win right here is the decrease fee price — not the cap.

Each variations cap your fee at what you’d owe on a regular 10-year plan. And in case your revenue is low sufficient, your fee may very well be $0.

Need to see your quantity? Run it by means of our Previous IBR calculator or New IBR calculator relying on while you first borrowed.

Sherpa Be aware: For those who take out new federal loans on or after July 1, 2026, IBR gained’t be obtainable to you. If all of your loans have been disbursed earlier than that date and also you don’t borrow once more, IBR stays a everlasting reimbursement choice for you. There’s one crucial entice although: in case you take out even one new mortgage after July 1, 2026, all of your loans may very well be moved off IBR and onto RAP or the Tiered Customary Plan. For those who’re planning to borrow once more, that call deserves critical thought earlier than you signal something.

What Is RAP?

The Reimbursement Help Plan — RAP — is model new. It was created by the One Large Lovely Invoice Act, signed into regulation in 2025, and it launches on July 1, 2026.

RAP is the one income-driven reimbursement choice for debtors taking out their first loans on or after July 1, 2026. IBR stays obtainable solely to grandfathered debtors — those that already had an eligible mortgage stability earlier than the cutoff and haven’t taken out new loans since. For those who’re ranging from scratch after July 2026, your decisions are RAP or the brand new Tiered Customary Plan — a fixed-payment plan whose reimbursement time period (10, 15, 20, or 25 years) relies on how a lot you borrowed.

Right here’s how RAP works: as an alternative of calculating funds based mostly on discretionary revenue, it costs a flat proportion of your whole adjusted gross revenue (AGI). The speed scales up as your revenue grows.

RAP additionally has a $10/month minimal. You’ll all the time owe a minimum of $10, even when your revenue is almost zero.

And there’s a significant upside: a full curiosity subsidy. In case your month-to-month fee doesn’t cowl accruing curiosity, the federal government covers the hole. Your stability gained’t balloon when you’re making funds.

The catch? Forgiveness doesn’t come till after 30 years.

RAP additionally features a Matching Principal Cost provision present in no different plan. In case your on-time month-to-month fee reduces your principal stability by lower than $50, the federal government makes up the distinction — capped on the lesser of $50 or your precise fee quantity, minus no matter principal your fee already diminished. For debtors with smaller balances making modest funds, this assure of significant month-to-month principal discount can speed up payoff even inside a 30-year timeline.

How IBR and RAP Funds Are Calculated

That is the core of the IBR vs. RAP debate — and the 2 plans use fully completely different math.

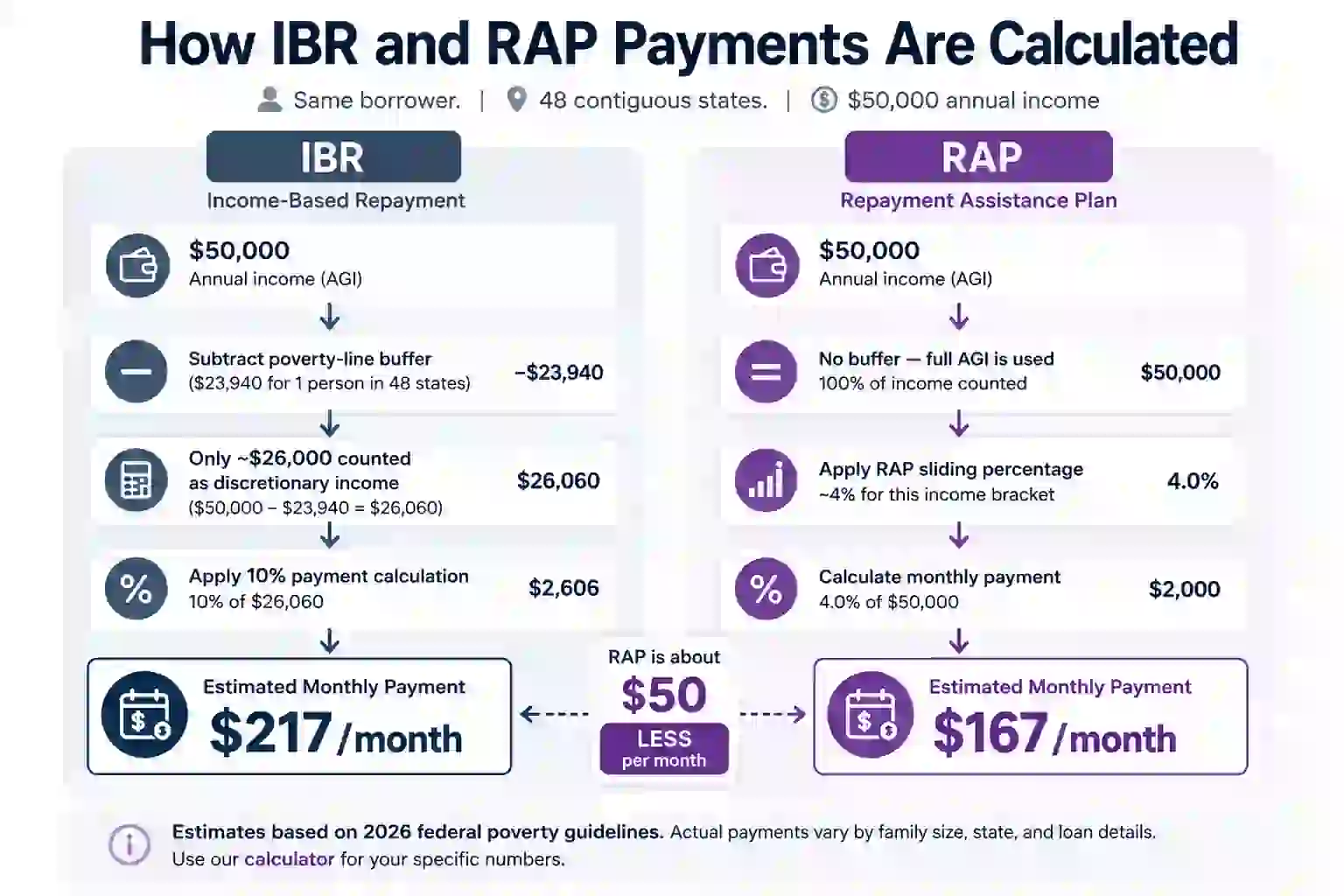

IBR: Subtracts a Poverty-Line Buffer First

IBR doesn’t cost you a proportion of your full revenue. It costs you a proportion of your discretionary revenue — that’s your AGI minus 150% of the federal poverty line. Understanding how AGI elements into your scholar mortgage funds and how discretionary revenue is calculated will show you how to make sense of why these plans produce such completely different numbers.

For a single borrower incomes $50,000, IBR doesn’t cost you 10% of $50,000. It costs you 10% of roughly $26,000. That distinction provides up quick.

RAP: Expenses a Share of Your Full AGI

RAP skips the poverty-line buffer totally and costs a sliding proportion of your whole AGI. The speed begins small at decrease incomes and scales up as you earn extra.

RAP does have one deduction: for each dependent baby you declare in your taxes, your month-to-month RAP fee drops by $50. Two youngsters, that’s $100/month again in your pocket. For households, this modifications the comparability meaningfully. As a common rule, RAP tends to provide decrease funds at decrease incomes. IBR sometimes wins at increased incomes as a result of the poverty-line buffer does numerous work. However the crossover level depends upon your particular revenue, household measurement, and mortgage stability — which is why operating the precise numbers issues.

Sherpa Tip: Don’t guess. Use our RAP calculator and examine it in opposition to our Previous IBR calculator or New IBR calculator relying on while you borrowed. And don’t simply calculate based mostly in your revenue at the moment — RAP’s price scales up as you earn extra, so a plan that appears cheaper now may flip in 5 years in case your revenue grows.

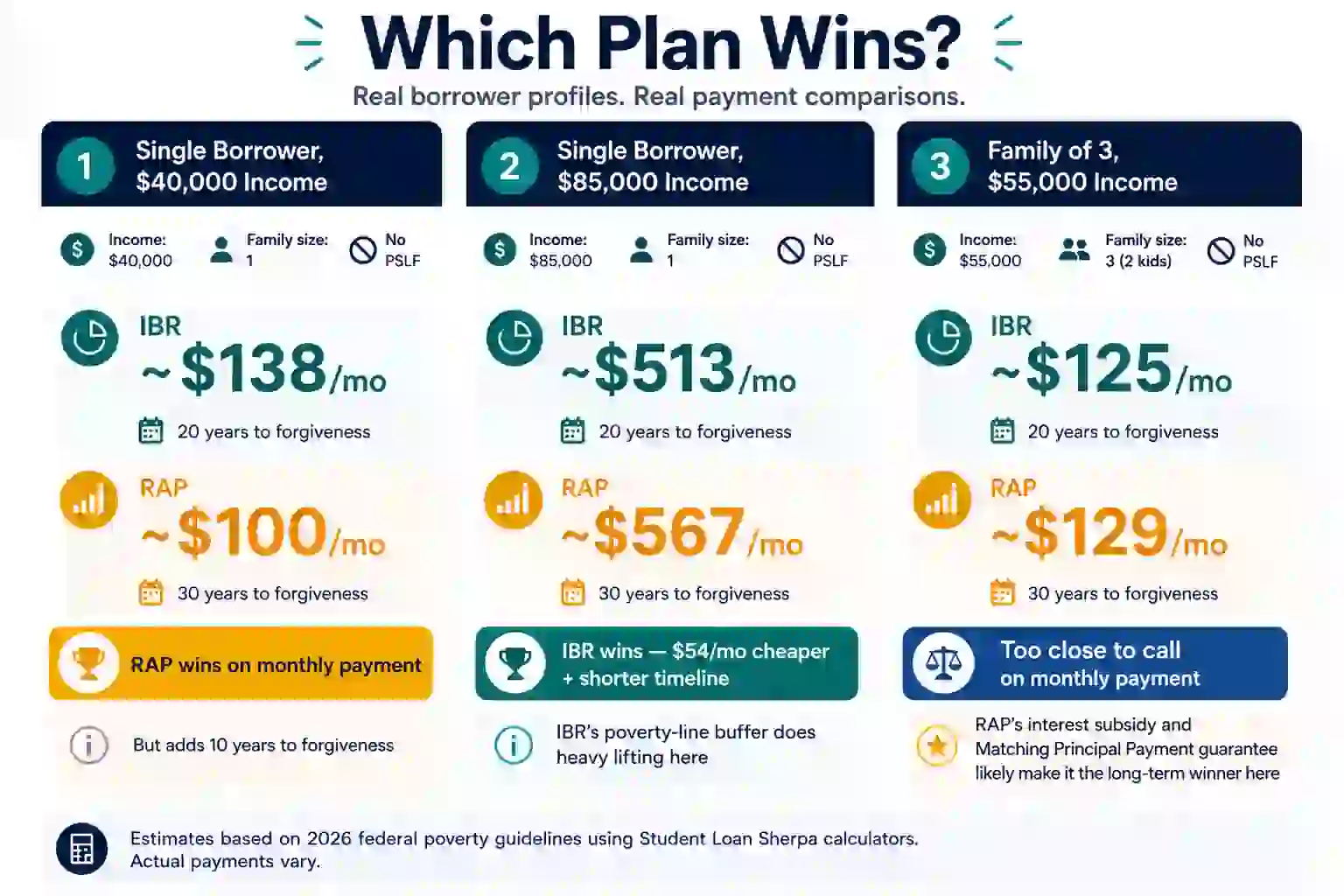

Actual Numbers: Three Borrower Profiles

The infographic under reveals what IBR and RAP truly produce for 3 frequent borrower conditions, calculated utilizing our personal calculators. Assumptions: New IBR eligibility (borrowed after July 1, 2014), 48 states and DC poverty pointers, no PSLF.

Profile 1: Single Borrower, $40,000 Revenue

IBR: ~$138/mo (20 years) vs. RAP: ~$100/mo (30 years)

Takeaway: RAP produces the decrease month-to-month fee right here — $38 much less per 30 days. However the borrower trades that financial savings for an additional 10 years earlier than forgiveness. Whether or not that tradeoff is sensible depends upon their long-term revenue trajectory. In the event that they count on vital raises, RAP’s scaling proportion may flip the mathematics over time.

Profile 2: Single Borrower, $85,000 Revenue

IBR: ~$513/mo (20 years) vs. RAP: ~$567/mo (30 years)

Takeaway: IBR wins clearly right here. It’s $54/month cheaper and reaches forgiveness 10 years sooner. That is the high-income crossover in motion — the poverty-line buffer in IBR’s formulation does vital work at this revenue degree.

Profile 3: Borrower With Two Children, $55,000 Revenue

IBR: ~$125/mo (20 years) vs. RAP: ~$129/mo (30 years)

Takeaway: This one is sort of a tie on month-to-month funds — simply $4 aside. IBR technically wins, and it affords forgiveness 10 years sooner. However right here’s the nuance: RAP’s full curiosity subsidy implies that if the $129 fee doesn’t cowl all accruing curiosity, the federal government picks up the distinction. If this borrower is fearful about their stability rising, RAP’s curiosity safety may tip the choice. The $4/month distinction is shut sufficient that the forgiveness timeline and curiosity subsidy turn into the actual elements.

Estimates based mostly on 2026 federal poverty pointers utilizing Pupil Mortgage Sherpa calculators. Precise funds range.

IBR vs. RAP: Aspect-by-Aspect

| IBR | RAP | |

| Cost calculation | % of discretionary revenue | % of whole AGI |

| Minimal fee | $0 | $10/month |

| Forgiveness timeline | 20–25 years | 30 years |

| Curiosity subsidy | Restricted (sponsored loans solely, first 3 years) | Full — govt covers the hole |

| PSLF eligible | Sure | Sure |

| Open to new debtors after 7/1/2026 | No (except no new loans) | Sure |

| Household measurement definition | Broad | Slim ($50/baby tax deduction) |

| Father or mother PLUS loans | No | No |

| Sometimes higher for PSLF optimization | Generally | Typically |

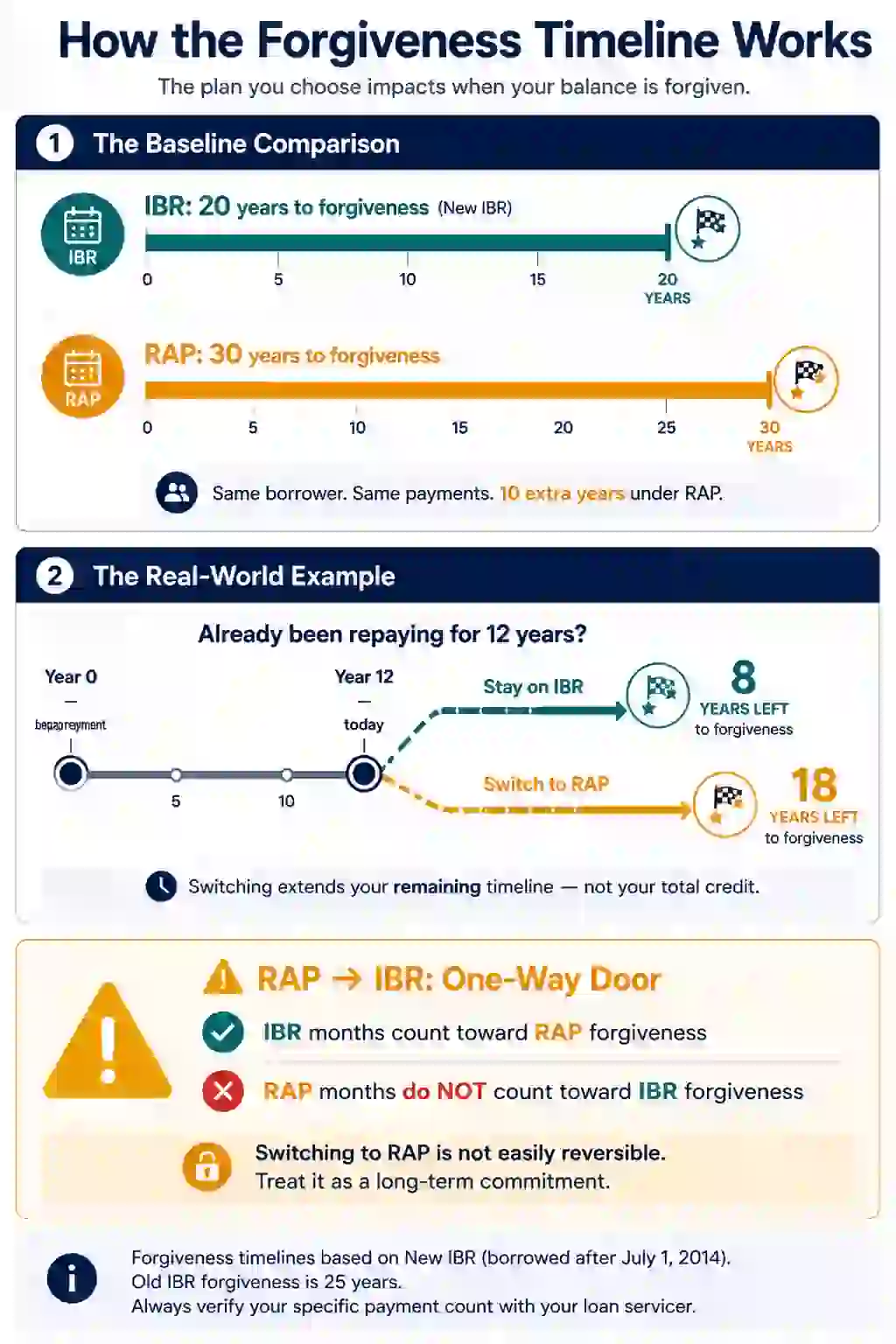

Mortgage Forgiveness: 20 or 25 Years vs. 30 Years

That is the place IBR vs. RAP will get actually necessary — particularly in case you’ve already been in reimbursement for some time. IBR forgives your remaining stability after 20 years (new IBR) or 25 years (outdated IBR). RAP forgives after 30 years. That’s a 5 to 10 yr distinction.

That’s price repeating: switching from IBR to RAP doesn’t reset your clock to zero — however it does lengthen your forgiveness timeline to 30 years whole. For those who’ve already been making funds for 12 years beneath IBR, you’re 8 years from forgiveness. Change to RAP, and also you’ve acquired 18 years left.

If You Change Plans (With out Consolidating)

For those who swap from IBR to RAP, your prior IBR fee months carry over. You don’t lose the credit score you’ve already constructed up.

However right here’s the entice: this solely works a method. For those who later swap again from RAP to IBR — say, since you need the shorter 20-year forgiveness timeline — these months spent in RAP is not going to depend towards IBR forgiveness. The longer you keep in RAP earlier than switching again, the extra credit score you lose.

Switching to RAP isn’t simply reversible for forgiveness functions. Deal with it as a long-term dedication, not a trial run.

If You Consolidate to Get onto RAP

That is the place it will get trickier. Your forgiveness credit score turns into a weighted common throughout all loans within the consolidation — weighted by stability.

- For those who consolidate a $50,000 mortgage with 10 years of credit score and a $5,000 mortgage with zero credit score, you retain most of that credit score. The massive stability carries the calculation.

- However flip these balances — $5,000 with 10 years of credit score, $50,000 with zero — and also you’ve simply worn out practically all the pieces you’ve constructed.

Sherpa Tip: For those who’re contemplating consolidation to entry RAP, run the weighted common math first. Consolidating carelessly may price you years of forgiveness credit score.

The Forgiveness Tax

The federal tax exemption for IDR forgiveness has expired. A forgiven stability could also be handled as taxable revenue within the yr it’s discharged. Ensure you’re not caught off guard by the forgiveness tax invoice.

One exception: PSLF forgiveness stays tax-free on the federal degree. Don’t simply brace for the tax invoice — plan for it. Calculate your projected legal responsibility, then open a devoted taxable brokerage account and make investments a set quantity month-to-month in a broad index fund. A modest month-to-month contribution over 10–15 years, compounding the entire time, can organically construct the precise warfare chest you’ll want when the IRS comes calling. Beginning early is all the pieces right here.

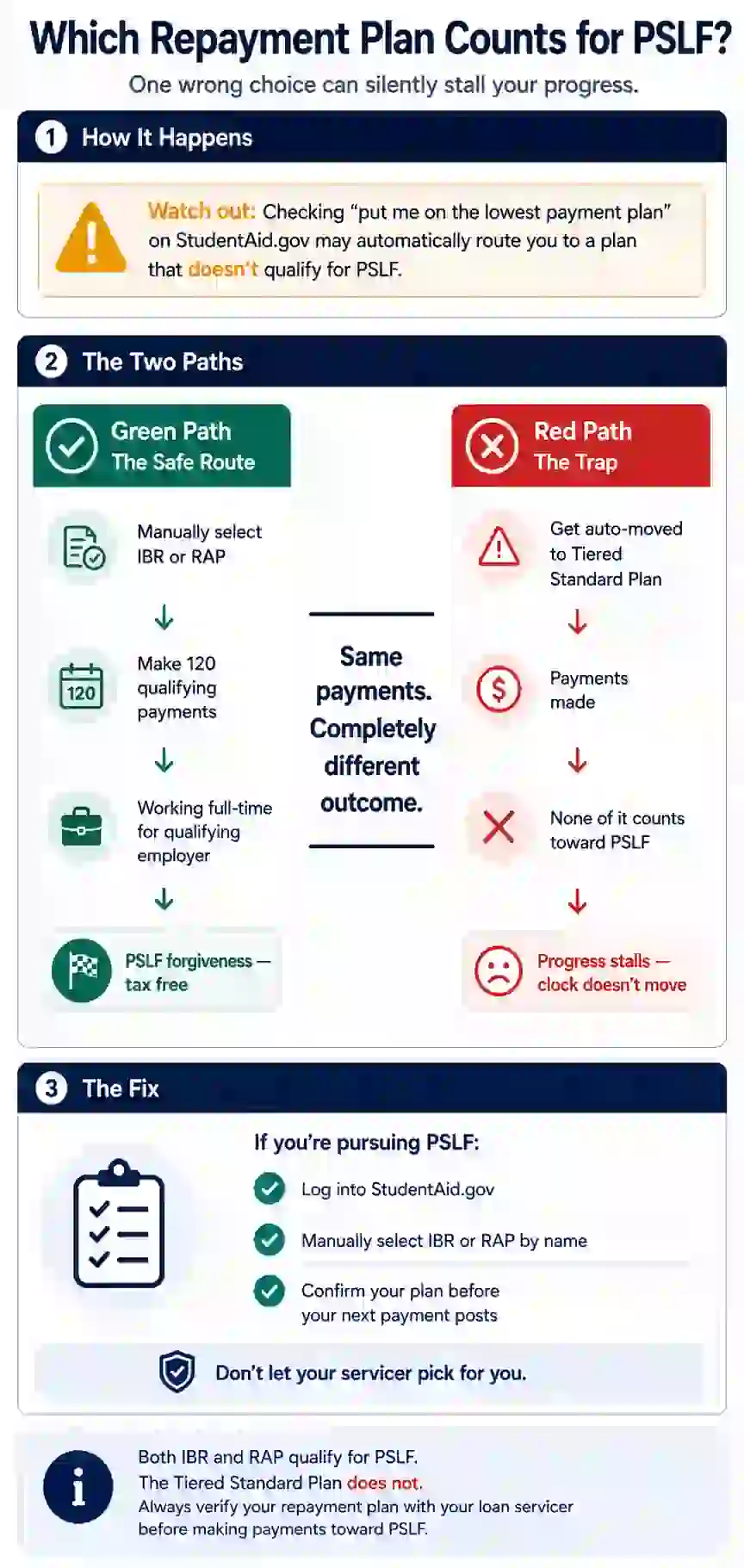

PSLF: Does the Plan You’re On Matter?

Excellent news: each IBR and RAP depend towards Public Service Mortgage Forgiveness. The ten-year, 120-payment requirement didn’t change.

For those who’re working towards PSLF, the plan you select is usually about minimizing month-to-month funds — since PSLF wipes the stability after 10 years regardless.

In lots of PSLF circumstances, RAP may very well outperform IBR — regardless of the longer 30-year forgiveness timeline. Why? As a result of PSLF debtors aren’t aiming for 20- or 30-year forgiveness in any respect. They’re aiming for the bottom potential qualifying fee over 120 funds. That modifications the mathematics fully.

For PSLF debtors particularly:

- A decrease month-to-month fee sometimes issues greater than a shorter forgiveness timeline

- Curiosity progress issues much less, because the remaining stability is forgiven tax-free by means of PSLF

- The higher plan is often whichever produces the smaller required fee over the subsequent 10 years

Instance: A borrower paying $150 much less per 30 days beneath RAP in comparison with IBR may save $18,000 over a full PSLF timeline. In that state of affairs, RAP’s longer 30-year forgiveness schedule turns into largely irrelevant — the stability disappears after 10 years by means of PSLF anyway.

That mentioned, IBR nonetheless has one significant benefit for PSLF debtors: stability. IBR is an older, well-established plan with a protracted PSLF observe document. RAP is newer, and implementation particulars might proceed evolving. For debtors with a few years left earlier than 120 funds, that’s price factoring in.

Sherpa Tip: For PSLF debtors, the optimum technique is often easy: select whichever qualifying reimbursement plan produces the bottom month-to-month fee whereas preserving PSLF eligibility. For those who’re near 120 funds, that’s the one quantity that issues.

Be careful for 2 traps that would derail your PSLF progress:

The Tiered Customary Plan Entice

The brand new Tiered Customary Plan — the opposite choice created by the OBBBA — does NOT qualify for PSLF. For those who’re a brand new borrower and get robotically moved to the Tiered Customary Plan with out realizing it, these months gained’t depend towards your 120 funds. It’s a must to manually swap to RAP to maintain your PSLF progress on observe.

The Father or mother PLUS Entice

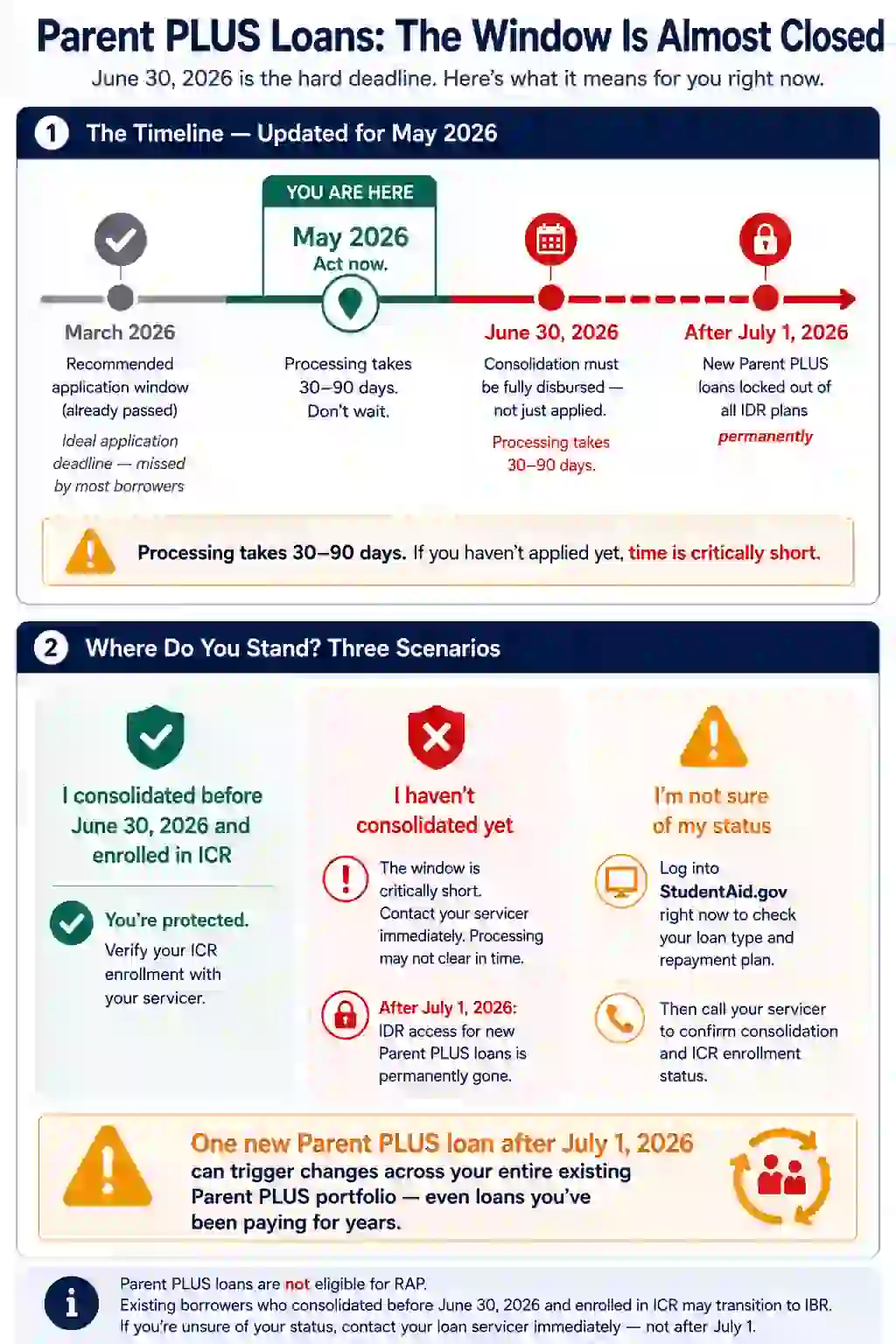

Father or mother PLUS debtors face a crucial two-step course of with two completely different deadlines — and complicated them may price you completely.

Step 1 — Consolidation (Laborious Deadline: June 30, 2026): Your Father or mother PLUS loans should be consolidated right into a Direct Consolidation Mortgage, and that mortgage should be absolutely disbursed — not simply utilized for — by June 30, 2026. Processing takes 30–90 days, so making use of in Might or June is already dangerously late for many debtors.

Step 2 — ICR Enrollment (Deadline: June 30, 2028): As soon as your consolidation is disbursed, you’ve till June 30, 2028 to formally enroll in ICR and make a minimum of one full, on-time fee. That single fee then unlocks the choice to modify to IBR, preserving your 25-year path to forgiveness.

Miss Step 1, and IDR entry is completely gone. Miss Step 2, and also you lose the IBR transition window.There’s yet one more landmine: take out even one new Father or mother PLUS mortgage after July 1, 2026, and your present Father or mother PLUS loans may be pulled onto the Tiered Customary Plan — which has no IDR forgiveness and no PSLF eligibility. One new mortgage can set off modifications throughout your complete portfolio.

For the complete breakdown of deadlines and the step-by-step workflow, see our Father or mother PLUS mortgage forgiveness deadline information.

Particular Conditions: When You In all probability Want Assist

Some conditions are genuinely sophisticated, and the usual IBR vs. RAP comparability gained’t lower it.

Married Debtors

Each IBR and RAP permit married debtors to file individually and exclude a partner’s revenue. IBR’s actual edge for married {couples} is the poverty-line buffer — that deduction out of your revenue earlier than the fee calculation kicks in does vital work at average revenue ranges. One caveat for RAP filers: in case you file individually beneath RAP, your dependent depend is proscribed to kids claimed in your particular person return, which might cut back the $50/baby deduction. And for both plan, submitting individually has actual tax prices — some OBBBA deductions don’t apply to MFS filers — so run the complete tax image earlier than deciding. See our information to IBR for married {couples}.

Father or mother PLUS Debtors

Neither IBR nor RAP is on the market to new Father or mother PLUS debtors after July 1, 2026. When you have present Father or mother PLUS loans, the consolidation deadline is crucial — and the deadline is disbursement, not simply software. Processing takes 30–90 days, which means consultants advisable making use of by March 2026. Miss this, and IDR entry is completely gone.

Be aware: Purposes submitted in Might 2026 might not disburse earlier than June 30. Name your servicer at the moment to evaluate your choices.

There’s yet one more landmine right here. Take out even one new Father or mother PLUS mortgage after July 1, 2026, and your present Father or mother PLUS loans may be pulled onto the Customary Plan. One new mortgage can set off modifications throughout your complete portfolio.

Excessive Balances

For those who owe $150,000, $300,000, or extra, the distinction between a 20-year and 30-year forgiveness timeline — and the tax penalties — may be huge. The maths will get sophisticated quick. If any of those conditions describe you, a one-hour dialog can prevent years of uncertainty. ➤ E-book a session with the Sherpa and we’ll work by means of your particular numbers collectively.

Who Ought to Select IBR?

IBR is usually the best name in case you:

- Have vital reimbursement credit score constructed up and don’t need to lengthen your forgiveness clock to 30 years

- Earn over $80,000 — IBR’s discretionary revenue calculation tends to provide decrease funds at increased incomes

- Count on a major revenue bounce sooner or later — IBR has a statutory fee cap. Your month-to-month fee can by no means exceed what you’d owe on a regular 10-year plan, irrespective of how excessive your revenue climbs. RAP has no such cap. For residents changing into attendings, or anybody on a steep revenue trajectory, that ceiling is significant safety.

- Have a posh household state of affairs — IBR’s broader household measurement definition can considerably decrease your fee

- Are married with uneven incomes and need to file individually to defend your partner’s revenue

- Have already got loans disbursed earlier than July 2026 and need to shield your IBR entry — it’s essential truly be enrolled in IBR earlier than July 1, 2026. Having outdated loans isn’t sufficient safety. For those who haven’t enrolled and also you later take out a brand new mortgage or consolidate, you possibly can be robotically moved to the 30-year RAP observe.

Who Ought to Select RAP?

RAP is usually the best name in case you:

- Are a brand new borrower after July 1, 2026 — RAP is your major IDR choice, and for many, the one one. IBR is basically restricted to debtors who already had a stability earlier than July 2026. For those who’re beginning contemporary, RAP is it.

- Earn beneath $70,000–$80,000 — RAP’s decrease proportion charges can undercut IBR at these revenue ranges

- Are fearful about curiosity rising your stability — RAP’s full curiosity subsidy prevents adverse amortization

- Are presently on SAVE, PAYE, or ICR and wish to select a brand new plan earlier than these plans are eradicated in 2028

- Declare kids in your taxes — the $50/baby month-to-month discount could make RAP aggressive even in opposition to IBR’s decrease base price

Sherpa Be aware: For those who’re presently on SAVE forbearance and attempting to modify plans, be careful for a standard servicer glitch. For those who examine the ‘put me on the plan with the bottom month-to-month fee’ field on StudentAid.gov, the system might robotically route you again to SAVE — which is legally blocked and phasing out. Your software shall be denied. To keep away from this, manually choose IBR or RAP by identify. Don’t let the system auto-select.

Key Deadlines You Can’t Miss

For those who bear in mind nothing else from this text, bear in mind these dates. Too many debtors have missed crucial deadlines just because they didn’t know the foundations modified. Don’t let that be you.

| Deadline | What It Means |

| July 1, 2026 | IBR closes to debtors who take out new federal loans on or after this date. For those who haven’t borrowed something new, you may nonetheless enroll in IBR till 2028. |

| June 30, 2026 (disbursed — not simply utilized) | Father or mother PLUS consolidation should be absolutely processed and disbursed by this date. Processing takes 30–90 days — consultants advisable making use of by March 2026. Miss this, and IDR entry is completely gone. |

| July 1, 2028 | SAVE, PAYE, and ICR are eradicated. For those who don’t proactively select IBR or RAP earlier than this date, you’ll most probably be auto-placed on RAP. Exception: when you have loans that aren’t eligible for RAP — corresponding to a Father or mother PLUS consolidation mortgage — the Division of Schooling will default you into IBR as an alternative. Both means, don’t let your servicer resolve for you. Proactively select your plan earlier than the deadline. |

See the complete record of necessary scholar mortgage deadlines.

The principles are nonetheless evolving. Rules are being finalized, courtroom challenges are ongoing, and servicers are struggling to maintain up. ➤ Be a part of our free e-newsletter — we observe each change and clarify what truly issues for debtors.

A Easy Approach to Resolve Between IBR and RAP

Nonetheless unsure? Stroll by means of this so as.

- Run each fee estimates utilizing our calculators — RAP and IBR facet by facet, based mostly in your precise revenue and household measurement.

- Evaluate forgiveness timelines. What number of years of credit score have you ever already constructed? What number of years till forgiveness beneath every plan?

- Estimate your revenue in 5 years, not simply at the moment. RAP’s price scales up as you earn extra — a plan that’s cheaper now is probably not in 5 years.

- Resolve how a lot the curiosity subsidy issues to you. In case your stability rising retains you up at night time, RAP’s full curiosity protection is an actual profit.

- For those who’re near forgiveness, mannequin the influence fastidiously earlier than switching. Extending your timeline by even 5 years modifications the mathematics considerably.

Backside Line

IBR and RAP are usually not interchangeable. The correct plan depends upon your revenue, your mortgage stability, your loved ones state of affairs, and what number of years of reimbursement credit score you’ve already accrued.

Right here’s the brief model:

- Larger revenue or near forgiveness? IBR is usually the higher selection.

- Decrease revenue or new borrower? RAP is usually the stronger transfer.

- Sophisticated state of affairs? Don’t guess.

Your motion for at the moment: Run the numbers on each plans. Use our RAP calculator and examine it in opposition to our Previous IBR calculator or New IBR calculator relying on while you borrowed. It takes 5 minutes. And mannequin each your present revenue and the place you count on to be in 5 years — RAP’s price scales up as you earn extra, so a plan that appears cheaper at the moment may flip as your profession grows. That 5 minutes may very well be price 1000’s of {dollars}.

For many PSLF debtors, the higher plan is whichever produces the decrease month-to-month fee — full cease. PSLF wipes your stability after 120 qualifying funds no matter which plan you’re on, so the 30-year RAP forgiveness timeline is basically irrelevant. Each IBR and RAP qualify. The Tiered Customary Plan doesn’t — so don’t get auto-placed there with out realizing it.

You’ll be able to swap from IBR to RAP, and your IBR fee months carry over. However the reverse doesn’t work the identical means — in case you swap again from RAP to IBR, these RAP months is not going to depend towards IBR forgiveness. Switching to RAP is successfully a one-way door for forgiveness functions. Deal with it as a long-term dedication, not a trial run.

Don’t swap off PAYE voluntarily proper now — however not due to capitalization. As of July 2023, leaving PAYE not triggers a capitalization occasion, so your accrued curiosity gained’t abruptly get added to your principal while you swap. The actual purpose to remain put is strategic: PAYE sunsets in July 2028, and you’ve got time to fastidiously mannequin IBR vs RAP earlier than being pressured to resolve. Use that window to run the numbers, assess your revenue trajectory, and swap in your phrases. One necessary warning in case you’re contemplating IBR particularly: switching from IBR voluntarily to a different plan is among the remaining statutory capitalization triggers. So in case you transfer to IBR and later need to depart, be sure to’re able to commit.

IBR — and this is among the clearest circumstances the place it issues. IBR has a statutory fee cap: your month-to-month invoice can by no means exceed what you’d owe on a regular 10-year plan, irrespective of how excessive your revenue climbs. RAP has no such cap. As an attending, your RAP fee scales up with each greenback you earn. For those who’re additionally pursuing PSLF, the calculus shifts: choose whichever qualifying plan produces the bottom fee throughout your remaining months towards 120. For many residents-turned-attendings on PSLF, that’s nonetheless IBR as soon as revenue spikes.

When you have vital reimbursement historical past or a better revenue, swap to IBR now — don’t wait. SAVE is legally blocked and each month in forbearance is probably not counting towards forgiveness. One crucial warning: while you apply, manually choose IBR by identify on StudentAid.gov. Don’t examine “lowest fee” — the system might route you again to SAVE and deny your software. In case your revenue is decrease and also you’re near July 2026, it’s cheap to modify to IBR now and re-evaluate RAP when it launches.

IBR subtracts a poverty-line buffer (~$23,940 for a single borrower in 2026) out of your revenue earlier than calculating your fee. You solely pay 10% of what’s left — not 10% of your full revenue. RAP skips the buffer totally and costs a proportion of your full AGI based mostly on 11 revenue brackets, starting from 1% on the lowest incomes as much as 10% for these incomes over $100,000. There’s additionally a $10 month-to-month minimal beneath RAP — not like IBR, there aren’t any $0 fee choices even when your revenue drops to zero. That single structural distinction is why IBR sometimes wins at increased incomes and RAP usually wins at decrease ones.

Sure — and it usually ideas towards RAP. For smaller balances, RAP’s two built-in protections turn into proportionally extra helpful. First, the complete curiosity subsidy: in case your fee doesn’t cowl accruing curiosity, the federal government waives the distinction. Second, the Matching Principal Cost: in case your on-time month-to-month fee reduces your principal by lower than $50, the federal government makes up the shortfall — however with a particular cap. The federal government’s contribution is proscribed to the lesser of $50 or your precise fee quantity, minus no matter principal your fee already coated. In plain phrases: the federal government gained’t contribute greater than you paid, and gained’t contribute greater than $50. For a borrower whose small fee goes virtually totally to curiosity, this provision ensures a minimum of some significant principal discount every month. One necessary caveat: paying greater than your required RAP fee can cut back or get rid of this profit, since additional funds cut back principal straight — probably pushing your payment-driven principal discount above $50, which is the brink that triggers the match. On RAP, paying precisely what’s billed is often the optimum technique.

Pedro Gomez is the new Pupil Mortgage Sherpa and a Licensed Monetary Planner™ with over a decade of expertise serving to purchasers navigate advanced monetary selections. He’s the founding father of International Monetary Plan, the place he writes about worldwide dwelling, geoarbitrage, and techniques for retiring younger, and likewise leads Brickell Monetary Group, a registered funding advisory agency centered on accelerating monetary freedom.

Pedro is the architect behind the “12 Ranges of Monetary Freedom” framework and blends scholar mortgage technique with long-term planning, tax effectivity, and investing. His work is very geared towards upwardly cellular professionals, entrepreneurs, and people seeking to design a life past the default path.

Pedro is on the market for technique periods and press inquiries.